Hi,

I have some cash which I need to park for 18-20 months. I know FD is one of the option but I am looking for some other good options for the same.

Please help.

Hi,

I have some cash which I need to park for 18-20 months. I know FD is one of the option but I am looking for some other good options for the same.

Please help.

You can park money for lesser tenures too, but people usually expect everything even for shorter terms. They expect safety, liquidity and returns more than a FD, that would be a problem. Investing in a financial product that is linked with the market is taking a chance, particularly when investing for short duration.

FD suits best, but depending on safety, liquidity and return, once can look at liquid funds and money market funds too. But a the tenure is 20 months, there will not be indexation benefit for investing in mutual funds, so if the return will be more or less the same, FD will be the better option.

What about arbitrage funds? They have better tax benefits.

I don’t want to go by previous returns. I am more inclined to understand what could be better for near future considering the current economic situations (obviously nothing is certain, so it can be an educated guess only)

Yes, arbitrage funds are an option too. One can look at them. They can invest in bonds up to 35%, so these are like hybrid funds now.

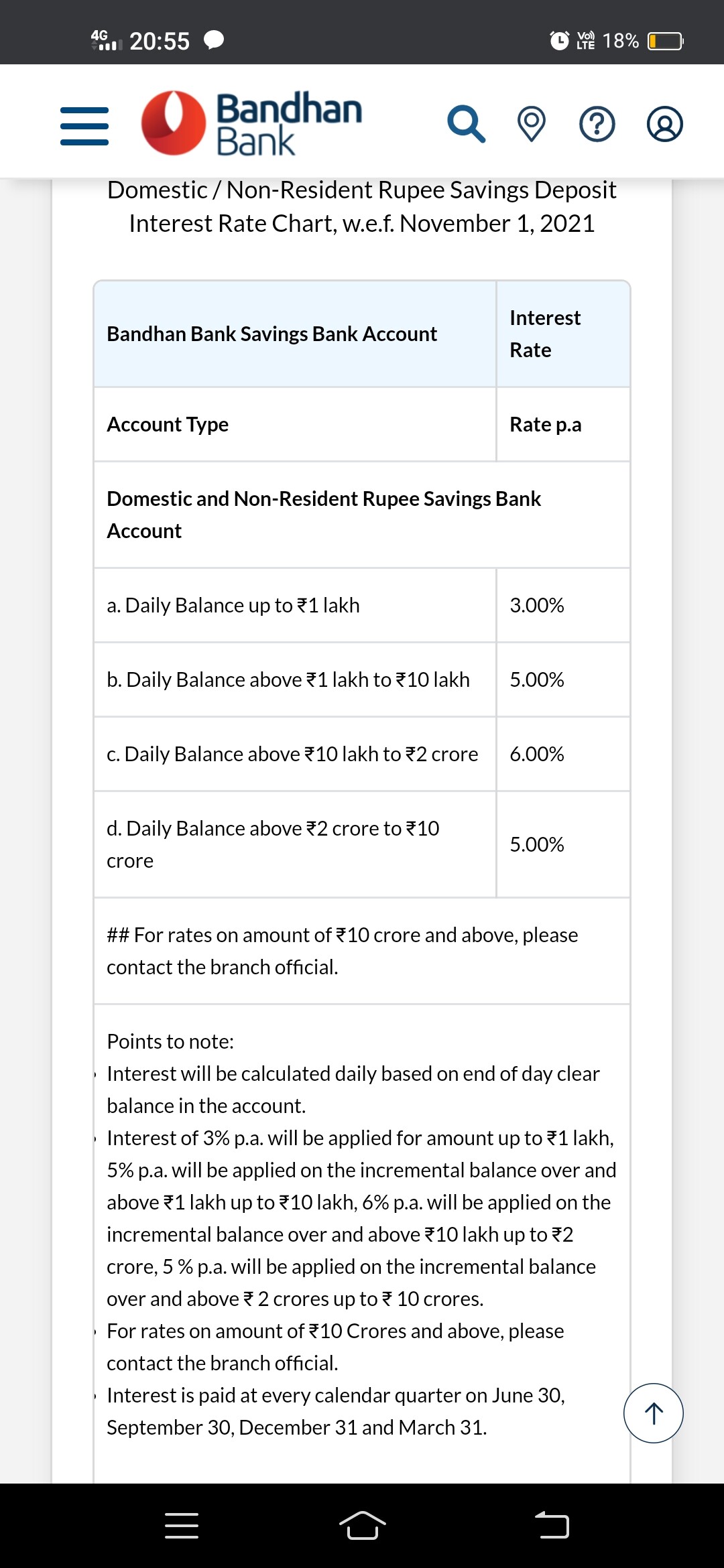

Check this

above rates look attractive, moreover no penalty (like in fd) and u can withdraw and deploy towards stocks in case of a market crash

these interest rates are definitely better than liquid funds etc

Ok. But this contains the inherent risk that equity market possess. If due to any reason, equity market is in crash like situation (or even under medium correction), I might not even get my principal amount back.

The selection should be simple for such tenures. A simple FD would fit the bill perfectly but the return will be less depending upon the tax slab, but the protection of capital, liquidity are guaranteed, at least with large PSU banks.

We have to compromise with one thing or the other, in the case of FDs it is return and tax. At least here, we get to know the return we will be getting unlike debt funds or even arbitrage funds. Even liquid funds could give negative returns for some days, their NAVs will fall. Any market linked instrument will come with volatility, volatility that could smoothen out with time, and the inherent risk of capital loss, however little it may be.

If you are an active participant in the market, who does not want to miss a single day’s fall, then liquid ETFs are the solution.

If you are an equity MF investor and think markets will fall for a few days or weeks continuously, then investing in the overnight or liquid funds of the same fund house, of your equity funds could work, but you have to check the instant redemption limit, or you can switch from liquid funds to equity funds, but have to pay the exit loads if any and the taxes as switching is redemption.

What we need money for and how do we need it, at the end of our tenure, should be the criteria for selecting an option.

Overnight fund is a good option.

Agree on this, but main point is “Over the long haul”.

Does 18-20 months fit this?

All wonderful suggestions in previous posts. Before choosing one of them - I think you need to be super-clear about your goal and your risk appetite…

Looking at your first post, I had assumed that your requirement is complete capital preservation with no risk at all (for e.g. money to be kept aside for a planned expenditure in 18 months - like house/education etc.)

But, looking at some of the suggestions, I think many have interpreted requirement as maximizing returns with reasonable risk (for e.g. keep money aside for a possible expenditure which may not be required - like travel/luxury purchase etc.)

| Least Risk | Max Risk | |

|---|---|---|

| Planned expense Have to preserve capital |

Cash/FD - Least possibility of loss of capital. - May loose value due to inflation - Sure to meet the planned expense |

Debt MF (Money Market/Liquid) - Higher possibility of loss of capital (due to rising yields). - May atleast match inflation - Can theoritically loose some capital |

| Optional expense Can risk capital |

Debt MF (Short-Duration/Credit Risk) - Higher possibility of loss of capital (due to rising yields) - May slightly beat inflation |

Any other MF scheme (Debt/Equity/Balanced) - All risks apply (Fund Manager risk, Interest Rate Risk etc.) - May give superior retuns |

Note:

Thanks for various options. I will check on this