Attended the concall. Looks like they are going to sacrifice Margins for topline growth. I asked if you are giving 30-35% guidance for revenue what’s the PBT (not asked about PAT due to tax issue) growth will be. They are telling if my top line growth is 30-35% my PBT growth will be higher. I said then that means margin improvement but here your margins have dipped. He is saying if I can grow 30% at 10% margin product I can grow 50% at 6% margin product. So my take is when you transition from 9% margin to 6% margin your bottom line is going to suffer for the transition period no matter what. Already stock is not moving for few quarters due to PAT not growing for tax issue. Now again they are going to sacrifice margin for topline growth. Though they are claiming company’s aim isto grow the profit (PBT or PAT) my take is for next few quarters the PBT is going to suffer no matter what.

Souresh, management is more focused on more cash Profit not on book keeping profits. They can generate 9% easily but thier cash will be stuck in the working capital.

Stucking in working capital issue might suffer company more in longer term, because of that management more focused cash profit not a bookkeeping profit.

Same has been witnessed through the balance items of FY25.

OCF/EBITDA stood at - 98%

Revenue growth in Fy 25 stood at 47% (but Receivable come down from Rs. 252 Cr to Rs.205 Cr).

So, we should project margin between 6.5% - 7%.

Depending upon the situation of working capital margin can increase.

Due to lower margin profit growth will be lower than revenue growth in short term period.

At this valuation 20% profit (cash profit not a bookkeeping profit) is enough for rerating of the valuation.

We should expect valuation reratibg from Q2 Fy26 once profit growth visible.

Disclosure - Invested.

Management said they were focused on PBT. But that dropped 1% from Q4FY24. Not sure about what’s happening here

Wc or cash flow has nothing to do with margins imo. When a company has ROCE or ROE of 15-20% and growing at 30-40% the cash flow and WC is going to suffer no matter what..it has to raise fund or increase short term debt.. that’s why the fast growing SMEs have cash flow problem.

Well in that case there will be no PAT growth for one more year. Check last year EBITDA margin. From 8% margin to 6% margin means 25% drop in margin to offset that one needs to grow the topline at 33% just to maintain the same ebitda.

I couldn’t attend con call. Did Management mention what is the structural change in business which led to such sharp drop in margin?

Volume, realization , margins are a lot dependent on market condition & own market play . This can’t change just like that. What is the guarantee that revenue jump will follow through in coming quarters when we have compromised on margins?

Are they consciously dropping margins to get more business?

Sometimes when you sell items for cash you give discount. So margins take dip. Cash flows improve. This is not a structural change. What they are telling is long term objective is to increase Profit. But when you suddenly start giving discount for direct cash payment margin will suffer and so does the profit for the transition period. This might be a phenomenon of 3-4 quarters.

I am not sure if this is just a trade off between cash discount and margins. Such tactical measures are applied only for a particular segment of a business which is inflating your working capital requirement. So you give upfront cash discount for payment. A qoq jump in overall revenue by 30% with a drop in overall margin by roughly 3% tells the entire business has seen some strategic call by management. This is a very rare phenomena in my view.

Here is my obsearvation , where I start with comapring similar comapny in same sector with similar growth tregectory

Onse side we have

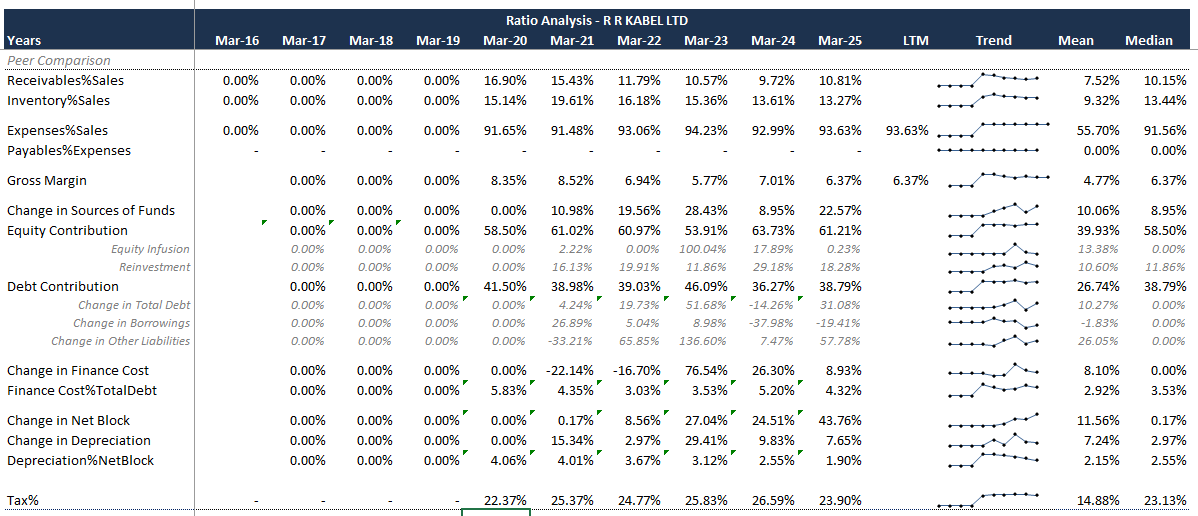

RR Kabel: Where Operates in the same line of business.

Showing great sales growth with no compromise on margins

Demonstrates that if you pursue sales growth by offsetting margins, it is not a long-term strategy

what Issues I Observed with Paramount Communications:

- Confusing Management Commentary on Margin Reduction

Management appeared confused while answering the first question regarding margin compression.

First explanation: Claimed the margin drop was due to a fall in raw material (copper) prices.

This is factually incorrect there has been no significant price fall in copper.

- Unreasonable Justifications Provided

Utilization of Increased Capacity:

Management stated that increased capacity utilization led to margin reduction.

This is counterintuitive higher capacity utilization should typically improve margins, not reduce them.

De-risking from the US Market:

Management cited uncertainties in a major market (USA) as a reason to scale back.

This is contrary to industry behavior – most companies are expanding exports to the USA, not pulling back.

Even if de-risking is needed, should it come at the cost of margin reduction?

Feels like “burning down the house to kill a spider.”

- Vague and Strategic Deflection

When the management couldn’t provide a concrete explanation, they resorted to generic statements like:

“Business strategy must be dynamic and evolve daily.”

- Contradictory Approach to Order Book Management

Typically, selling at low prices should help win large orders to make up for reduced margins.

However, the management stated that they do not want large orders.

Prefer holding a smaller, flexible order book to capture short-term opportunities.

This contradicts conventional strategy in a low-margin environment.

I’ve not read through the con-call, but if these are the answers that they are giving to the analyst’s questions, and almost all of which are contrary to what’s happening in the Industry then I feel that it’s a very serious governance issue. And I don’t know if people have taken notice of it or not, An Independent Director Resigned the company w.e.f May 16th 2025, which was before the FY25 results of the company. Now all these factors are now looking like very big red flags to me. Also why is it that only this company is facing such high Cashflow Issues (apart from this FY) when companies of similar size are not facing any such issues? And they’ve been talking about fund raise from some-time now and they’ve not raised any funds as of now, and with very low ROE and low ROCE they won’t be able to sustain such high growth rates going forward without actually raising money.

Indeed this is very helpful. do you have insights for RR Kable as well ?

Taxation was low during the period for R R Kabel, I think they have booked some type of losses in Q2FY24.

concerns regarding any top line based projections without considering OPM raised earlier by me:

I still don’t see any governance issues( apart from Tibrewala case) . If everything was good with the company then it wouldn’t be trading at a cheap valuation and hence less money to be made ![]()