About:

Panama Petrochem, started in 1975 in Gujarat, is one of the leading manufacturers and exporters of petroleum specialty products across 80 different variants. The products are vital for various industries like inks and resins, textiles, rubber, pharmaceuticals, cosmetics, power, cables and other industrial purposes.

Products:

White Oils - Pharmaceuticals, Personal Care and Food Packaging - Bulk

Petroleum Jelly - Pharmaceuticals and Personal Care - Bulk

Transformer Oils - Power - Bulk

Ink & Coating Oils - Ink and Resins - Speciality

Rubber Process Oils - Rubber - Speciality

Textile Oils - Textile - Speciality

Industrial Oils - Other Industries - Bulk

Automotive Oils - Automobile - Bulk

Drilling Oils - ONGC & International Drillers - Speciality

Waxes - Other Industries - By-product

Manufacturing Units:

It has built state-of-the-art manufacturing and storing units in Ankleshwar (Gujarat), Daman (UT), Dahej (Gujarat) and Taloja (Raigadh). Ankleshwar also has an DSIR (Department of Scientific and Industrial Research) approved R&D Centre. Exporting to global clients in every continent, they have set-up a full-owned subsidiary in Ras Al Khaimah, UAE under the name ‘Panol Industries’, enjoying logistics advantage towards GCC and MENA regions. The manufacturing capacity, in sum total, in Indian units is 240,000 tons, which is at 100% utilization and the UAE unit has 40,000 tons which is also at a 100% utilization.

Financials: as on 25th December, 2021

Mcap – 1487cr

CMP – 245.85 (FV – 2)

March, 2021 EPS – 22.37

P/E on March, 2021 EPS – 11 (Median P/E – 11.8)

TTM EPS – 38.54

P/E TTM – 6.37 (Highest P/E – 24.9 when EPS was 8.98)

Book Value – 111 (P/B – 2.21)

PEG – 0.16

Mcap/Sales (March,2021) – 1.02

Dividend Yield – 0.81%

5 Years CAGR on Consolidated Basis –

Sales Growth – 14%

Profit Growth – 40%

ROE – 16%

ROCE – 22%

OPM – 13%

NPM – 9.35%

Debt to Reserves – 0.07

Debt to Equity – 0.07

Fixed Assets – 192 (58 in 2012 and 173 in 2020)

Cash Conversion Cycle – 94 days

WC – 89 days

CFO from March 2012 to March 2021 – Positive in 21, Negative in 13, 15 & 19

FCF Average March 2012 to March 2021 – 10.85cr

Promoters Holding – 72.13

FIIs – 3.35

DIIs – 0.02

Investment Thesis:

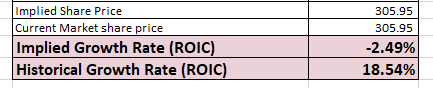

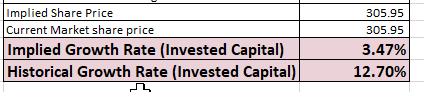

Valuation – This is a no brainer. All the metrics suggest decent valuations, if not undervalued in comparison to its peers & industry, and with the growth outlook guided by the management, it seems to be a good margin of safety at these levels.

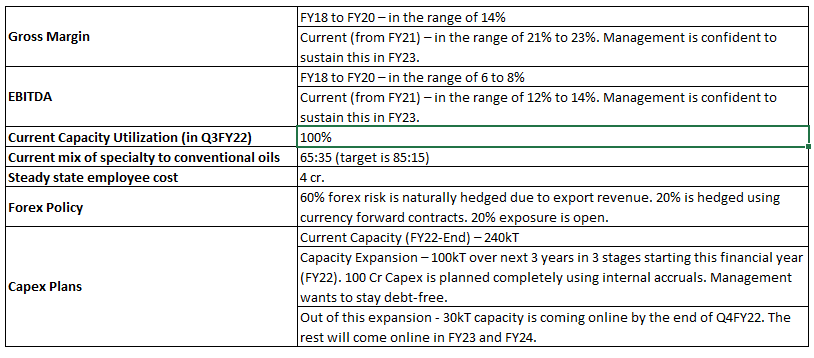

Capex driven by Demand – The company is utilizing more than 100% of its capacity at Indian units (257,000 tons against capacity of 240,000 tons) and with the rising demand for its speciality and value-added products, the company has laid down the plan of increasing its capacity to 340,000 tons (increase by 100,000 tons) in the next three years. The expansion will take place in equal phases of 33,000 each year.

Bulk to Specialty – Specialty currently accounts for 65% of the revenues and is expected to be increased to 75% with the help of increase capacity and R&D from its Centre in Ankleshwar. The management is also quite focused on improving and sustaining their EBITDA margins in mid two digits (14 to 15%). The company has been receiving a lot of demand for these specialty products that caters specifically to a particular industry.

Maiden Con Call – The company has just conducted its maiden con call with the joint MD Mr. Hussein V. Rayani and CFO Mr. Pramod Maheshwari. Prior to this call, Hussein Rayani has done a couple of interviews on CNBC and ETNow in the past year, with the highlights being:

ETNow (Feb, 2021) –

High demand from pharma, ink and rubber. Sustainable demand (73,000 tons in Q3).

High crude prices do affect the business as it is a key raw material along with base oil (a derivative of crude oil). The company is mitigating this by holding monthly contract discussions with their suppliers and clients with regards to the pricing. Positive and negatives are passed on to clients. Abrupt price changes might affect the margins, but base oil has a time lag of 4 to 6 weeks as compared to direct crude daily changes.

Focus shift towards Specialty Oils by changing the product mix for better margins. Specialty now accounts for 65%, few years back it was 50%, forecasted towards 75%. Demand from ink and rubber industry for cleaner and value-added products. Back log in the R&D Centre with approved list of products from their customers. Acting as Import substitute with JIT.

CNBC (Jul, 2021) –

Ratings upgraded by CARE and ICRA from A- to A stable for long-term and from A2+ to A1 for short-term. No plan to raise debt. All capex in Indian units (100cr.) would be done from internal accruals. Capacity utilization more than 100%.

UAE Subsidiary, Panol Industries, 40,000 tons capacity running on 100% capacity and expansion of another 20,000 that is on-going and will commercialize in FY2022.

FY2022 guidance a 15% to 20% revenue growth. Margin guidance for FY2022 would be 10-12% due to the rise in crude prices. Efforts in changing product mix towards specialty oils, as mentioned in February ETNow.

Promoters are optimistic on the business prospects and have been buying from the open market. Hussein openly accepts that we will be buying every year at about 1%.

Auditor could not visit the corporate office in 2020. They are hopeful with normalcy; physical inspection would be possible. Dividend pay-outs will increase going ahead.

Anti-Thesis:

Industry and Peer Valuations

Crude Oil Prices

Game of Capacity and No Moats

Please continue this thread with your research, and in the meantime I will be posting key highlights from the maiden concall as well.

Disc.: researching, not invested.