PPSL is 100% owned subsidiary of listed OCL. The other para which takes about change in ownership is about the VSS acquisition of part ant group stake in parent company, not about PPSL

Just to highlight, VSS is not the biggest shareholder as they claimed. This is just eye wash transaction, still the real majority owner is Ant group. The transaction is structured in such a way so that on paper VSS name will appear as major shareholder. RBI is not stupid to fool them with this kind of dealings.

Hi. In 2020, PhonePe went down because Yes Bank went down. Yes Bank used to be the sponsor bank for all UPI handles which were issued by PhonePe. For example if you went to PhonePe and linked your bank account you got a UPI handle which ended with @yesbank.

Now when Yes Bank went down, suddenly as a customer of PhonePe you could not make any transactions from the PhonePe app because the sponsor bank of your UPI handle was not working. So PhonePe spoke to NPCI and other banks. Within a day or so PhonePe got ICICI Bank as the sponsor bank. All UPI handles which ended with @yesbank were routed by NPCI towards ICICI. What do I mean by that? It is not as if your UPI handle on PhonePe app changed from @yesbank immediately. But whenever you wanted to do a UPI transaction on PhonePe, the sponsor bank at the backend whose servers were helping you complete the UPI transaction was ICICI.

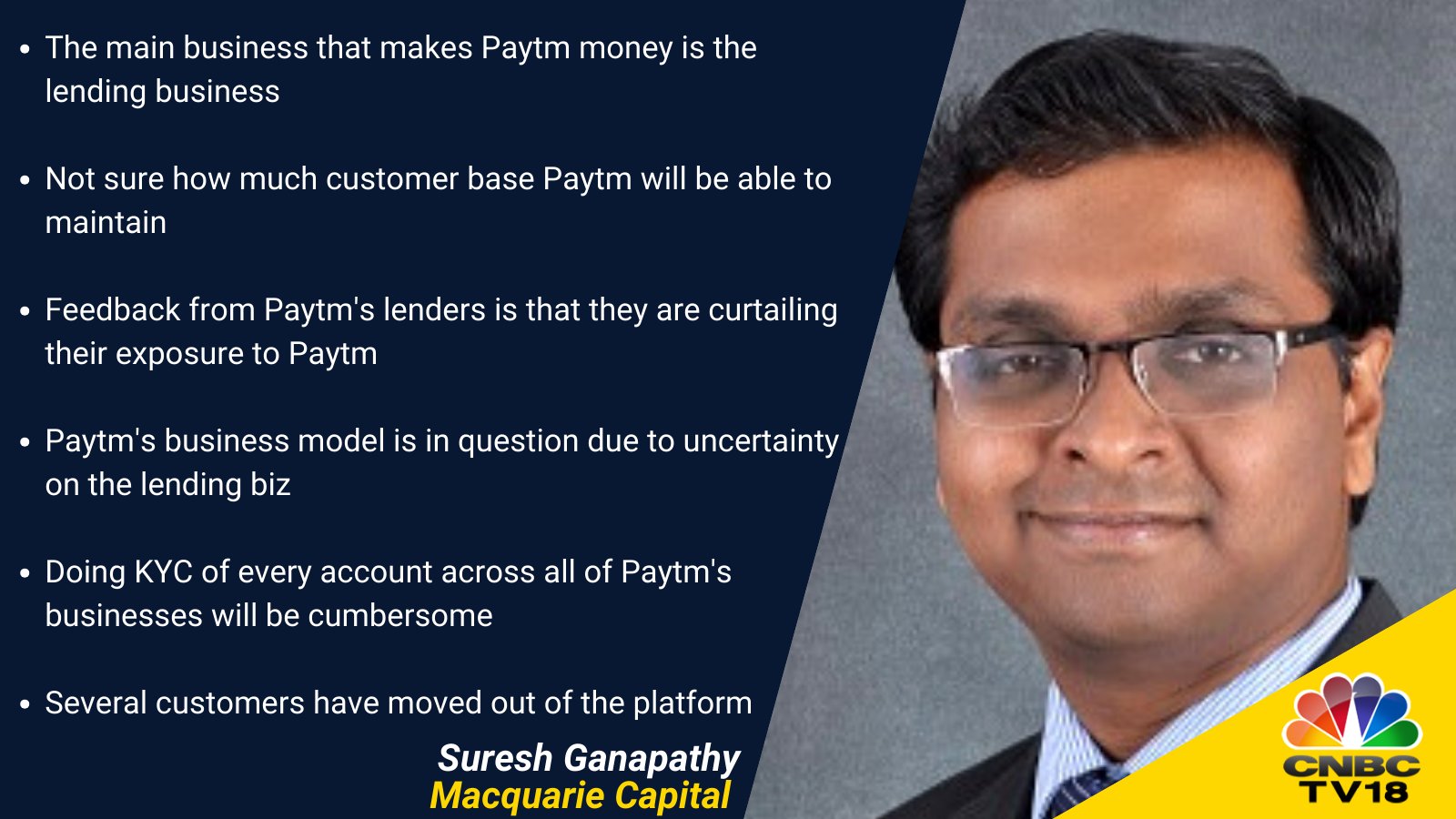

Now ICICI could not have done KYC for crores of UPI customers of PhonePe overnight. I want to learn from this group why would the NPCI and RBI not allow the same thing for Paytm. Why would in Paytm’s case the new sponsor bank or banks be first asked to complete KYC for all the UPI handles? That is a major point which Suresh wasn’t asked. May be I am missing something.

Here are a few articles about what happened at the time of Yes Bank going down.

Type 1. P2P - similar to the Phonepe 2020 case where consumers transact with other consumers

Type 2. P2M (soundbox) - consumer transacts with a merchant using UPI modality (~0% MDR but subvented by banks) - may be individual KYC necessary

Type 3. P2M (POS machines) - consumers transact with merchants (typically big box retailers) where alongside UPI, there are other instruments like CC/DC/EMI as well.

Paytm doesn’t divulge into each of the above categories. Overall there are ~40mn merchants (~10Mn having soundbox i.e. no. 2) and ~300 mn consumers.

Overall above 3 types of transactions accrue 7-9 bps at a net revenue basis with gross being around 30-35 bps which at the scale of Rs 5 trillion per qtr is decent at 25-30% gross margin.

My assumption is case 3 has to be re-KYC surely with there’s VISA/MC etc involved along with banks. Not sure about type 2 (maybe someone can shed some light).

