Overview

Par Drugs & Chemicals makes API’s & Fine Chemicals for domestic as well as Exports Market

Business

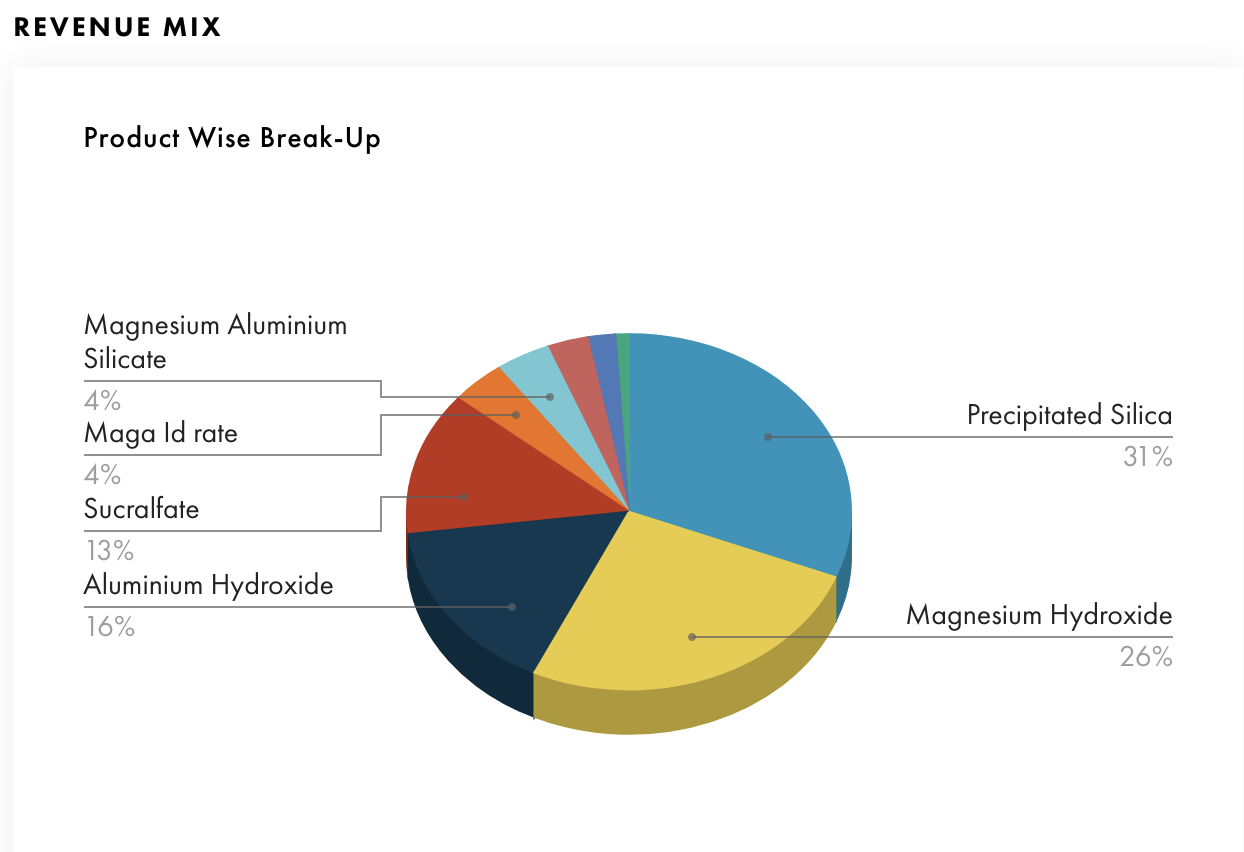

They have 2 business verticals namely - APIs & Fine Chemicals. 72% of Revenue comes from APIs & rest 28% from Fine Chemicals

APIs

In APIs the company makes APIs for Formulation Manufacturers. For example when a drug is formed their are many steps to it. First is KSM which is key starting material then comes your intermediate after that API and then at the end comes Formulation which is also called Finished Dosage.

