Hi Reposting this as i had just given a link which the moderator asked me to copy paste.

Disclaimer: I had personally invested here at 36 rs.

Introduction:

This stock was first introduced to me by a friend who goes by the weird pseudonym of MunkthePunk on the money control board. As we collectively deep dived into this stock we unraveled a slew of triggers that has the potential to substantially rerate this stock. This note is a logical representation of our discussions on this stock in particular and on the steel industry in India in general. Since I have already disclosed who is the culprit in unearthing this stock a statutory disclaimer to begin with - If it transforms into a multibagger - as we think it would, the credit is mine and if things do not turn out as expected you know whom to blame.

On a serious note now let us start with the analysis:

Something about the Company:

First a cut copy paste about the company from their site for those who are too lazy to visit the Panchmahal site

With 40 years of special steel making experience, Panchmahal Steel is a leading producer of Stainless Steel long products in India. With a dedicated focus on Stainless Steel & fully integrated facilities from steel melting to cold finishing, we offer a comprehensive range of Stainless Steel grades, in hot rolled wire rod & bars and cold finished bars & wires.

Panchmahal’s state-of-the art steel melting facility includes an ultra-high powered 50 metric ton electric arc melting furnace, AOD convertor, ladle furnace for superior steel refining and continuous casting.

Facilities for cold finished bars & wires include coil-to-bar drawing & bar-to-bar peeling lines, heat treatment facilities, shot blasting & pickling lines and spooling, cutting & stamping lines for Stainless Steel welding products.

We offer Stainless Steel in Austenitic, Martensitic, Ferritic, Duplex and low nickel - high manganese (200 series) grades.

Panchmahal’s core strength lies in its ability to meet customer’s unique requirements. Our fully integrated facilities enable us to produce Stainless Steels with various modified chemistries for customer specific applications.

With ever changing market dynamics, Panchmahal is equipped to provide customized products and services for global markets, for volume as well as for specialty niche market requirement.

Here is their Corporate video presentation:

They make Stainless Steel in fully integrated facilities from steel melting to cold finishing and offer a comprehensive range of Stainless Steel grades, in hot rolled wire rod & bars and cold finished bars & wires.

They have three products:

- Stainless steel wire rods and bars.

- Stainless steel wires

- Stainless steel Welding Wires

The product specifications can be found in Panchmahal Brochure Link given below:

Links:

http://www.panchmahalsteel.co.in/Panchmahal_brochure.pdf

Applications of their products are in: -

Architecture, Building & construction Hot forgings Surgical Instruments

Automobile Components Machining Thread Rolling

Ball bearing Oil and Gas Industries Welding

Bar and Wire Drawing Pump and Valves White Goods and Consumer durables

Braiding Refractory Anchors Wall Ties

Cold heading and fasteners Screens and Filters Wire Mesh

Food Processing equipment Spokes Wire Ropes

Heat resisting applications Springs

Deciphering the sales potential - Volumes

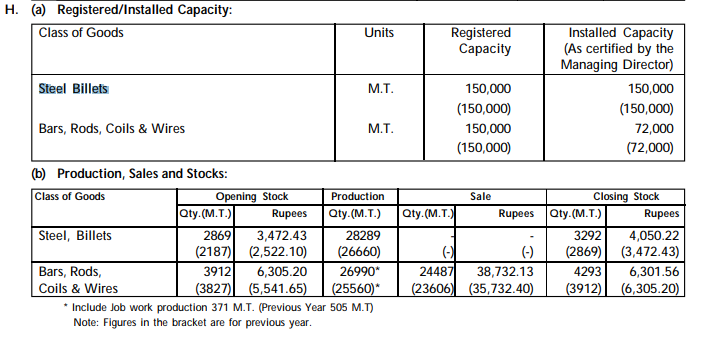

• Total capacity is 72,000 TPA out of their plant at Panchmahal , Gujarat

• The above data is a clear enough indication of the abysmal state of the steel industry in India where the capacity utilization was just 27 %. Now the question that needs to be answered is what lies ahead. There are winds of change blowing in the steel industry (Similar to what happened a few years back for the cement industry) which clearly points to a rosier future. Here are some data and facts.