So size and scale of Paytm might dampen their swift transition, which I believe Suresh is alluding to in fewer words.

That’s my 2 cents. Happy to be proved wrong and corrected.

Disc: no holding. closely tracking to see if the evidence so far merits an action.

The problem is not kyc but something else. Kyc is done by bank where you have your saving account and not by upi sponser bank. For example, if you create a new upi on a different app, say mobikwik, today, it will be active immediately without any kyc and its sponser bank (HDFC) won’t come to you asking for your docs. If you want to use wallet, then kyc is necessary. So if paytm ties up with a third party bank to ensure continuation of wallet, then it will be a big headache for the partner bank to do crores of kyc all over again.

Also banks are hesitating to partner with paytm because RBI is very angry at it. Yesterday, Axis bank MD said paytm is a big player and they would be happy to work with them, IF the RBI permits

When Phonepe had to migrate from Yes Bank to ICICI bank because of RBI diktat in 2020, UPI’s major utility was P2P than P2M. In P2P, the underlying account remains with an existing bank and a virtual payment address is provided by the UPI Player in tie-up with a bank like ICICI or Axis or Yes bank. You may observe that when you create a new Virtual payment address, on a new UPI app, its created instantaneously without any KYC completion. So Phonepe had only migrated the Virtual address and not the underlying account which is a far easier exercise

But the situation can be very different when it comes to the merchant onboarding which gained traction around 2021 with BharatPe cracking this model.

In this P2M model, a QR/ Soundbox issuer like Paytm gives the product along with the underlying bank account with a bank account… Paytm having exclusive Payments bank license, it routed all its merchants to PPBL to maximize the opportunity. When the underlying new account is that of Paytm, it is obligated to complete the KYC. Now when you transfer the underlying account, either of 2 things should happen:

Merchant has an existing alternative KYC verified account and Paytm has to just link the QR Code to that account and merchant can continue to operate with that account — (heavy on Ops – Merchant should be reached out to by Feet on street and collect the new account number and then link the current QR Code)

Merchant has no existing alternative KYC account and Paytm has to issue a new account with Axis/ ICICI/ Yes Bank and get the KYC done with the new bank and then link the QR to that newly opened account — (Centralized Activity - KYC to be collected and bank account to be created by FoS)

