Company continues to maintain sales traction supported by export sales (contributed 37%+ in Q3FY25). Export order book of Rs.2300 Mn + as of December 31, 2024 equivalent to four months sales. Quantum of proposed capex, investment and ability to raise borrowings (over equity dilution/QIP) would be important to understand.

2 Likes

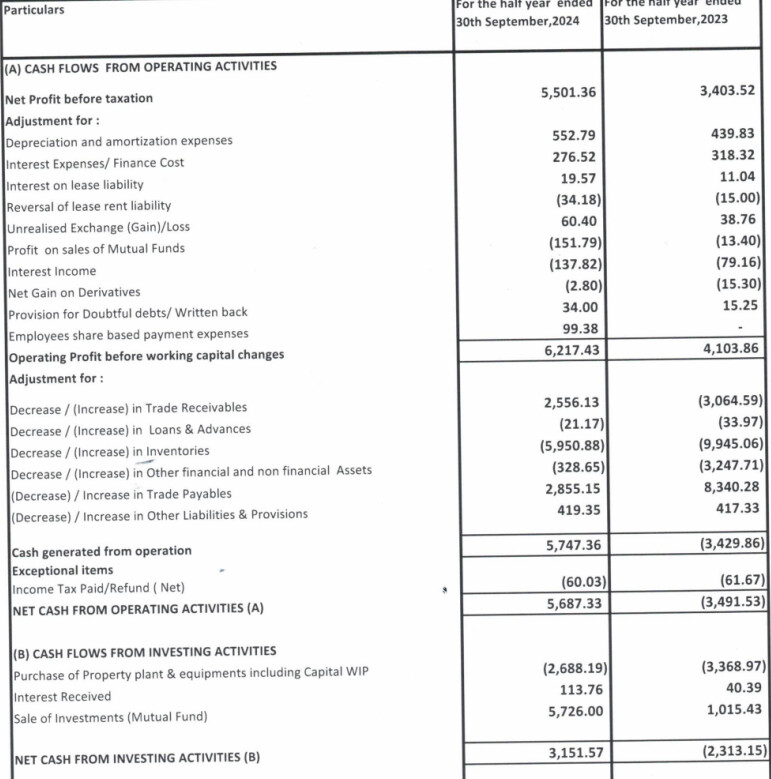

I am not able to understand in the cash flow of FY 24 that profit from operation is 95 crores but receivable is 84 crores and inventory is 121 crores? Is this normal?

Big players are entering this sector, how will small players be affected going forward? Though it will take time for the giants to scale up, the valuations surely wont be the same

Good part is 50% of this company’s topline will be from the USA, where these other players don’t have much penetration

2 Likes

I may be wrong but I differ here.

I think the biggies or others didn’t get penetrate is by choice not that they couldn’t. These players now have the plans of expansion to US which is yet to be played.

It seems the phrase “high entry barriers” may no longer be valid, atleast partially. If we see the past, there were multiple players with intense competition in the sectors telecom, airlines and recently paints. Of course who consolidated positions is secondary.

But I believe the recent entry players, margins on low voltage section will mostly be lost and high voltage section is the one we need to watch for. At the sametime, I also assume the players will also be ready to take losses for 4-5 years to capture market share.

Invested and now looking for an exit.

5 Likes

Have been researching this stock for a while after coming across it in various platforms and the thread here in VP was very helpful.