The Indian steel demand- supply is expected to tighten significantly:

The Supply constraint:

• No new steel capacity creation has come about in the last 3 years due to the deteriorating global steel industry environment and the abysmal financials of steel companies reeling under mountains of debts.

• Given the 3-4 year lead time to add steel capacities no new capacity should be available till at least FY 2022.

The demand outlook – Major triggers:

• Turnaround in the Investment cycle: The investment cycle in India is expected to pick up in the coming two years. The Steel demand growth which crashed to 3 percent over FY 2013-2017 is expected to climb up to 5-7 percent growth for FY 2017 - 2022.

Links:

• National Steel Policy: The Government is focusing on increasing domestic procurement in public sector projects going forward through its new National Steel Policy.

Links:

Indian steel companies set to get a boost from GAIL’s local sourcing policy 08 Jun 2017 Steel GAIL, Steel

Prime Minister Narendra Modi’s Make in India mission received a big boost when state-owned GAIL India issued a tender for a Rs. 3,000 crore pipeline project giving preference to domestic steel companies, which have been badly hit by cheap imports from China, said a report.

• Anti- dumping policy: Anti-dumping duties are now being imposed by the Government to spur domestic production:

Links:

• GST – Low GST on raw material and transport costs: Steel industry is likely to benefit from the new GST rate for steel which is at 18%, with key inputs like coal, iron ore marked at 5%, which is the lowest slab under GST, could help to lower input costs. Together, with a substantial slash in transport costs due to unified and standard tax rate under GST, this is likely to help steel companies reeling under large debt and also keep steel prices stable.

Links:

http://www.steel-360.com/mag_iss_view.php?date=2017-06-01

• Affordable Housing, Construction, and Infrastructure: The Governments affordable housing program will spur demand.

Links:

http://economictimes.indiatimes.com/industry/indl-goods/svs/steel/higher-spends-on-affordable-housing-transport-to-boost-steel-usage/articleshow/56917729.cms

The demand – Supply end result:

• The demand supply should tighten significantly going forward with increasing demand, restricted supply and tightening imports.

• What this means is that the capacity utilization which is presently a measly 27 percent in FY 2016 should go up substantially till FY 2019. In fact, the projection is of the steel industry reaching up to 90 percent plus capacity. This means that Panchmahal has the potential of reaching up to a capacity of 65,000 - 68,400 tonnes till FY 2019.

Deciphering the sales potential - Prices

• For 12 months ending March 2016, the company sold 19,737 ton (27% capacity utilization) for 314cr, average realization was approximately INR 1,65,000 per ton, which means using the average realization price, they had the potential in March 2016 to achieve a sales of Rs.1145 crores at full capacity utilization.

• The anti-dumping duties which we elaborated on above have put a floor on steel prices and margins. With the steel industry reeling under massive debts it is improbable that the Government will reduce the protection of steel anytime soon.

• Current average realization of the products is around Rs.2,65,000/- per ton (US$ 4112 per ton).

Deciphering the cost of production

• Let us have a look at the raw materials consumed by Panchmahal:

Scrap billets, Nickel and Ferro Chrome are the main raw materials:

• 70% of it is imported:

• The breakup of the raw material costs:

• Ferro chrome prices could rise signaling a risk, however there are no visible supply constraints. Nickel prices are slumping due to weak demand. Steel billet prices are in a downward trend. The raw material cost trends needs to be monitored closely as they are very volatile.

Links:

http://www.moneycontrol.com/news/business/economy/no-need-to-cap-iron-ore-prices-plan-to-expand-output-govt-2302273.html

https://www.metalbulletin.com/Article/3708365/GLOBAL-BILLET-WRAP-Prices-fall-amid-mixed-market-signs.html

The promoters pedigree / Shareholding pattern

• The company has been in this game for the last 40 years.

• Promoters stake is a very healthy - 70.79% indicating strong promoter confidence.

• Promoters have been increasing their stake since December 2014 at a steady pace. Main promoter Ashok Malhotra further increased by 3.23% as per March 2016 SHP.

