I dont track Heritage in detail (I try to avoid DIRECT political connection companies ) .Having said that its a GOOD professionally managed company but regional focus unlike Parag (Pan India ) and also their VAP is less than Parag .

1 Like

Exactly. That is the reason why (I believe), Heritage is always undervalued in the market. As you said, its professional enough when it comes to mgmt. It faced multiple years of opposition governments (who considered him their enemy, as well). And it was regional which started spreading a couple of years back and is successful enough in spreading as of now, and expansion plans are going well, as guided.

Their VAPs are less vis a vis Parag, but they are fast expanding their VAP percentage, and with reasonable success and speed.

So, is the reason I feel, its undervalued.

I am looking for the reasons why one shouldn’t buy it at this price. I welcome negative views on Heritage.

6 Likes

@debashih ji Given your investment in Parag Milk Foods, I wanted to understand your perspective on the company’s corporate governance practices. There have been some observations around frequent management changes, communication transparency, and the company’s broad approach to product launches. Additionally, past regulatory issues such as income tax scrutiny and huge inventory write-off (from 2021 to 2023) have been noted in the forum.

From your experience and view, do you believe Parag Milk Foods has the governance strength and strategic focus necessary to be a reliable long-term investment? How do you assess the key risks, if any, and do you see the company as well-positioned for sustainable growth for long term to be a multi bagger? Your insights would be highly valuable.