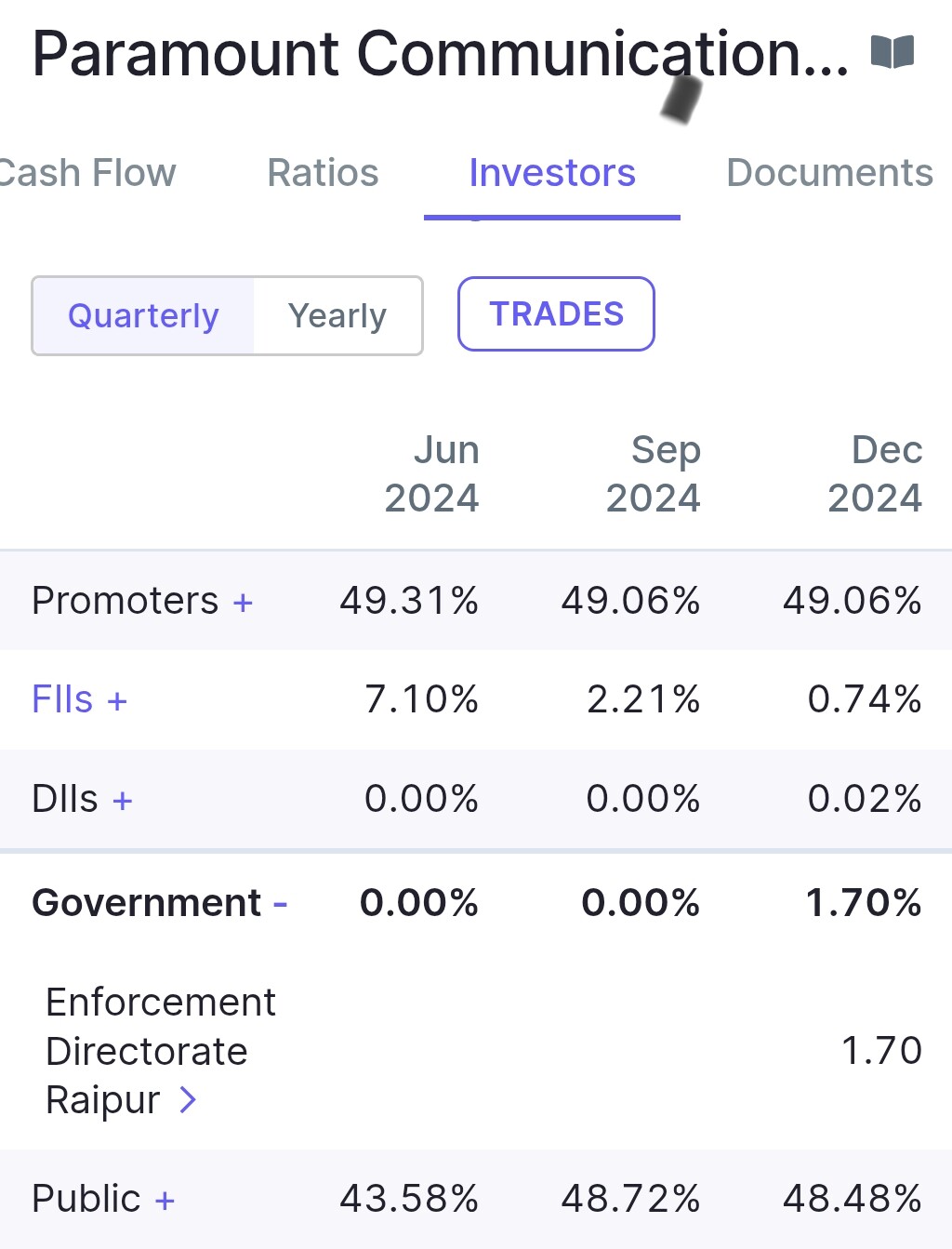

While going through most recent shareholding i found out that ED(enforcement directorate) has got a stake of 1.7%

Could not come up with any news or disclosures of the same.

This is what Google AI says:

Could any member clarify on the same?

Also interesting that no DII’s have any stake in this company despite showing promising returns over many years and FII’s(I’m presuming these were new investors who invested in pref issues) have no current stake from as high as 7%

While i agree that institutional holdings is not a fool-proof way to judge a company, a company with market cap in excess of 1500 crore and high growth with profitability should evince good interest from small/midcap focused funds.

This is one of the criteria i use to shortlist/avoid companies as institutions have significant knowledge of factors beyond retail investors purview (like management quality, CG issues, etc)

Company has consistently traded at significant discount to industry peers

The other big negative trigger is the foray of Ultratech and more recently announcement of Adani getting into P&W industry which could lead to de-rating of established players and we have seen how that has played out in paints sector.

Disclosure: Not invested but tracking

If things were that much simple. When you are investing in Asian paints type companies with high valuation such things are important. Like the ones with polycab, Havells, kei etc. Paramount is available at mid teen pe a lot of risk is already baked in the price. Also there is risk of US recessions or tariffs and all.