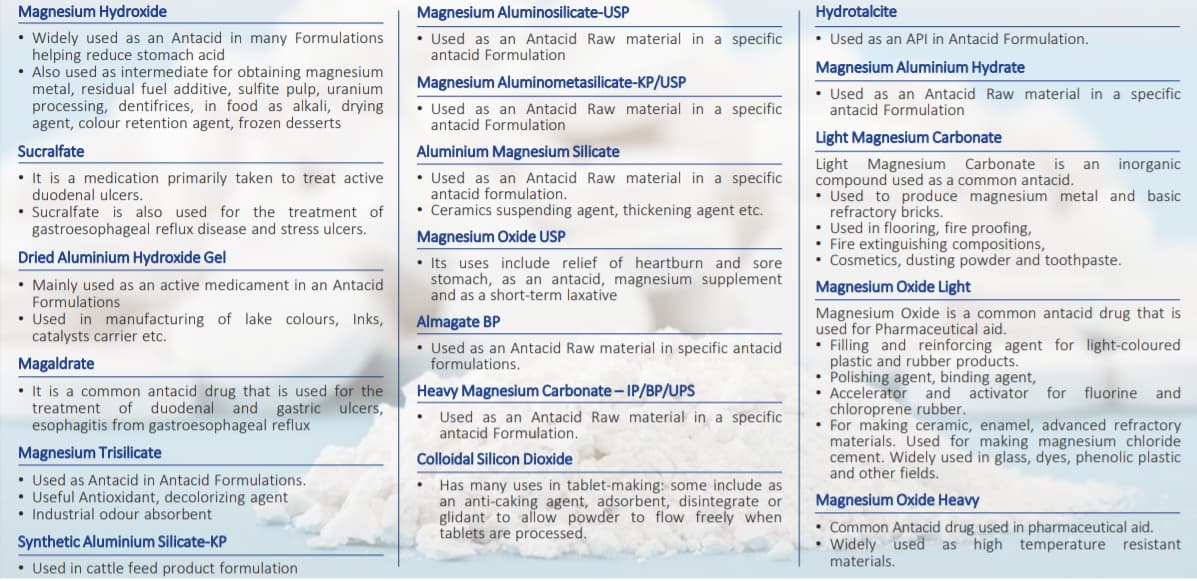

It has entire range of Antacid Molecules. Antacid Means a medicine that prevents Acidity. Currently they have around 18 APIs molecules , As follows-

The company is one of the largest manufacturer in Magnesium Hydroxide, Sucralfate and

Magnesium Trisilate in India. Their uses are stated above in the Image. So basically they are a End-to-End Antacid Solution Provider. With many APIs that cater to same segment.

