Business Model

Paramount Dye Tec Limited operates through two primary activities: manufacturing and trading, focusing on synthetic fibers and yarns. Here’s an overview:

Manufacturing Operations

Produces synthetic fibers, particularly recycled acrylic yarns used in sweaters, mufflers, caps, and socks.

Yarns are made by processing waste from virgin synthetic fiber manufacturers.

Contributes 65% of FY24 sales with a 22% EBITDA margin.

Since they use recycled fibres, their raw material procurement costs are significantly lower than virgin fibre yarn manufacturers and thus their EBITDA margins are higher.

Trading Operations

Trades in various yarn types, such as acrylic cloth, blended yarn, nylon, and polyester yarns.

Includes domestic sales and surplus raw materials from manufacturing.

Contributes 35% of FY24 sales with a 5% EBITDA margin.

Note: While the primary focus is expanding the manufacturing unit, trading continues to maintain customer relationships and handle bulk orders.

Capacity and Utilization

Fiber Capacity:

3600 MT annually (12 MT/day x 300 days on a 12-hour shift).

Capacity doubled from FY22 to FY23, with EBITDA increasing 4x.

Current utilization: 95%.

Company is producing excess recycled fibres as their yarn capacity is fully utilized so they have to sell the excess stock or store it as inventory

Yarn Capacity:

Current: 1440 MT (4.8 MT/day x 300 days) with 97% utilization.

Planned by FY25-end: 3540 MT (7 MT/day + 4.8 MT/day) using funds received from IPO in Oct-24, a 2.5x increase.

Company had already given orders for the new machines as per the RHP

The company has started laying the wires and transformers in mid-Nov with machines expected by end of Nov. Production to start in Q1FY25.

Key Financial Highlights

Cash Flow:

CFO/EBITDA ratio: 11%, with positive operating cash flow.

Personally, whenever, I have reached out regarding some questions, he has been really forthcoming and prompt even on late Sundays.

The remuneration seems fair

Risks and Concerns

Concentration Risk: Although, this is because the company is really small and doesn’t need to diversify yet.

Top 10 suppliers account for 100% of purchases.

Top 10 customers contribute 78.18% of revenue.

Promoter-Related Risks

Promoter company is engaged in a similar line of business of cotton yarn recycling and manufacturing. Future plans, including potential acquisitions, remain unclear.

Raw Material Volatility

Prices of key inputs like acrylonitrile fluctuate, impacting pricing and margins. Competitors with better production efficiency or superior quality may erode market share.

Seasonality in Demand

Seasonal dependence exists, but capex from IPO proceeds targets expanding into the summer wear market.

Planned portfolio includes blends of acrylic-cotton, cotton-polyester, and other materials for t-shirts, shorts, and polos, mitigating seasonality risks.

Industry Outlook: Textile industry going through major tailwinds. Source: Systematix Institutional Equities

Personally, whenever, I have reached out regarding some questions, he has been really forthcoming and prompt even on late Sundays.

Did you reach out to the promoter via some email or did you talk over call? The valuation seems very tempting. The only major risk I see at current valuation is promoter’s own private entity, did you get any clarity on that ?