On the bright side paramount is available at mid teen PE, growing nicely even when copper price was down, copper is looking very bullish and seems to give a multi year breakout. So paramount is a very good investment opportunity imo.

Here take a look at copper price chart. Anybody with basic understanding of technicals know copper price is going to explode very soon

I was invested in Sirca paints in 2022 and exited in 2023 with very good gains. I was unaware of all the big players entering the paint industry. Sirca is in a niche space was growing nicely. Share price followed. I exited when growth seems to be slowed down.

Few months ago when paramount share price was higher some people were very bullish on the forum and was giving an exit pe of 50 now at mid teen ttm pe people are bearish. This shows narratives are formed after price movement. I also suffer from it. I might be biased since I’m invested in paramount communication.

13 Likes

Why would higher Copper prices be positive for a consumer of the product?

It will lead to higher raw material costs which may not be fully passed onto customers due to competitive pressures and slowing economy.

Even assuming they are able to pass on 100% of the cost, i don’t see how that will be positive for the company as that will be more a function of margins and efficiency.

In a competitive market, price-rise generally leads to lower margins and/or sales.

5 Likes

Finally got clarification on the same.

Query was raised during Q3 Earnings call conducted by the company.

Sharing screenshot of the relevant section of the transcript below:

5 Likes

The ED’s shareholding in Paramount is linked to the Mahadev Betting App case. The accused, currently under investigation, allegedly used hundreds of crores for pump-and-dump activities in multiple stocks. The transactions were carried out through Zenith Multi Trading DMCC, but the ED has now seized its holdings in around 10 companies, including Paramount.

That said, I firmly believe Paramount and its management have no connection to this entity or its activities. However, the stock has seen a sharp correction and is trading much lower. With my entry at around ₹80, the stock has dropped about 40%, despite being a strong exporter of cables to the US and catering to domestic demand.

The stock is currently under pressure due to US tariffs on metals and the ED’s seized holdings. As an investor, I’m still trying to confirm whether these tariffs apply to wires and cables and what impact they might have on Paramount. If they do, its US distributors are likely to increase pricing, which could affect demand. I plan to clarify this in the next earnings concall.

So far, there have been no ED raids or direct allegations against Paramount, yet the stock seems to have priced in all possible worst-case scenarios. Competition isn’t a major concern either—Adani and Birla have a minimal presence in this segment. Given their recent expansion moves in cement, they might consider acquisitions in cables too, and Paramount remains among the top 10 in India and ranks 6th in sales.

For now, I remain invested, confident in the management and the long-term growth of the power sector.

6 Likes

Metal tariff won’t be applicable on them as that is a raw material used and will be universally applied to all countries, what’s relevant is reciprocal tariff which is 15%+GST and other charges for cables and wires(custom duty) [Source: Google] which India levies and which Trump has said will go live on April 2nd. So it will depend on what rates other countries apply to see if it will be beneficial/hindrance for the company. Generally speaking, India levies higher taxes vis-a-vis other countries.

Optically the stock seems one of the cheapest in the industry but maybe there is a reason for the same.

Untill i see get more clarity, better cash flow and institutional interest i have decided to stay away but will keep it in my tracking list

4 Likes

Revenue of cables and wires makers to rise 15-16% in fiscal 2026.pdf (104.4 KB)

As per Crisil Cables and wire Industry report.

Domestic Market expected grow 15 - 16%

Export Market expected to grow at 20 - 22%

3 Likes

I started looking at this stock because of its exports.

The valuations seem too cheap to be true especially for a sector that’s so hot.

There’s an event which is really interesting

The Tibrewala money laundering case originally came out in early 2024 on which day the stock topped.

The volumes aren’t really that high. Looks like a lot of people were taken by surprise.

