Hello Investors,

I am creating this post since could not able to find a dedicated thread on Panchsheel Organics Ltd. (POL).

Industry Overview

• Panchsheel Organic Ltd. operates in the pharmaceutical industry.

• The current market size of this industry is ₹ 543 lakh Cr. (US$ 65 billion). India’s

pharmaceuticals industry is expected to reach US$ 130 billion by 2030, and US$

450 billion by 2047.

• During FY18 to FY23, the Indian pharmaceutical industry logged a compound

annual growth rate (CAGR) of 6-8%.

• Major competitors of POL are Hikal, Aarti Drugs, Gujarat Themis Biosyn, etc.

Company Overview

• Panchsheel Organics Ltd is a manufacturer of Bulk Drugs and Intermediate.

• Panchsheel an ISO CERTIFIED, GMP (Good Manufacturing Practices) approved, maintaining WHO Standards, a public listed company (listed on BSE) are manufacturer and exporter of Active Pharma Ingredients (APIs), Intermediates & Finished Formulations (both Human & Veterinary) having a wide experience of more than three decades in the healthcare field.

• The company has its corporate office in Mumbai and has two multipurpose manufacturing unit is situated in Indore (120 TPA to manufacture APIs) and Pithampur.

Products Categories

• Bulk Drugs & API Intermediates

• Steroids & Hormones

• Pharma Pellets of all ranges with different potencies.

• Pharma Formulations (Finished Products).

• Veterinary Products

• Agri Biotech products. (Bio Fertilizers, Bio Stimulants, Growth Promoters)

• Probiotics & Enzymes

Capex Plans

Phase 1:

- This capex plan is comprised of ₹ 40 Cr. at Pithampur, Indore (MP) for Probiotics & Enzymes.

- Capacity of 36-40 TPA.

- The funds were sourced through a mix of preferential allotment and warrants in September 2022 and the remaining done through Internal Accruals.

- Revenue potential is around ₹40-50 cr. once the full capacity is available in FY25.

Phase 2:

- This capex plan is comprised of an initial investment of ₹50-70 Cr. at DMIC Vikram Udyogpuri Biotech Park Near Indore (MP) for fermentation-based and API-based pharmaceuticals.

- Capacity for fermentation-based pharmaceuticals is around 36-40 TPA and for API-based pharmaceuticals is around 120 TPA.

- The funds were sourced through a mix of preferential allotment and warrants, Internal Accruals, and Debt/Equity (if needed).

- Revenue potential for fermentation is around 40-50 Cr. and up to 100-120 for API.

Corporate Actions

• The company has issued and allotted 17,75,950 Equity Shares on a preferential basis in September 2022.

• The company has also undertaken the bonus issue of shares in a 1:1 ratio in December 2021.

• The company is very regular in dividend payments with an average of 12-15% over the last 10 years.

SWOT Analysis

Strength:

• Very low debt (6 Cr. 3.7% of Balance Sheet).

• Constant growth in revenue and net profit.

• The pharma industry is expected to reach 130 billion US$ by 2030 which is currently at 65 billion US$ (More potential for revenue and profit).

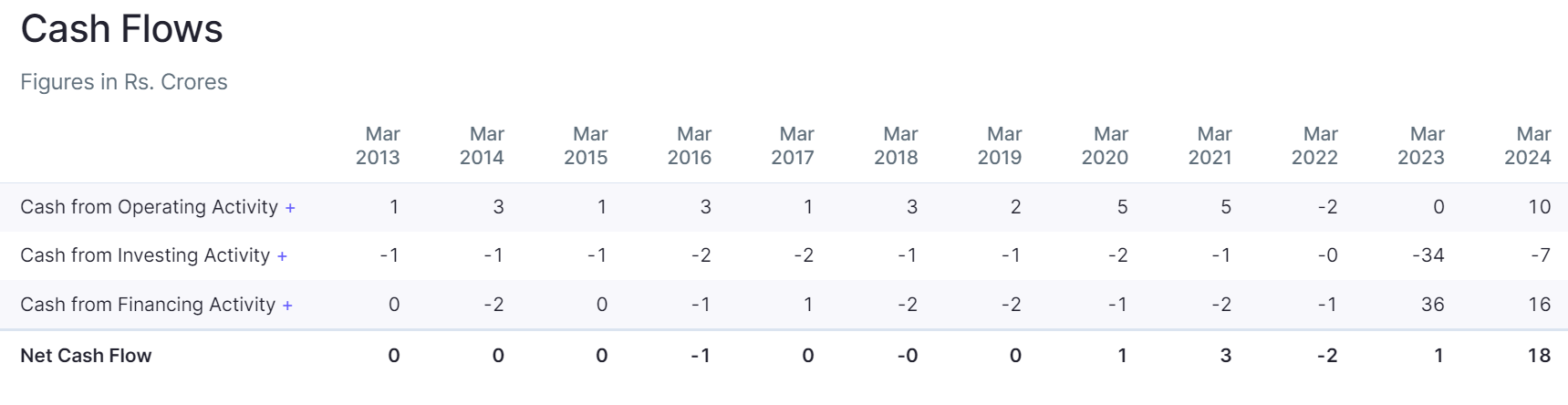

• Rise in Cash Flow from Operation activity.

