Panyam Cement as a stock investment idea came from came from AceInvestorTrader blog (link at the end). Coincidentally, SP Tulsian recommended it in the last few days (as I was compiling this post) and there was a management interview also (links provided below).

Date – 21.11.15

CMP – 79.65

Mcap – 128 cr

Book value – 14.9 (as on 30.09.15)

Enterprise value – 175 cr (Mcap plus total debt less cash, as on 30.09.15)

Basically, it’s a turnaround case. The plant was shut in Nov 2013 due to lack of power and was restarted only on 21.07.14. Sales and profits since then are showing some signs of improving.

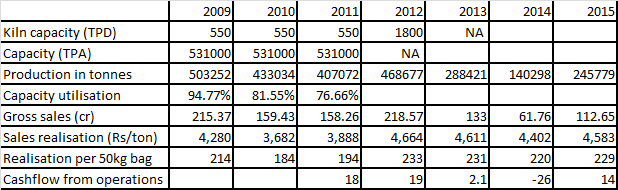

Its current capacity is not exactly known, however, they commissioned an enhancement in capacity from 550TPD in Kiln 1 to 1800TPD on 10.08.2011. The company reported capacity of 5.31 lakh tons per annum in their 2011 annual report (when their Kiln 1 capacity was 550 TPD), however stopped reporting the capacity thereafter. In any case, they haven’t been able to make full use of their capacity for one reason or the other.

The owners are part of Nandi group and I had read earlier that they had political affiliations. The MD however is an IIM Ahmedabad graduate and is said to be running the company professionally.

The company is based in Telangana region which is expected to witness very high demand given the planned infra development activities (there are several new bits regarding how this region is expected to attract lot of demand, so this bit seems plausible). In addition, it also sells in neighbouring states like Goa, Karnataka. It has access to limestone mines close to the plant.

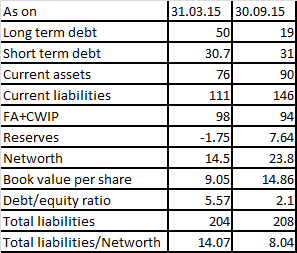

Following information is compiled to indicate that turnaround is taking roots:

Point 1:

Reduction in debt and debt equity ratio is positive. Though it is still high at above 2x. Total liabilities to networth is uncomfortable

Accretion to reserves is also positive.

Current assets have reduced (ex cash), and current liabilities (ex short term debt) have increased, which taken with profits, reduction in debt and depreciation, shows cashflows are improving.

They had 25 cr of CWIP as on 31.03.15, which seems to have come down to 20 cr as of Sep’15 which indicates some capex is on – either balancing equipment or debottlenecking or some such. 2015 annual report had a figure of 4 cr under Estimated contracts remaining to be executed under capital account (Rs 6 cr as on 31.03.14).

Point 2:

Pledged shares are down a lot and promoters are slowly buying shares from market (albeit marginal). There was one internet link which had compiled information (it was a paid site) for potential acquirers. However, acquisition (ie promoter selling out) is not a part of my thesis yet.

Historical data:

Some historical financial and production data:

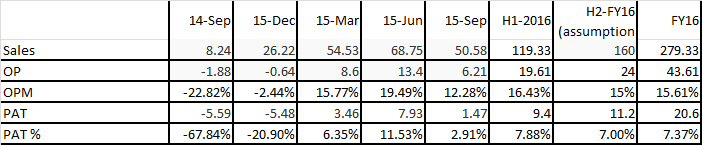

Recent Quarterly trends:

Some recent Quarterly data, which indicates improvement in financials:

Management says they will achieve 160 cr sales in H2-FY16 compared to 120 cr in H1-FY16, which looks possible.

They say that they will produce total 8 lakh tons in FY16, which works out to approx. 175 Rs per 50 kg bag, which considering current prices of anywhere from 250-300 Rs per bag, looks conservative and achievable.

They also say margins would remain in line with 1st half of the year. Assuming margins as given in the table, expected net profit in FY16 is around 20 cr, and current market cap is 128 cr.

Some Negatives in financials:

There are huge statutory liabilities under dispute shown as contingent liabilities (eg. IT claims of 42cr, Excise claims of 11 cr, Royalty delays penalty 13 cr etc). If these become payable, then the company would be bankrupt.

There is a component of interest received of 5 cr in 2015 (4.3 cr in 2014) which is included in the profits. Sustainability (genuineness?) of this is unknown.

The company had taken unsecured loan from promoter of 35cr in 2014 (the amount as on 31.03.14 was 41 cr) which came down to 30 cr as on 31.03.15. Why are promoters taking out money, when it could have been used to repay more debt.

Significant related party dues within the group – eg. 60 cr given to associate company as deposits/advances, corporate guarantee on behalf of group companies of 220 cr etc

These are significant figures, on which there is no clarity.

Concluding remarks:

I admit, this would appear as a leap of faith kind of stock.

It corrected 20-25% after Q2 results, which I was not very happy with, especially the profits. However later it struck me that Q2 is monsoon quarter, and in such a period, if they have done sales which is just 25% below the Q1 figure, then it is actually quite decent.

Given presence in Telangana, cement demand being especially good in 2nd half of the year, access to limestone mines close by, some bit of capex going on, reduction in debt, increase in promoter holding, reduction in pledged shares, near term prospects appear good. Part of it seems to already be in the price, but if they continue like this even in 2017, then it could really turn out to be cheap at this price. This would need close monitoring and hence current allocation cannot be high.

Disclosure:

Taken starter position at 60, added a bit recently. However it’s a very miniscule portion of my PF allocation as yet.

Links and other info:

http://bullseye.in.com/video/stocks-views/positivepanyam-cements-target-rs-125-tulsian_4190881.html

http://www.panyamcements.com/panyam%20files/Annual%20Report%20Final-2014-15.pdf

http://www.sebi.gov.in/takeover/panyamloo.pdf

http://www.researchandmarkets.com/reports/2775378/panyam_cements_and_mineral_industries_ltd#rela0