The stock goes down and consolidates after which this article drops:

The article was published on September 3,2024 on their site and on September 6,2024’s physical copy

Right after which the stock saw massive volumes during which “institutions”(the ultimate beneficial owner of these pooled capital FIIs can’t be found easily) and other 1+% shareholders exited

They haven’t raised the 400cr QIP yet

Found this sequence pretty interesting so thought I’d share it. I’m not accusing anyone of anything

Disclosure: not invested

10 Likes

That was quite insightful, what I am trying to understand is that I looked into this case and what I understood was that this was among the 14 stocks that were getting manipulated so that the top around 110 was created around the early 2024. But what I am unable to understand is we can see that the company’s fundamentals (as in Rev, Profits etc ) are improving but obviously the biggest red flag is that the avg CFO/EBITDA conversion for the past 5 years have been about a meagre 20% which clearly shows that the cash conversion quality is poor, maybe that is the reason for the cheap valuation, but the management had reasoned that this was due to as they were not able to do factoring. So to sustain the kind of growth rate at which they are growing they need to either raise equity of debt to fund their WC requirements, but they’ve been saying that they will raise 400Cr of equity and if the co doesn’t raise this equity it wouldn’t be able to grow at all. It’s tough to make sense of this situation. I thought I was missing something in the business, now I realise what it was.

Thank you so much @Bull_Miller !