1 Like

3 Likes

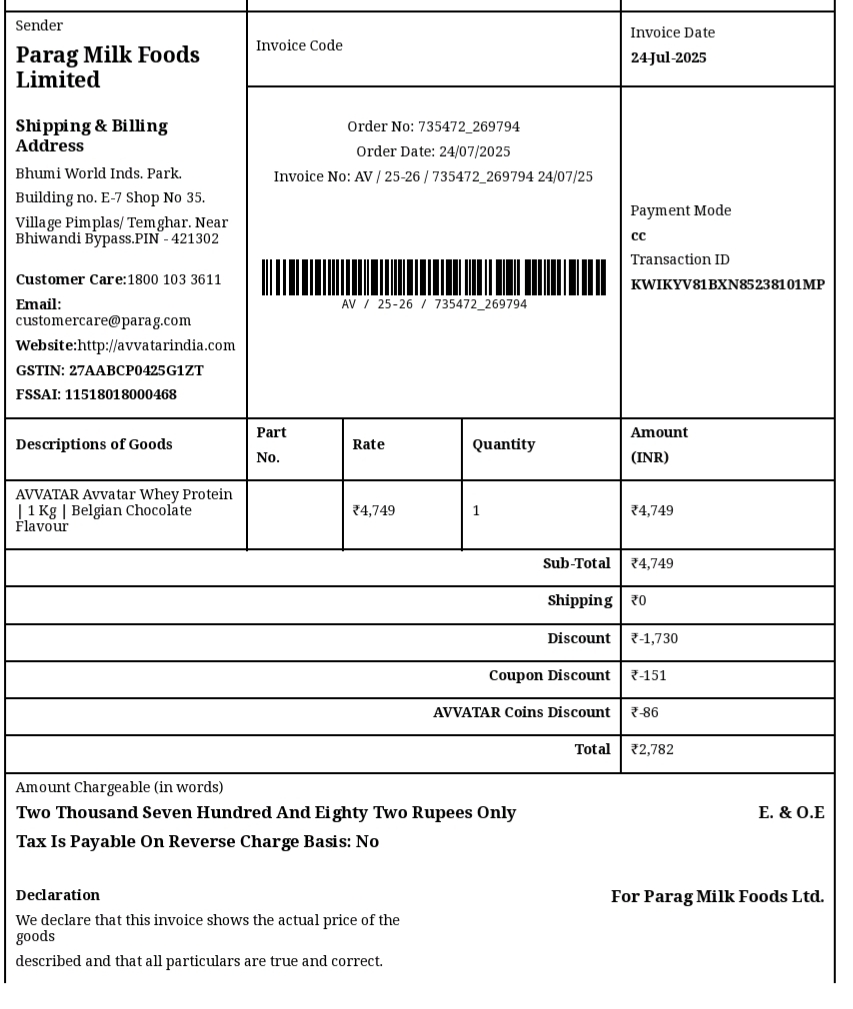

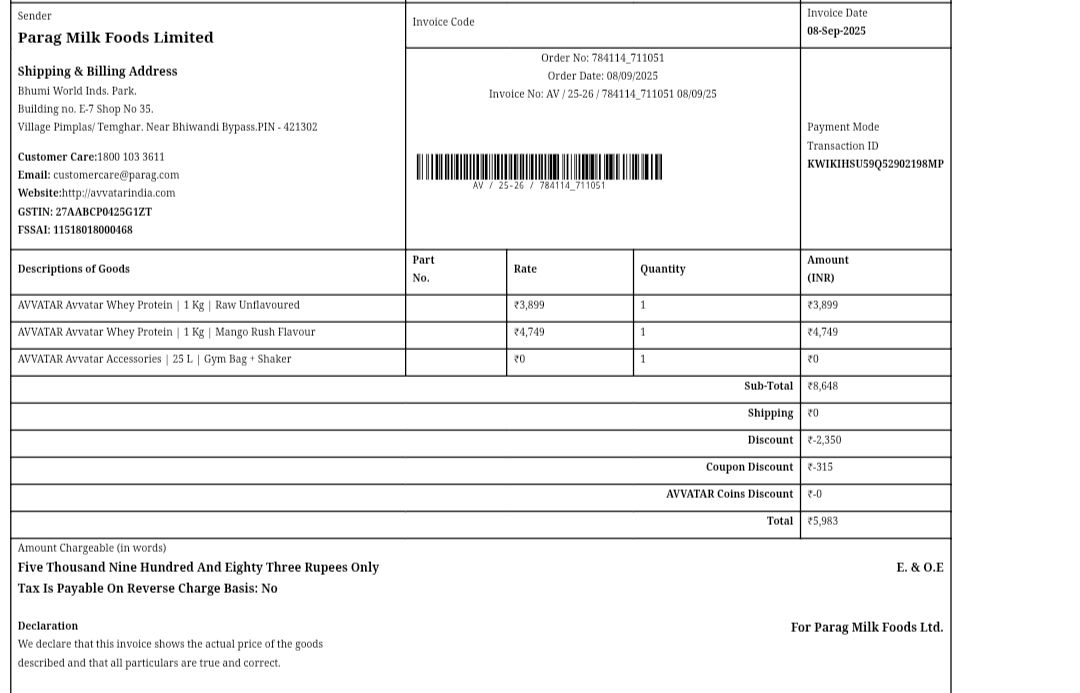

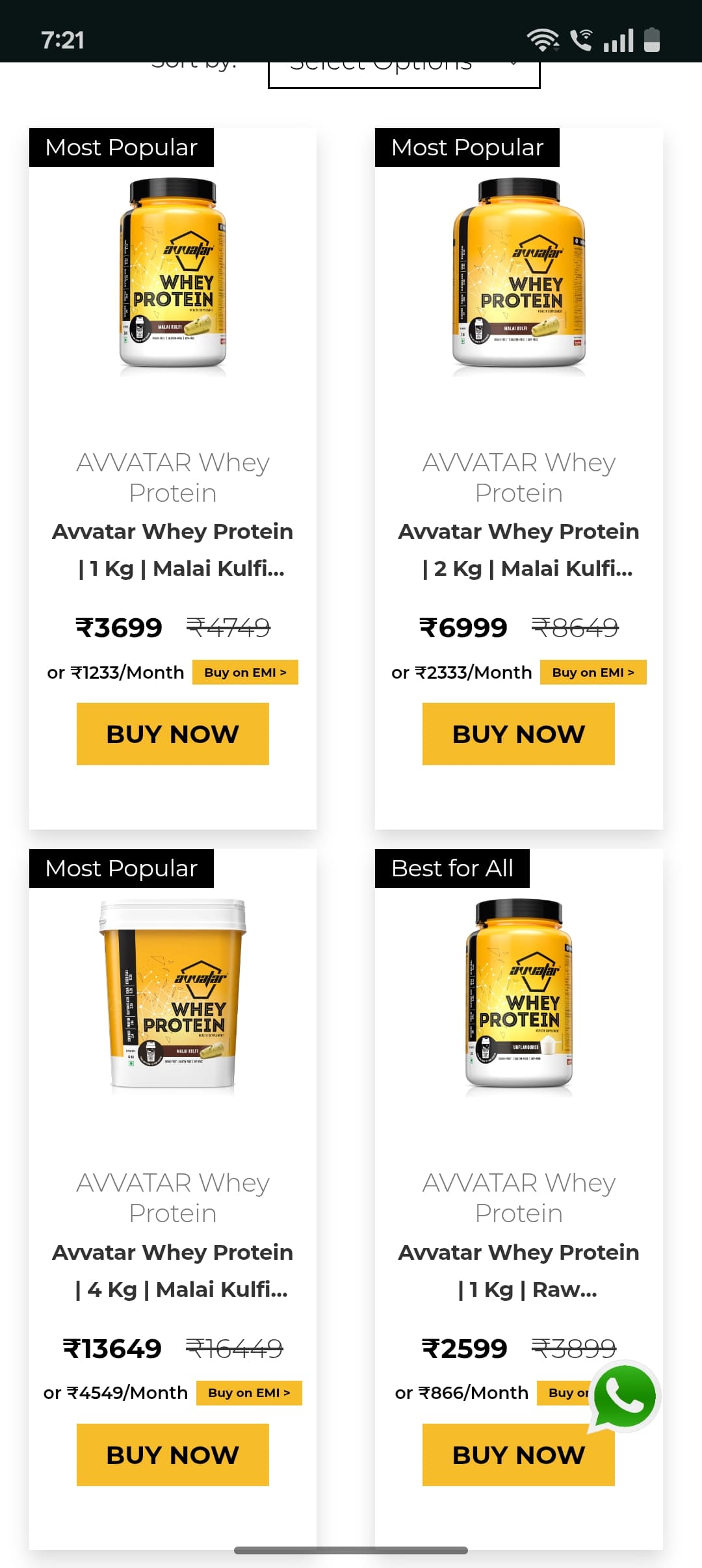

1)Sharing some digital scuttlebutt this is July 2025 bill and price

2)This is September 2025 bill sudden surge in price approx 25-30% , MRP is same but discount given is less

3)This image from taken from direct website

So lots of protein trend started in India , india is low consumption protein intake country’s,for GLP -1 story you can take proxy also.

In my opinion usually people don’t change their protein powder till the authenticity works so little switching cost might Play.

Disc invested in last 7 days ,not sebi register.

