| FY 25 | FY 25 | ||

|---|---|---|---|

| Q2 | Q3 P | ||

| Income | |||

| Revenue from Ops | 2,001 | 2,420 | >Assumed 1800 Cr retail and 620 cr refinery sale >Assumed Q3 FY 24 retail ; refinery sales mix was 65:35 and assumed 45% retail growth in this quarter in line with business update >with 45% retail growth , Retail sale would be ~ 1800 Cr and refinery would be 620 cr |

| Other | 12 | 2 | |

| Total Revenue | 2,013 | 2,422 | |

| Expenses | |||

| Cost of Material Consumed | 1866 | 2187 | After factoring in 9.7% Gross Margin |

| Employee Cost | 27 | 33 | In proportion to increase in store from 39 to 48 |

| Finance Cost | 13 | 11 | in proportion to increase in revenue and factoring in 30% reduction due to increase in GML from 20% to 55% |

| Dep and Amort | 7 | 9 | Increased in line with revenue increase |

| Other Cost | 54 | 65 | Increased in line with revenue increase |

| Total Expenses | 1967 | 2305 | |

| Tax | 10.9 | 30.09254511 | |

| 24% | |||

| Gross Profit | 147 | 235 | |

| EBITDA | 66 | 136 | |

| PBT | 46 | 117 | |

| PAT | 35 | 86 | |

| Gross Margin | 7.3% | 9.7% | |

| EBITDA Margin | 3.3% | 5.6% | |

| PAT Margin | 1.7% | 3.6% | |

| Retail: Non Retail Sales Mix | |||

| Retail | 60% | 74% | |

| Non Retail | 40% | 26% | |

| Retail: Non Retail Gross Margin | |||

| Retail | 12% | 12% | |

| Non Retail | 3% | 3% |

2 Likes

Here is my projection for Q3

@murali603 : For your comments Pl

1 Like

@bibhor You may right or wrong. But i appreciate your efforts. Great work sir. Thank you. This post is definitely enlightening.

2 Likes

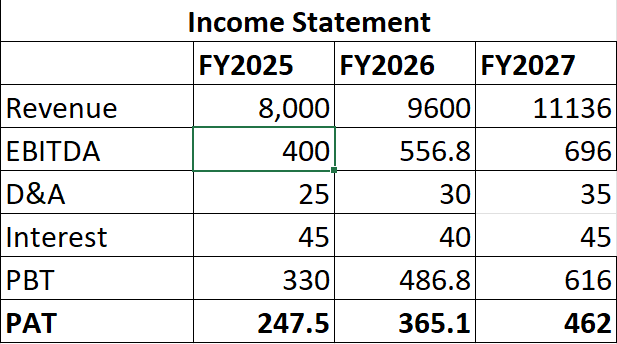

I made below annual projections for my YouTube video purpose, I may be a bit more bullish here, but it could be a ball park idea.

1 Like

Hi Amit , Can u be little more detailed on assumptions on gross margin , ebitda margin and drivers for these , retail vs refinery ratio and new store count assumed

Only numbers does not help to understand the thought

3 Likes

This is a conservative estimate, Management told they will be at par with peers margin profile in 2-3 quarters, so we may see gradual improvement in margins QoQ slowly

Hey, Bibhor I have taken the EBITDA margins at 5% in FY’25, which can improve due to higher retail sales as well gold sourcing from IBX along with the higher stud ratio. In my views company is on track to make ~8000 crores of revenue by the end of FYE’25 as of now they have done ~6,000 crores in FY’25. Finance cost in next year could be lower due to use of GML and depreciation could increase because of higher number of stores. I have explained these details in the video link in profile.

4 Likes

Hey, Amit thanks for sharing the video, I disagree with the sales numbers that 8000 crores can be reached. In my views company could miss this number by 5% to 7% , however margins could be in the same range.

3 Likes

Kudos bibhor!

You were correct to the point on PAT. It helped me build conviction and make a stronger position.