9 Likes

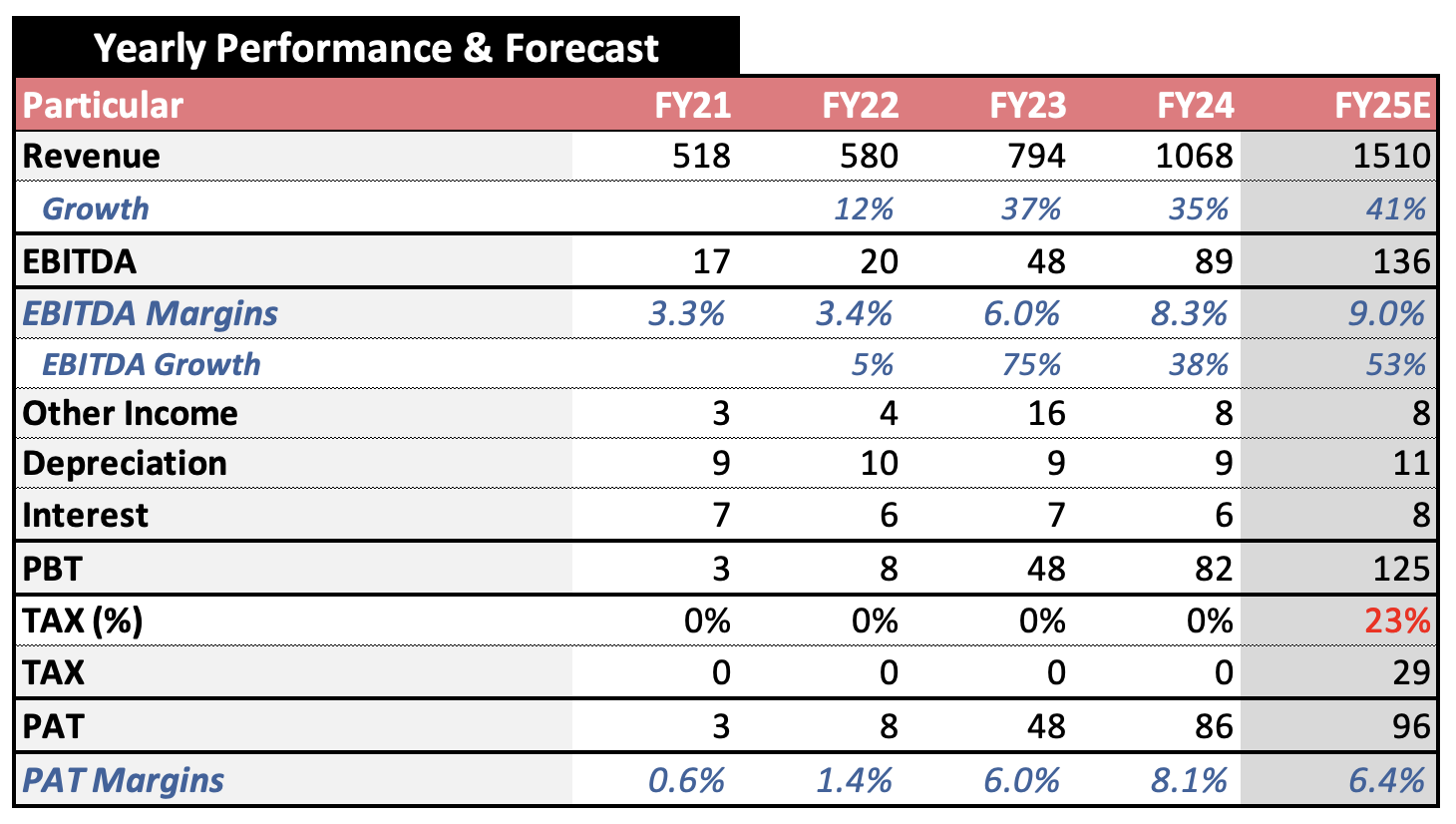

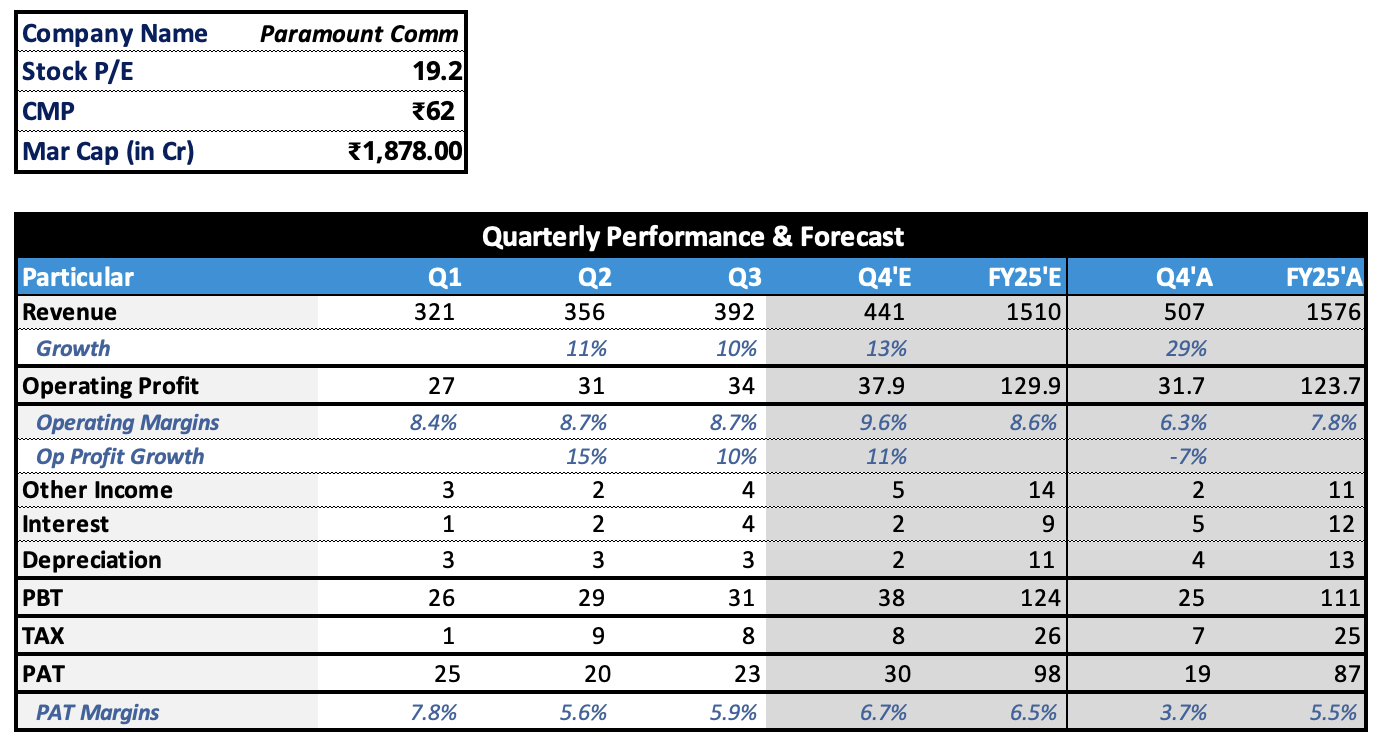

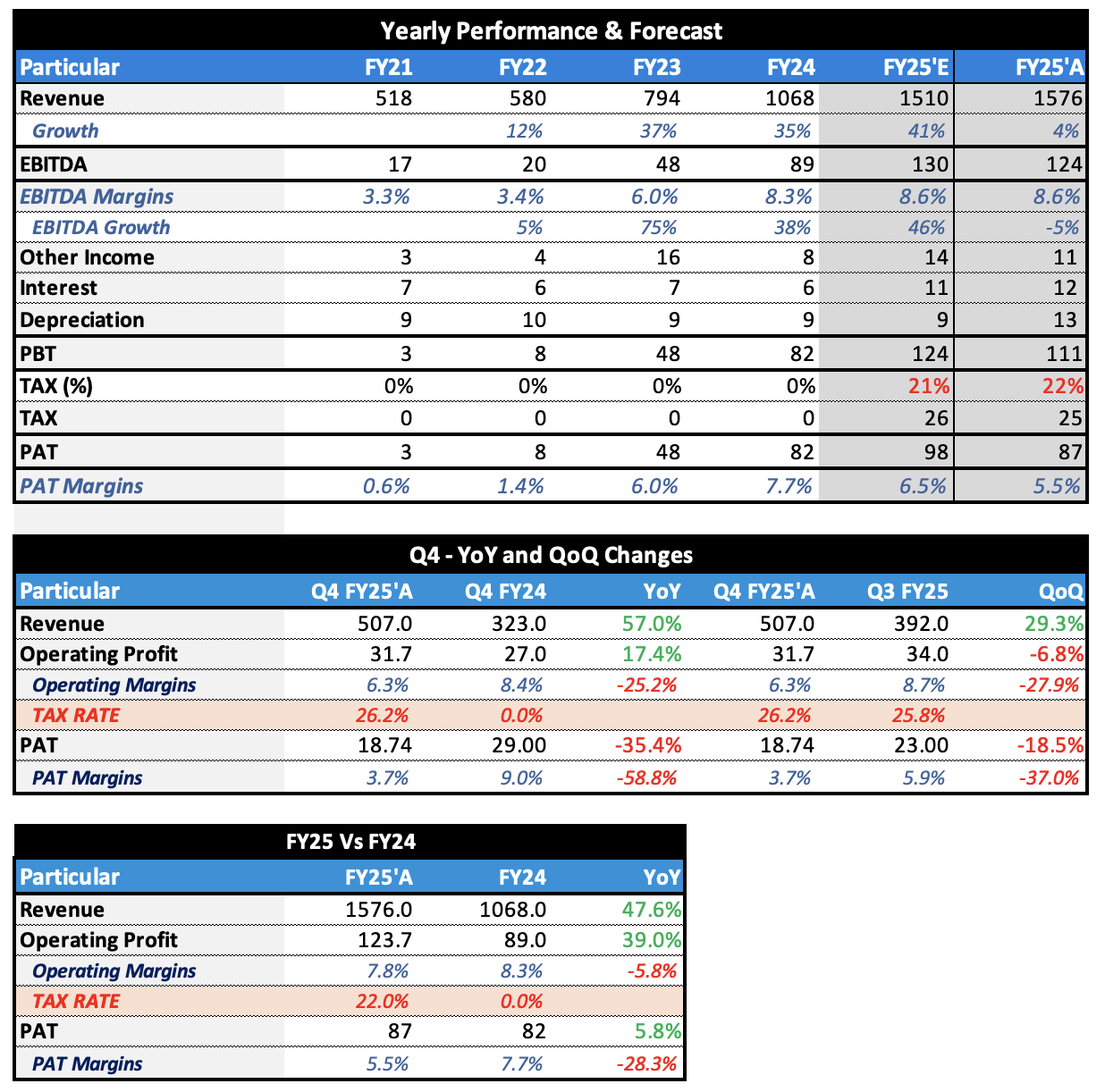

As per my analysis company will do 1500 Cr Plus of revenue and 97 Cr + PAT in FY25 driven by extreme growth in the industry as a whole and Huge increase in exports

3 Likes

The company will definitely do a lot of growth but the issue is cash flows and hence the growth the company is poised to do if the company fails in raising capital.