8 Likes

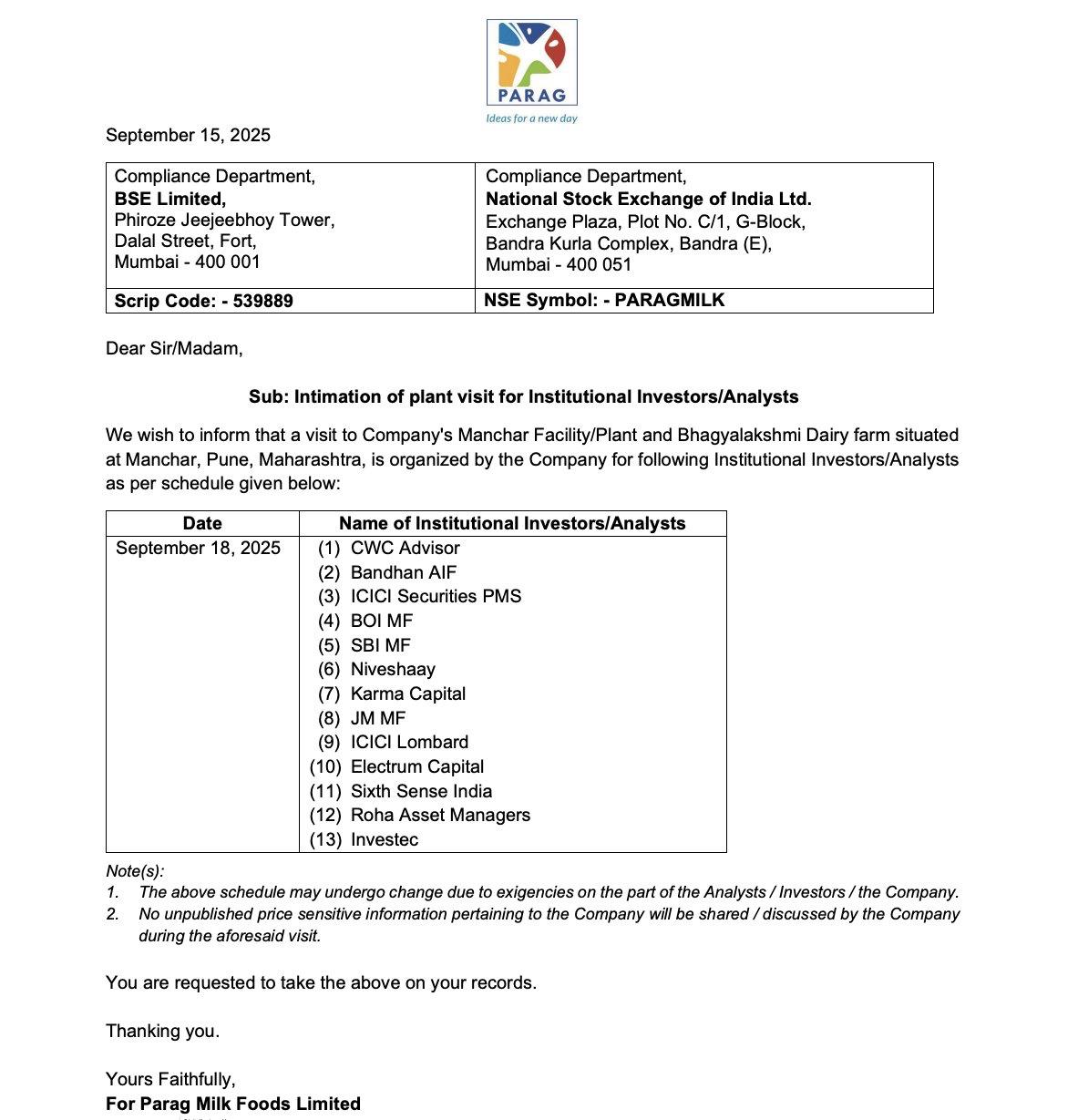

Big Investor group visited the dairy, looks like something is cooking. Stock has almost doubled in past 6 months. Any insights ?

Whey Protein is one of most popular at Amazon but it is not a substantial part of their revenue.

Disclaimer: holding tracking level position.

They have hiked their Protein Powder price already at par with Optimum Nutrition.

The Protein Bar price was hiked from 60 to 80. Believe 60 could just be introductory. At least the 5-6 Shops I buy them from tell me that they are outselling RiteBite Max Proteins.

I usually don’t like to do these kinds of investigations, but I consume Protiens Bar & Powder a lot & this is what I have observed.

6 Likes

@DEBASHISH Sir, if Parag Milk has such higher value added mix then -

- Why their gross margins are similar to other milk players and infact lesser than likes of Hatsun?

- Why was the value growth in value added categories so less in FY25 than the volume growth? Why could they not show pricing power and extract more value growth?

2 Likes

Parag buys milk from traders/collection centers → higher procurement cost.

Hatsun sources 100% directly from farmers → lowest milk procurement cost in India.

Procurement accounts for 60–70% of total COGS, so even a ₹1/litre difference massively impacts gross margin.

Hatsun’s massive scale in the South → better fixed cost absorption.

Larger plants, more SKUs, higher throughput → lower per-unit cost.

Parag’s scale is improving but not at Hatsun levels.

Hatsun has the strongest cold-chain + direct distribution network.

Parag still depends more on distributors instead of direct distribution, which:

increases channel margins

reduces pricing control

leads to higher return/expiry costs

Hatsun’s curd, ice cream, UHT milk have very high repeat demand + scale.

Parag’s cheese and whey are higher value but:

lower scale

underutilisation of cheese plant reduces gross margin

whey is still small and volatile

So the value-added mix helps gross margin but not enough to beat Hatsun.

Parag lost share earlier due to:

COVID disruptions

working capital issues

low distributor confidence

To regain distributors + retailers, they kept pricing stable while increasing discounts.

So volumes grew, but net realization per unit decreased.

Cheese pricing power was weak across the industry.

Amul launched:

low-price variants

bulk cheese at aggressive pricing

So Parag did not raise prices to avoid losing shelf space and food-service clients.