• Zero promoter pledge.

Weakness:

• Decrease in RoE (17% to 13%) this year.

• Decreases in RoCE (27% to 17%) this year.

• Dependency of products on the availability of raw materials.

Opportunity:

• Upcoming Capex plans help to generate more revenue and net profit.

• The Company has a wide range of pharmaceutical products in its portfolio.

• Export market opportunities.

Threat:

• Continues decrease in promoter holding.

• Rise in the cost of raw materials.

Key Clientele

• Swiss Granier Life Science

• Abbott

• Madras Pharma

• Akums

• Zydus

• Hetero Healthcare

• Ajanta Pharma Limited

• MacLeod’s Pharmaceutical Ltd.

• Aristo Pharmaceutical Pvt Ltd.

• Intas Pharmaceutical Pvt Ltd.

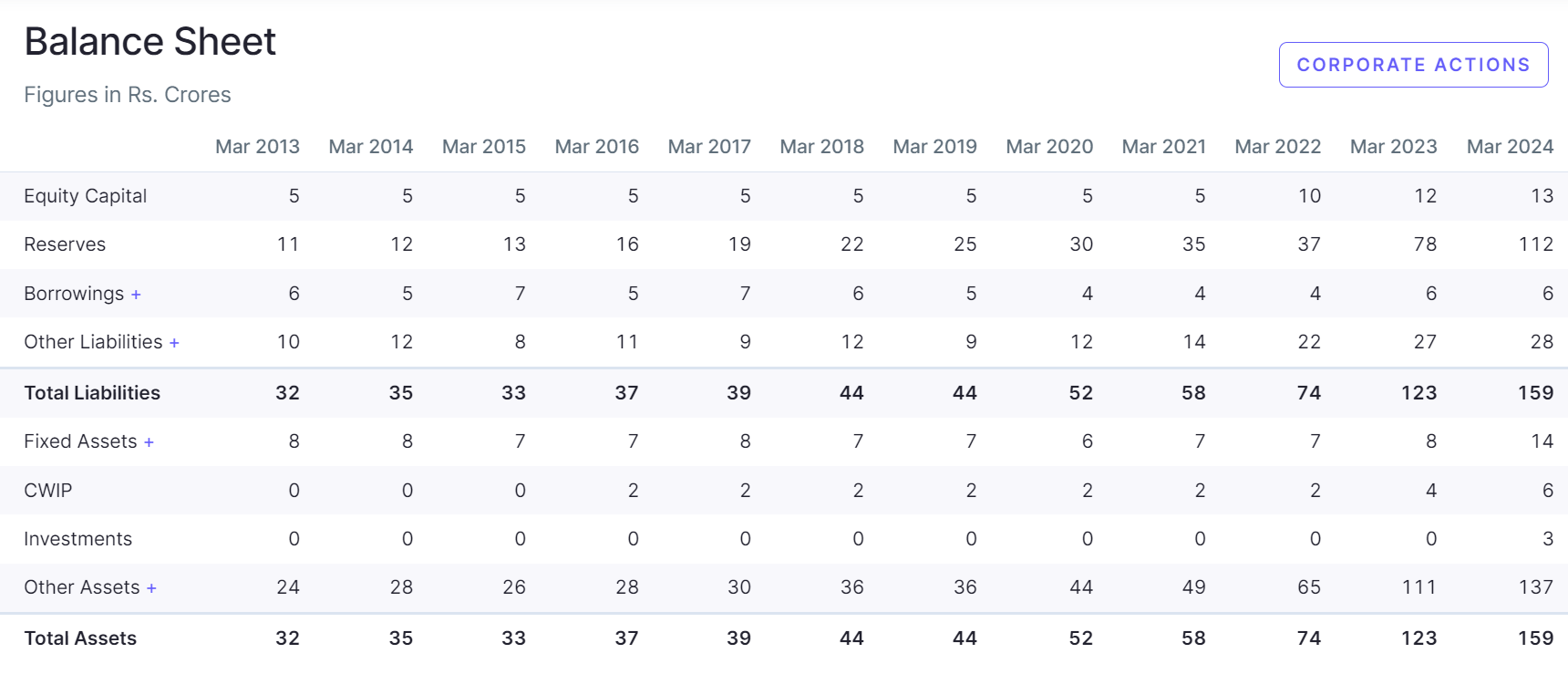

Key Financials

• Market Cap - 331 Cr

• Current Price - ₹ 281

• High / Low - ₹ 288 / 160

• Stock P/E - 23.4

• Book Value - ₹ 106

• ROE - 13.1 %

• ROCE - 17.4 %

• Price to book value - 2.64

• D/E – 0.05

• EPS – 11.98

• Promoter Holding – 56.12%

• Sales – 105 Cr.

• PAT – 14 Cr.

• Balance Sheet – 159 Cr.

• Borrowings – 6 Cr.

• Working Capital – 79 Cr.

Incorporating the key financials of the Panchesheel Organics Ltd.

- Profit & Loss

- Balance Sheet

- Cash Flow Statement

Disclosure: I am invested in Panchsheel Organics Ltd. and this is not an investing advice. Please do your own due diligence before investing.