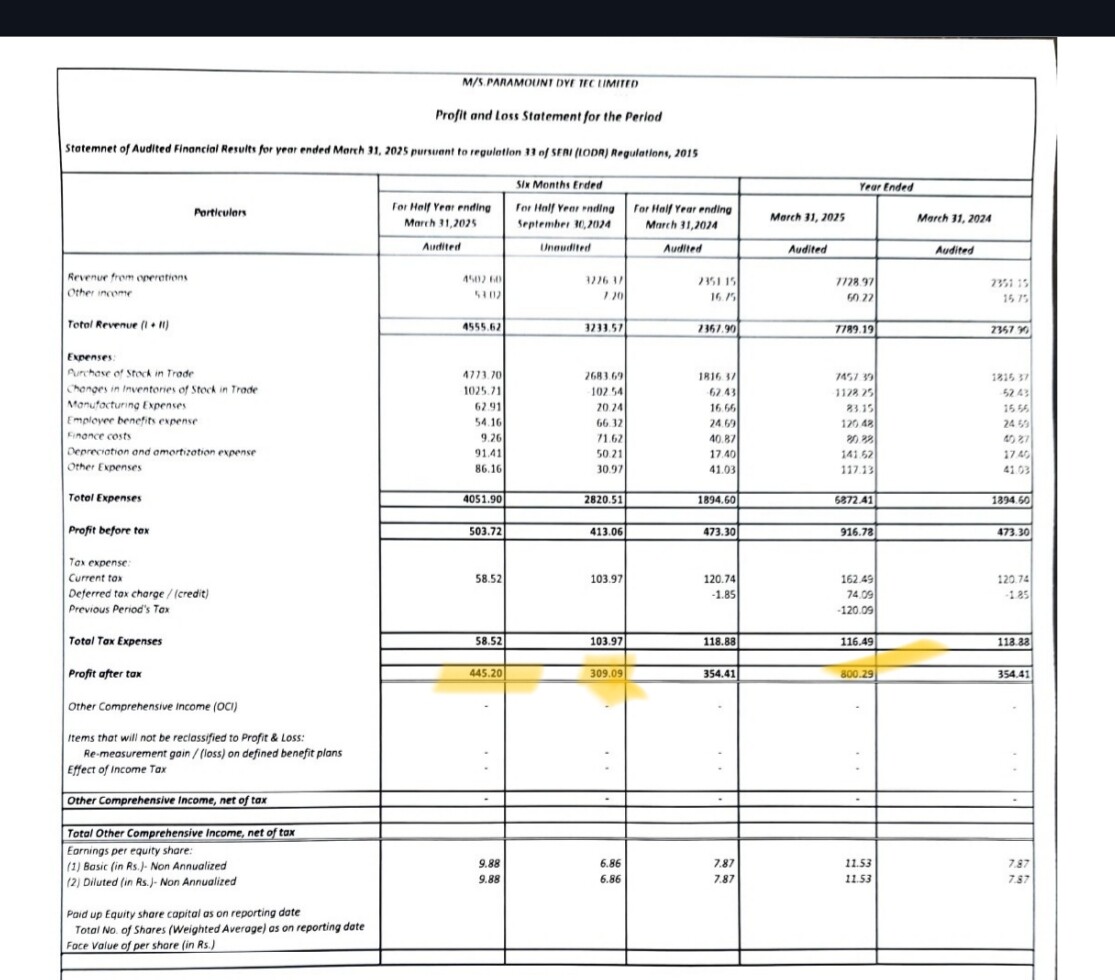

Sales up 229%, EBITDA up 157% and PAT up 126% and CFO to EBITDA has also improved significantly.

Receivables / Sales is at 15% which is pretty good considering the new facility just went live.

Inventory is still pretty high and probably would remain high as such is the nature of the business

The only major risk I see at current valuation is promoter’s own private entity, did you get any clarity on that ?

I didn’t get a chance to reply. The private entity processes cotton yarns from recycled cotton fibres whereas the listed entity processes synthetic yarns. The plan is to eventually merge the private company into the listed entity but I don’t have any timelines.

Very well put. But it can happen due to tax implications/ adjustment of deferred tax. But it should be shown in 3/25 half year figure. May be it is a typological mistake as net tax payable is shown as 58 lac which is low.

But be aware of these SME companies as there is no transparency in their information due to lack of disclosures. So always make indepth analysis when rosy pictures are being shown. Further there is no MOJO in most such companies which leads to abysmal performance/ closure when competition catches up.

Promoter has 3 other companies on his name . All 3 company facilities are shown at same location on Google.

This has been mentioned in the RHP and in the Youtube video itself, there is another business of cotton yarn recycling that runs nearby which the company plans to merge down the line.

Company is at a 2x MRR in April and pretty sure they would finish with a higher sales growth. Current TTM PE is 5.64, forward PE all thing being the same would be ~3.

Also, note that the company has land worth ~13 Cr on its books.

Warrants in SMEs get cancelled in my experience any time that share price drops below the warrant price. One example contrary to this is Madhusudan Masala.

I tried calling on the number mentioned on the company’s website and nobody picked up.