Fine Chemicals

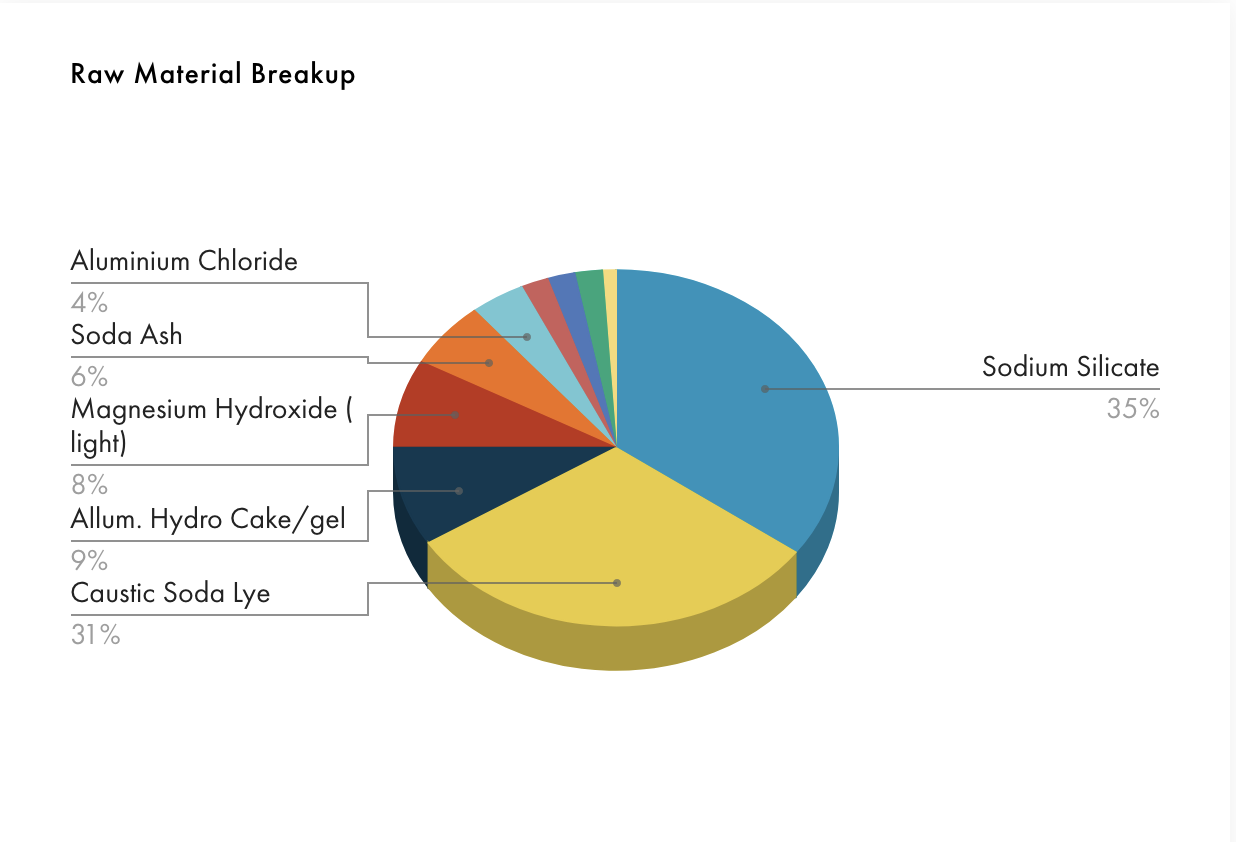

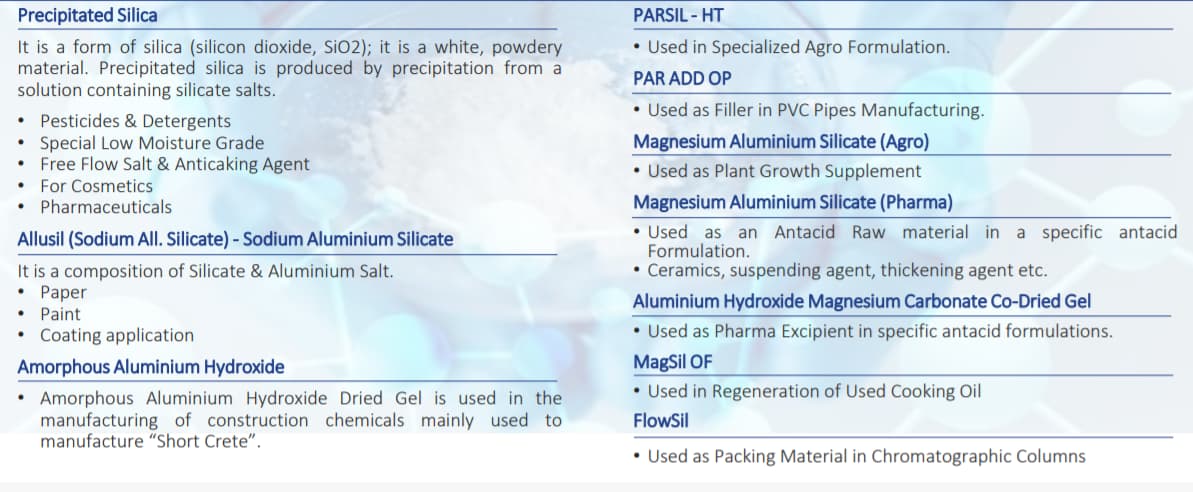

Coming to Fine Chemicals. Unlike APIs fine chemicals have uses in many Sectors such as Pharmaceuticals, Adhesives , Agricultural etc etc