• There has been no equity dilution since 2013.

• However presently 36% of the promoter’s stake is pledged. With long term debt virtually repaid it is a matter of time before this pledge is removed.

• The Asset Reconstruction Fund (ARC) have reduced their holding from 21.14% in March 2012 and currently holds 4.14% of shares (equivalent to 8 lac shares), which they are keen to cash out of.

• The equity is size is 1.97cr shares only out of which promoters hold 1.39 crore shares.

• Only 21.15 lac free shares available as per March 2017 SHP.

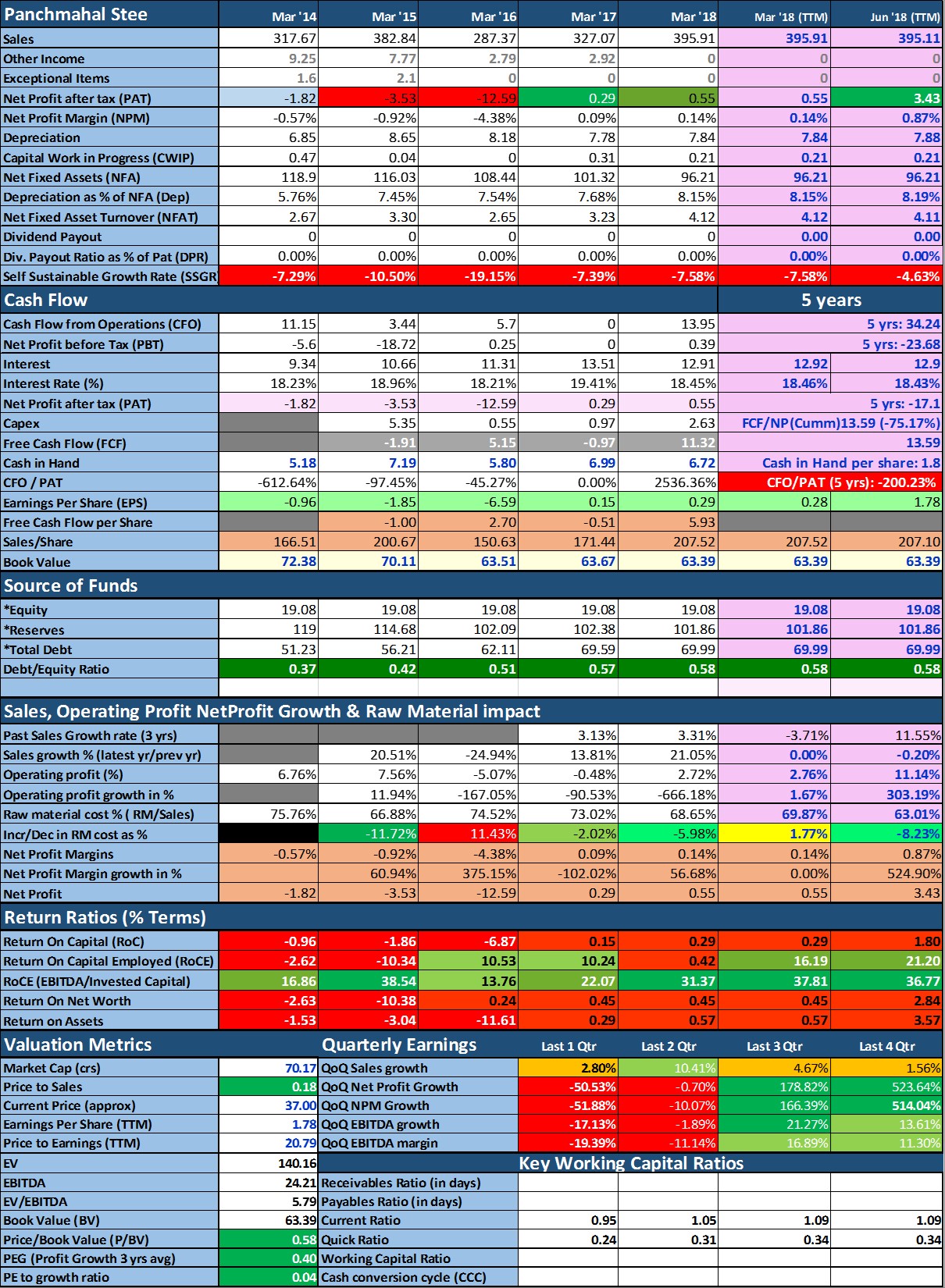

The Financials:

• Let us do a comparative analysis of their financials to see where Panchmahal is placed.