(C) Value Added Segment Was Pushed Through HoReCa (lower realisation)

Parag increased cheese sales in:

QSRs

Hotels

Bakery chains

HoReCa = higher volume, lower margin / lower realization.

Retail cheese demand was slow → food service dominated growth.

This reduces realization per kg, so value grows slower than volume.lowest procurement cost

highest distribution reach

high working capital capacity

dominant regional presence

Parag is improving but not dominant like Hatsun in:

South (curd, ice cream, UHT)

Amul in the West/North

Without regional dominance, you cannot increase prices.

Also:

Milk procurement prices were rising

Retail cheese demand was stagnating

Competition was aggressive

So they could not push price hikes.

—Because their value-added mix advantage is neutralised by:

(1) Higher milk procurement cost

Cancels 60–70% of the theoretical margin advantage.

(2) Under-utilized cheese capacity

Fixed costs spread over fewer units → lower margin.

(3) Higher discounts to revive distribution

Pulls value down.

(4) Lower realization in HoReCa

Bulk cheese = low margin.

(5) Weak North India distribution

Higher channel margin burden.

12 Likes

Thanks for sharing different pointers. I had similar mental model on milk players but thanks for putting it here.

Yes I have started investing in parag let’s see how does it goes company would selling products to dubai also through it’s subsidiary let’s see if margin expands as company is guiding for that

Your questions are very valid .Infact me and also market is looking for margin expansions .In my view their margins are lower because of :

- Higher procurement cost .Unlike the Southern players (bcos of concentration )where margins are higher bcos of efficient sourcing ,Parags sourcing is not efficient bcos of lack of scale like a national player like Amul .With increase in scale margin should improve .

- I feel their institution and HORECA contribution is very high where they may be charging much lower price which is bringing the overall margin down .

- They are the highest spender on A&P where they spend around 4.8 % of sales (huge given size ) compared to regional players hence if we add this and look at EBIDTA % Parag doesnt look that bad .With increase in contribution of Avaatar (margin is double )the overall EBIDTA ideally should move up.

On your second query ,if you look at core category their value growth now is actually more than volume growth .

11 Likes

Gowardhan Ghee:

➝ “commands 22% market share in the branded cow ghee segment”

Go Cheese:

➝ “commands 35% market share in the Cheese category”

Quarter Milk Inflation YoY Price/Litre

Q2 16% ₹38

Q3 20% ₹40

Milk industry has been facing issues - Parag milk also in the same boat. Ebitda is still good for parag milk

6 Likes

Parag needs to be spending money on Advertising. Right now the focus should be capturing market share as much as they can. Once they do that, then they can slowly increase their margins through price hikes and premiumization. 3 things that I am underwriting for an investment in this script

- Gradual revenue and profit growth - 15% for the next few years

- Margin improvement from 7% to double digit

- P/E to improve from 25 levels to 50-60 odd if they management to reach their FMCG aspirations.

While India drinks a lot of milk, value added products are lesser and these should allow for even faster growth. Highly linked to middle class expansion

2 Likes

#ParagMilk Q3 FY26 concall

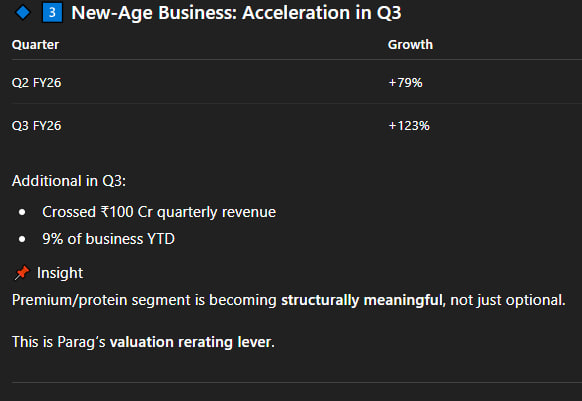

-New age business (Avataar & Pride of cows) now contribute roughly 9-10% of the overall revenue. Targeting to take it to around 20% in 2 years.

-Marketing spend is around 3.5-4% of revenue.

-Brand collaboration with Blue Tokai for Pride of Cows.

-Significant debt reduction will happen during this FY.

8 Likes

Disc: not invested

3 Likes