Currently company has around 10 fine chemicals portfolio, Which looks like this -

As you can see they have variety of uses

Capacity

Company has around 9,700 MT Capacity in Bhavnagar for APIs, Fine Chemicals & Magnesium Hydroxide.

Company also doing a 1,400 MTPA Brownfiled CAPEX in 2021 , which will add put to their capacity

Customers

Company caters to around 132 Customers & Added 20 New Customers in FY21 .Its key customers include Essential Drugs Company, Pfizer, United Phosphorus, Cipla.

R&D

The company mentioned that its R&D Team is focusing on Chronic therapies like

antidepressants, anti-diabetic and anti-bacterial. This shows that they are also entering newer & newer Therapeutic Segments & Expanding their Product Portfolio.

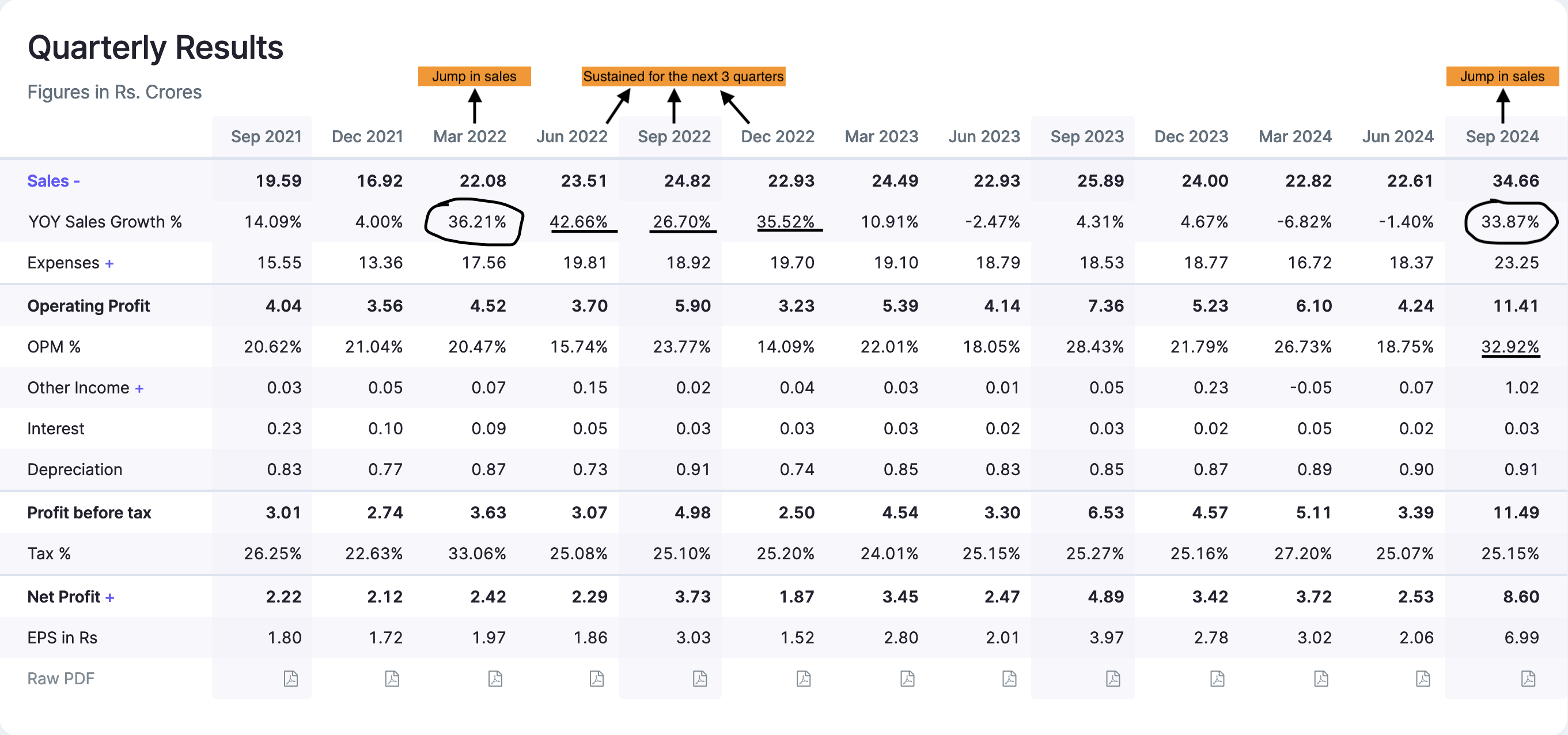

Financials

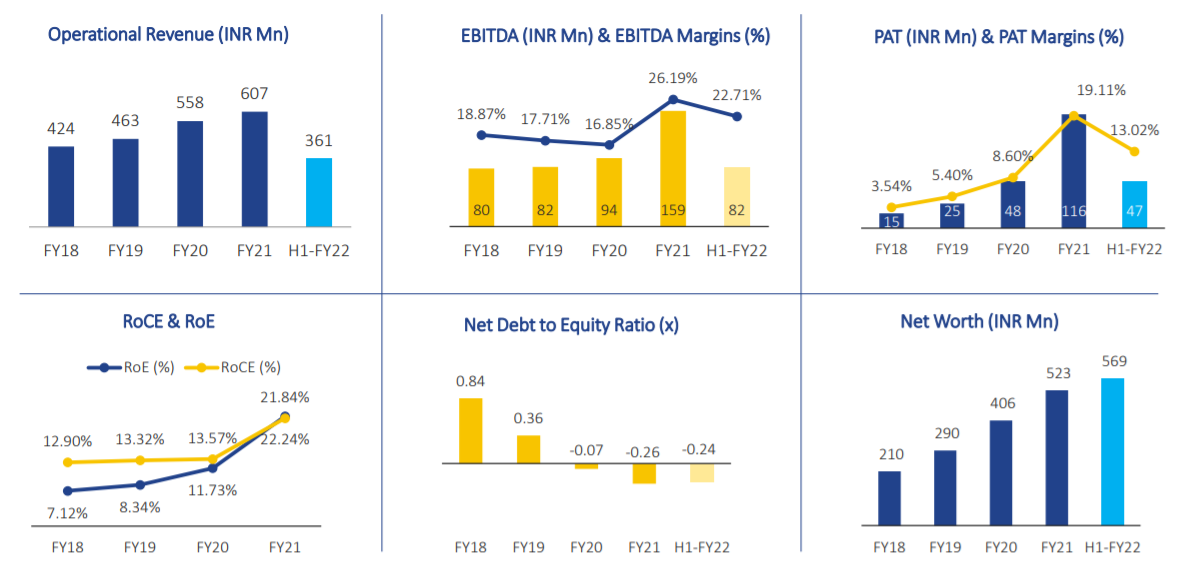

Financials as such looks good in FY21 Numbers -

EBITDA Margin - 26%

PAT Margin - 19%

ROCE - 22%

Risks

Risks in this business can be -

- Over Dependency on Antacid Products

- Lack of Execution of Management in terms of diversifying Product Portfolio & Capacity Expansion

Disclosure - Not Yet Invested

Here were my 2 Cents of the company. Thanks for reading & Giving your valuable time

Sources used in this Thread was Investor Presentation of the Company.

Link for it is this -