I think Paytm will focus on migrating the merchants who had loan accounts with them followed by Sound box merchants followed by QR Stickers to migrate. But even if any of these get missed, it will be a reputation risk for Paytm and will have deleterious consequences on the paytm brand name

But I hope and believe that Paytm will be able to overcome this within deadline or work back with RBI for an extension

PS: This is my understanding of the process from my secondary research. Please feel free to correct my understanding

The only problem here is that front end (PayTM i.e. OCL) and backend (PayTM payment bank) has almost same management (all main 3 people were on board of PPBL - Mr. Mahur has now left the board) so in phonepe case there was no linkage b/w yes bank and phonepe in terms of management. I hope they give the same treatment as they given to PhonePe but here it is a little a bit different case.

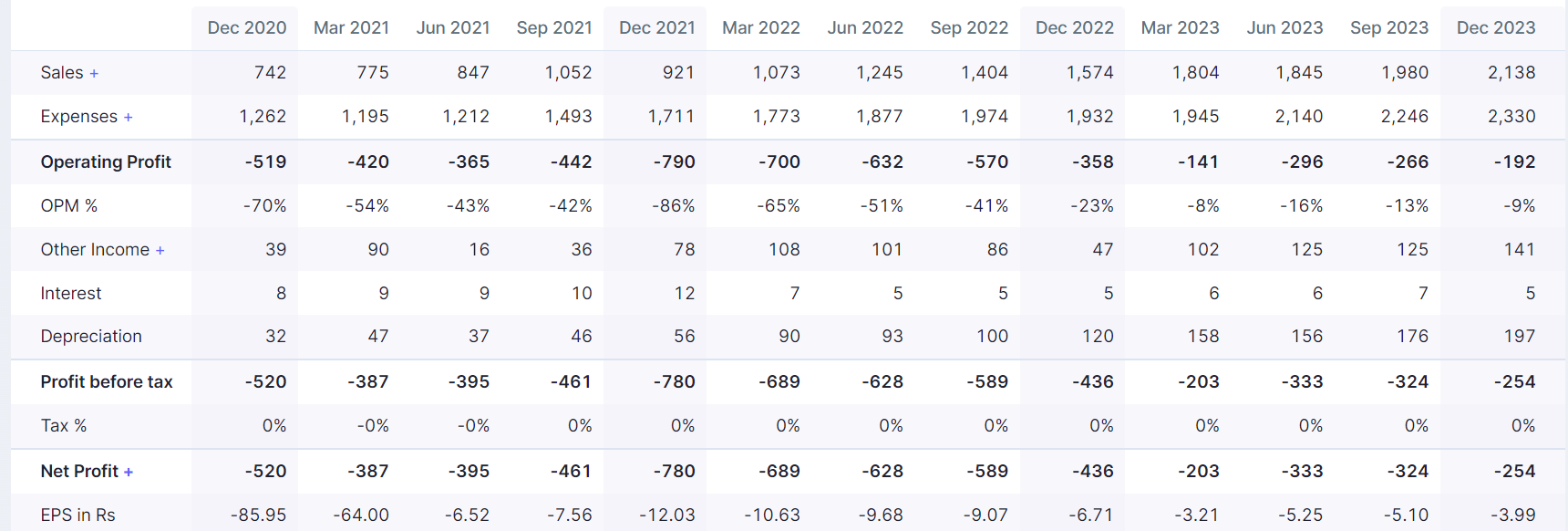

Paytm’s ECL is 5% which is high in lending domain (and that too when the defaults haven’t peaked as they are fairly new in this domain). Irrespective of the topline their bottomline will be wiped off with the ECL as that would be extended in some form of FLDG/cost sharing.

Never said Postpaid was there revenue generator, but it forms bulk of their entry to other loans. It acts as a major feeder for personal loans, as it serves as a great underwriting mechanism in a short period as well as keeps customers from changing platforms. And this will be absent.

With regulator’s action none of the lenders will want to participate with Paytm as a partner, as it will be viewed as going against regulator. Hence, mentioned the cryptocurrency topic.

Paytm in only personal loans (not postpaid, not merchant loans) is not in top 5 and is even further beyond. To find names one can go to Google Playstore and find the apps ranking in Finance category. The ones doing lending among them in top 50 were doing more than what Paytm did last way back in FY23 end. (not namedropping companies as all of them are unlisted, PhonePe, Google are not the ones).