Financials as on March, 2017

All Figures in Rs. Crores

• From the above it can be seen that Panchmahal is in a much better shape than its peers.

-

It is already in the green and showing some profits

-

Its debt / equity position is much lighter

-

Out of the total debt of Rs. 69.58 crores, Long term debts comprise of just 8.55 crores, while short term borrowings are 61.03 crores

-

Debt / EBIDTA levels and Interest cost / EBIDTA levels are very comfortable and way stronger than the peers.

-

The latest update is that Panchmahal has entirely paid off its long term loan and the promoters pledge can be released - it is only a matter of time.

-

The performance of Q4 has been exemplary and the operating margins are on the way up and was 6.36 % in Q4 of FY 2016.

-

Some of the factors that affect input costs such as iron ore, chrome, coal and power supply are down currently and government is ensuring that the supply of these remain smooth for steel industry. This will enable to have better margins with a positive impact on eps.

-

With long term loan paid, interest costs will come down to almost nil thereby giving positive impact on eps.

-

Specialized Steel products demand is expected to remain stable considering rising demand within the country owing to focus on various industry segments, such as affordable housing, warehouses, buildings, roads and infrastructure, automobiles, etc.

The Valuation game

• Let us do a comparative analysis of their financials to see where Panchmahal is placed.

Financials as on March, 2017

Parameter Data Assumption set

Investment price Rs. 36 – 39 Current market price

Current Market Capital Rs. 72.50 crore Market capitalization as on 14/06/2017

Target holding FY 2020 Based on steel upswing cycle elaborated above

Target capacity utilization 90% Based on projected capacity utilization in steel by 2019

Average market price per ton * Rs. 265,000 Conservatively at Current market price even without assuming price upswing

Average sales Rs. 1,717 crores 64,800 tonnes at average realization of Rs. 265,000 per ton

EBIDTA margins 10% March 2007 they had achieved EBIDTA margin of 10.8%. With better sales realization, operating leverage and stable costs of raw materials a 10 percent EBIDTA margins possible

EBIDTA Rs. 172 crores Assuming a target sales of around 1700 crores and EBIDTA margin of 10 %

Profit after tax Rs. 100 crores Negligible debt

Plants mostly depreciated

EPS Rs. 50 – Rs. 52

PE 10 -15 Reflecting sectoral peak, negligible demand

Target price range at peak capacity utilization Rs. 500 – Rs. 750 Targeted price in FY 2020 at peak capacity utilization

Targeted upside at peak capacity utiliization 13x – 20x

Even if we assume a conservative capacity utilization of 60% to 70% there is a significant upside to this stock. At peak valuations in 2008 it had reached 325 plus. If the steel sector upswing actually goes per expectations we may expect an encore performance.

• The Net Current assets today are Rs. 8.77 crores. The Current assets (including cash) are more than enough to cover their Short term borrowings of around 61 crores.

Risks and concerns

• Delays in start of the Investment cycle in India.

• Variations / Increase in the cost of raw material prices.

• Promoter pledge of 36 % (expected to be released)

• Change in Government policies e.g. removal of Anti-dumping restrictions (not foreseeable for the next 2-3 years)

Conclusion

Panchmahal Steels is a safe bet to ride through the upcoming steel industry upturn. The steel industry is today at a similar cross roads where cement industry was 5 years back. With the whole industry weighed down by debt ridden companies, Panchmahal Steel with its comfortable debt status is a safe horse to ride through the cyclical upturn. Investors can consider putting up to 5 percent of their portfolio in here. However, it has to be played for its entirety of 3-4 years to secure maximum benefits.

!

!