Let’s wait for the Sep results, we will get an idea of what’s going on

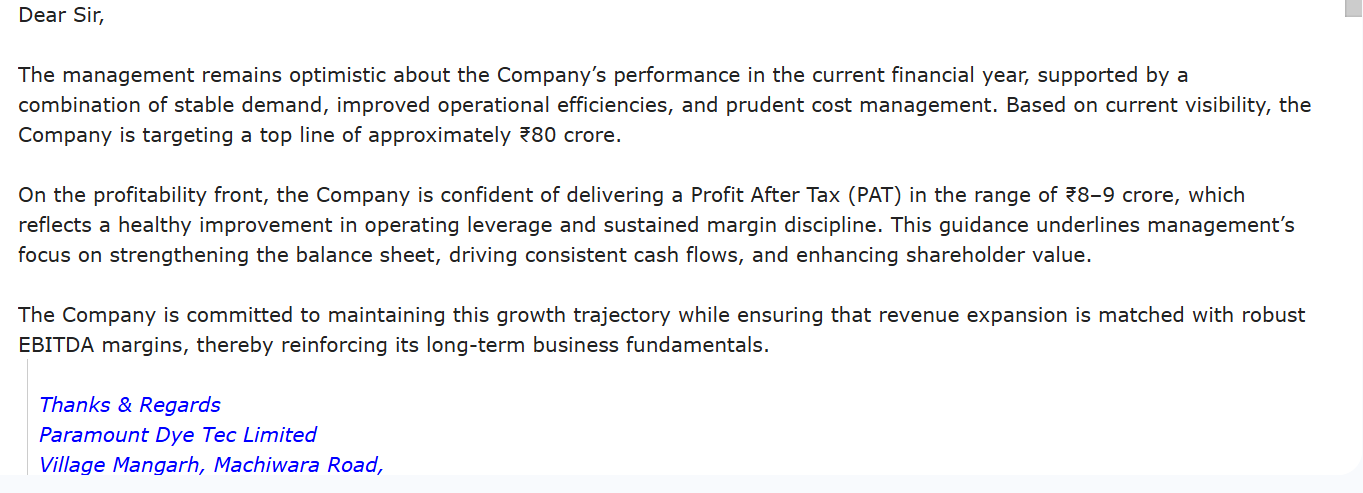

I had written to the Paramount dye tec team regarding the recent developments (Fire at the plant, tariffs for garment/fabrics industry, cancellation of preferential issue and very few updates from the company regarding operational achievements). This is what they responded with. Looks more of high level and generic response, nothing much to ponder:

Dear Sir,

Greetings from Paramount Dye Tec Limited. We truly value your concern and continued trust in the Company. Please find below our detailed clarification on the points you have raised:

Recent Plant Fire

The Company operates two independent manufacturing facilities:

· Fiber Facility – Village Mangarh, Machiwara Road, Kohara–141112, Punjab

The recent fire incident was confined exclusively to the yarn unit, while the fiber unit continues to function smoothly and remains fully operational. Importantly, all assets across both facilities are comprehensively insured.

The management has already initiated immediate and comprehensive measures to restore production capacity at the yarn facility to normal levels in the shortest possible time. Every effort is being made to minimize operational disruption and ensure resumption of full-scale production in a safe and efficient manner.

Withdrawal of Preferential Issue

The previously proposed preferential issue has been withdrawn after due deliberations of the Board. This decision was taken keeping in view internal considerations as well as the prevailing market conditions. The withdrawal does not reflect any liquidity stress or weakness in business fundamentals. Rather, the management remains confident of sustaining growth through internal accruals and operational efficiency.

Industry Challenges & US Tariffs

We are fully aware of the broader challenges in the textile sector, including oversupply pressures and recent changes in the US tariff regime. The Company has taken proactive steps to diversify its product mix and strengthen relationships with both domestic and overseas customers to mitigate potential impact. Management remains optimistic that our robust fiber operations, along with recovery at the yarn unit, will help sustain stable performance in upcoming quarters.

Corporate Communications & Investor Confidence

We acknowledge that the stock is currently trading at low valuations. Management is committed to enhancing transparency and frequency of updates to investors and stakeholders. In the coming months, we plan to share more structured communications on operations, strategy, and new initiatives being pursued.

We sincerely thank you for your concern and support. The Company remains firmly committed to restoring full capacity, protecting stakeholder interests, and driving long-term sustainable growth.

The company is terribly cheap at its current valuation, considering it has 13 Cr land on its books as well.

Concerned that it might get delisted at this rate, market sentiment needs to shift a bit. Hopefully, something happens and we get a pop like LT Foods which was also 5 PE at one point in time and became a 6x.

As a part of follow-up communication, I asked the team for future guidance and looks like they are anticipating of doing similar set for numbers for this financial year.

Also, can anyone share if the management has guided for fy26 numbers? Couldnt find much, hence wanted to check if the management is walking the talk or not.

D: Invested

They have still not published any report on the damage done due to fire in their plant. Sloppy from the management. Looks to me like the listing has not gone the way the had hoped

I exited today. There are low hopes of recovery from here with no triggers, no communication from management. I think it will keep hovering around the cmp and as per my interaction with the management - they are hopeful of matching the revenue of last year. But when asked about the fire incident and how it affected the operations - the standard answer is everything is on track and we are doing good.