Regulator never takes their step back and they have been taking action against Paytm for six years now in one form or other, hence the deadline has very minor chance of extension but almost impossible to reverse.

Few points to others that I noticed in other posts:

No Paytm cannot get the CIBIL data of customers without their express consent even if they are doing bulk of their transactions using Paytm.

Their UPI services will be up and running before the deadline, but the merchants KYC will need to be done for their wallet business and that is going to cost any entity a bomb (that’s in news today also).

All PPBL services can be routed through other banks and in the future Paytm will get it done. PPBL was most probably a profitable entity, but the addition to the topline wasn’t much. However, the quoted figure by management as revenue drop is going to be much more than stated in the call.

Opinions:

In any other field, still you get forgiven after sometime. In financial services, it takes a long long time to get your reputation back. Regulator doesn’t take extreme steps all of a sudden. So a lot must have been actually wrong with the compliance and regulatory stuffs at Paytm.

Lending was the way ahead for major revenue generation. But with reputation loss and lending coming to a halt, the defaults are bound to go up and it will lay more difficulties for association with Paytm.

When there are tons of stocks giving spectacular returns why gamble with something that is surrounded by so much negativity. Yes you may lose a bounce-back opportunity but the risk reward ratio is not in your favour.

Since you clearly don’t understand how high growth business works, doesn’t makes PayTM a non-business.

As per your defination, even PayPal & sorts of PhonePE are not businesses…

PayTM have made inroads to nukads & grocery stores which even established FMCG players find it difficult to build.

PayTM distribution & penetration is their moat which naysayers would realise only sometime later.

But Paytm is not earning from that nukads or grocery stores… at the end we need profit only… and now Paytm is not alone in providing such services… so market wouldn’t provide such a high valuation (even currently it’s highly overvalued)

Again a misstatement… PayTM ‘does’ earns from these nukads AND grocery stores in terms of merchant loans, soundbox fees, etc.

Also, the broader perspective one should look at is the multiplier effect from 30 crore+ users… It’s a household name now… PayTM can easily leverage on it.

On the profits part, it’s on its way towards it… The management was expecting profits by FY 25… Because of the RBI notification on PPBL, let’s assume a year’s more delay in profitability…

Market was cynical on loss making Zomato too at Rs. 40; look where it is now once the profits started pouring in 6 months back…

Disc: Holding both PayTM & sitting at 2x profits in Zomato

At <$3 billions; (with $0.5B in cash) PayTM is absurdly undervalued, atleast to me.

In my opinion, for a loss making company even if they have 3 billion cash in hand, it will be used for more ads, cashbacks which is effectively cash burning. What matters is how they use the cash in business that will help them generate net profits and FCF. What is their path to profitability going forward, considering their payments bank arm is in dire situation?

As far as the bulls are concerned, which probably includes me, paytm’s path to profitability is similar to its main competitors, such as phonepe and google pay. They don’t hold a payments bank license, either. If one believes the competitors have a meaningful business, it shall apply also to paytm. If we acknowledge competitor’s business, but not paytm’s, I suspect it could be due to the aversion caused by price movements.

One may also like the idea of businesses like paytm having the ability to spawn other businesses relatively easily like broking, ecommerce, etc. Yes, criticism here is that they’re not best in anything.

Indeed, an investor should keep in mind the major uncertainty caused by RBI action, long-running losses, analyst reports, etc. There is serious risk here. OTOH, one may think that RBI is concerned about financial inclusion and respects the significant role of companies like paytm in this. So business continuity doubt is probably an extreme reaction.

(BTW these analyst reports waver all the time, and mostly short term focused, one or two FYs at most. I’m even surprised that they’re even respected by the market. It is a separate topic to discuss.)

These are the situations which present opportunity to earn money, or… lessons :–)

Disc: Invested. I always consider myself as a novice investor. No recommendations here. I welcome opposing views, which would help me keep my thinking unbiased.

If i dont understand fintech business and if i presume that regulators wont step back. (example IEX, despite we retailers and promotors having varying self arguements of non practical,lenthy process …vagere vagere)

If i know that there are bull case arguements when cmp is rising and bear case arguments when cmp nose dives.

Where is the cmp support for paytm, how long it is when we may come to know it has hit the floor, where downside is limited ?