1 Like

Please check half yearly cash flow from operations

This shows management is working on that

2 Likes

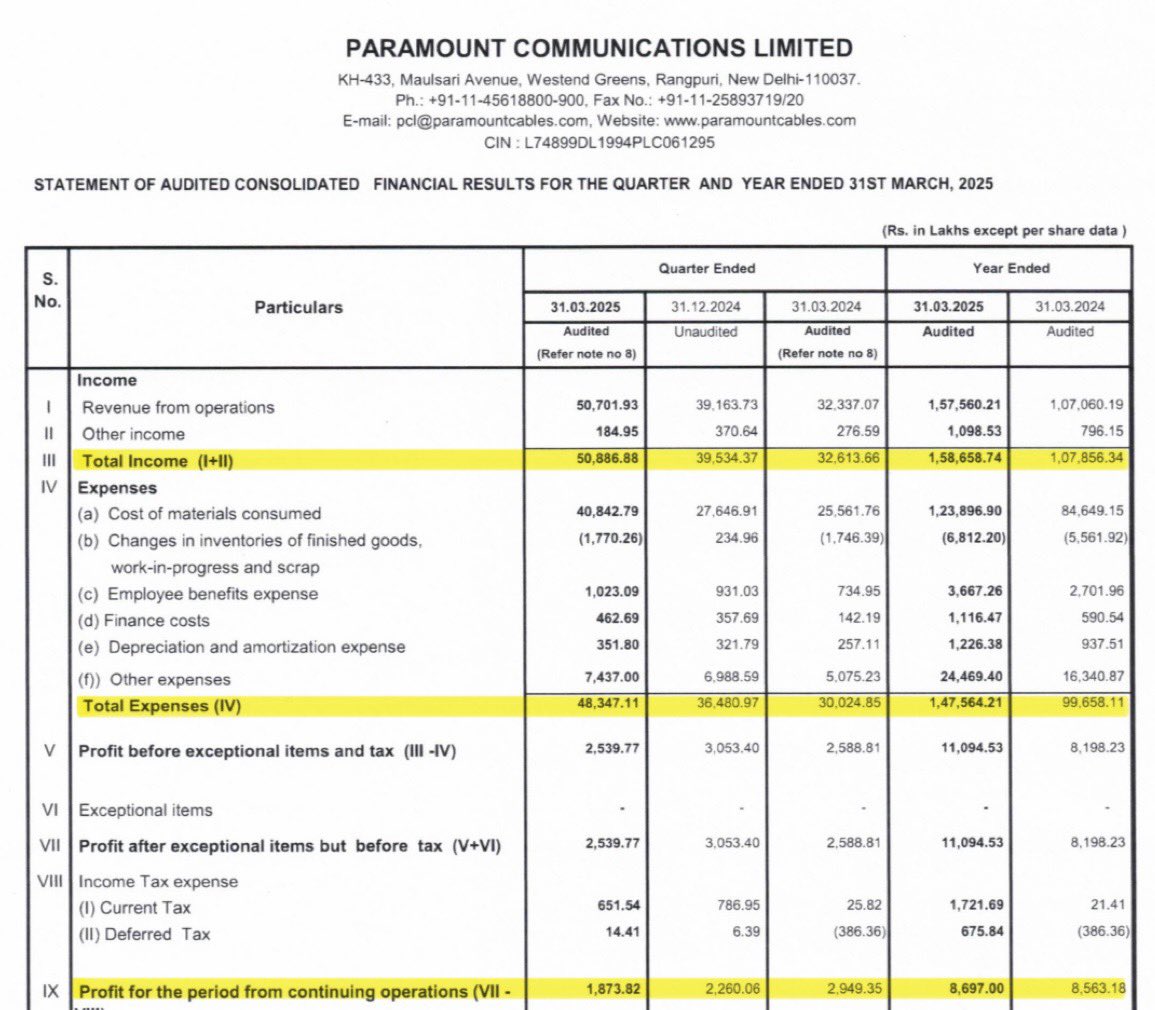

Company performs really very well but face challenges on EBITDA margin front because of Material cost.

As they are in B2B business, Hence they cannot transfer cost on customers.

Rest on revenue front company beaten Management guidance by 17% (management given guidance of 30% growth but company shows growth of 47% thats huge.

6 Likes