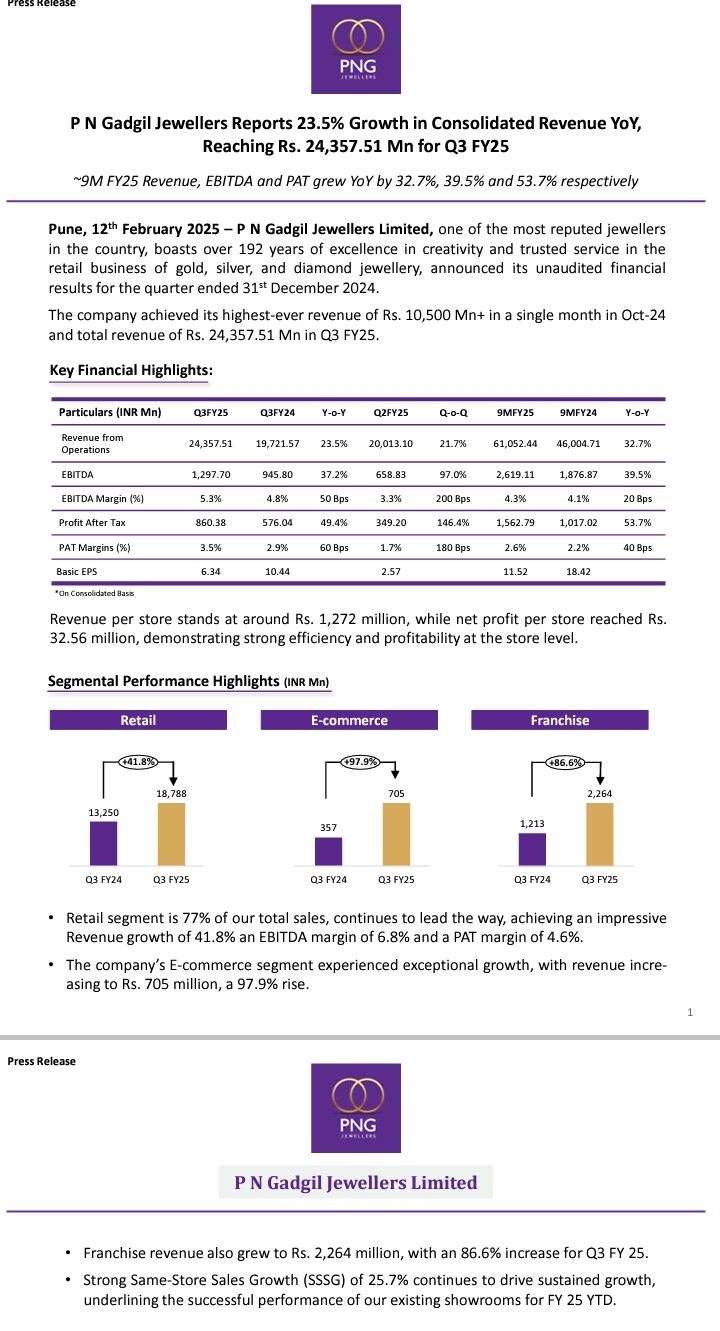

Results q3 fy25 good set of numbers

Operational Financial Highlights

•The transaction count grew by 20.9%, alongside a 21.7% increase in Average Transaction Value (ATV), reaching Rs. 86K.

•A 36.2% increase in foot falls, coupled with a strong Conversion rate of 93.7%, further fuels our growth, reflecting increased Demand, customer engagement and sustained purchasing behavior at the store level.

•festive season continues to contribute Navratri sales growing by 18.0% and Diwali sales seeing a substantial increase of over 52.7%.

•A 38.7% YoY rise in stud ratio, which now stands at 7.4%.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c2c4d63e-ea7d-41d6-ba32-93c3112219b6.pdf

2 Likes

Thanks Abhay ![]() By the way numbers are tying for Gross Margin and almost for EBITDA margin also ; Now lets see what the management guides for Q4 and next year FY 26

By the way numbers are tying for Gross Margin and almost for EBITDA margin also ; Now lets see what the management guides for Q4 and next year FY 26

2 Likes

I had one question and would be really helpful if someone could highlight what I am missing on here. Rev grew by 24%, however all the segmental revenue be it retail, ecomm or franchise grew by more than 40%. Is there any segment they are not reporting in press release? Also since Retail forms 77% of sales and grew by 42%, what is bringing the overall revenue growth to 24%… Just curious to understand more about the business model

All three are retail segment… They have one more segment non-retail, that degrow

PN Gadgil Jewellers Limited Q3 FY25 Concall Summary

Financial Performance

Record Month: October 2024 was best-ever month, with revenues exceeding 1,050 crore.

Retail Business: Contributed 77% to total revenue with an EBITDA margin of 6.42% and PAT margin of 4.23%.

E-commerce Revenue: Doubled to 70 crore (+100% YoY).

Franchise Revenue: 226 crore (+87% YoY).

Same Store Sales Growth (SSG): +26% YoY.

Revenue per Store: 3.25 crore, indicating strong efficiency.

Transaction Trends:

+21% increase in transaction volume.

+22% rise in Average Transaction Value (ATV) to 86,000 per transaction.

+36% increase in footfalls, with a 93% conversion ratio.

Festive Boost:

Navratri sales up 18%.

Diwali sales surged 53%.

New Stores Performance:

New stores reaching operational self-sufficiency, expected to break even in under a year.

New stores contributed 240 crore to Q3 revenue.

Marketing & Cost Increases:

30 crore increase in expenses due to higher marketing spend, hedging costs, and festive discounts.

FY25 marketing spend projected at 55-60 crore.

Inventory & Hedging:

Inventory worth 1,800 crore with 58 kg Gold Metal Loan (GML) as of December.

Q3 inventory gain: 2.5 crore.

Hedging ratio at 83% as of December, ensuring protection against gold price fluctuations.

Gold metal loan usage increased from 12% to 45%.

Fully hedged as of January 2025.

Hedging is based on sales forecasts and is a continuous process.

Mark-to-market hedging expenses included in expenses.

Expansion Plans

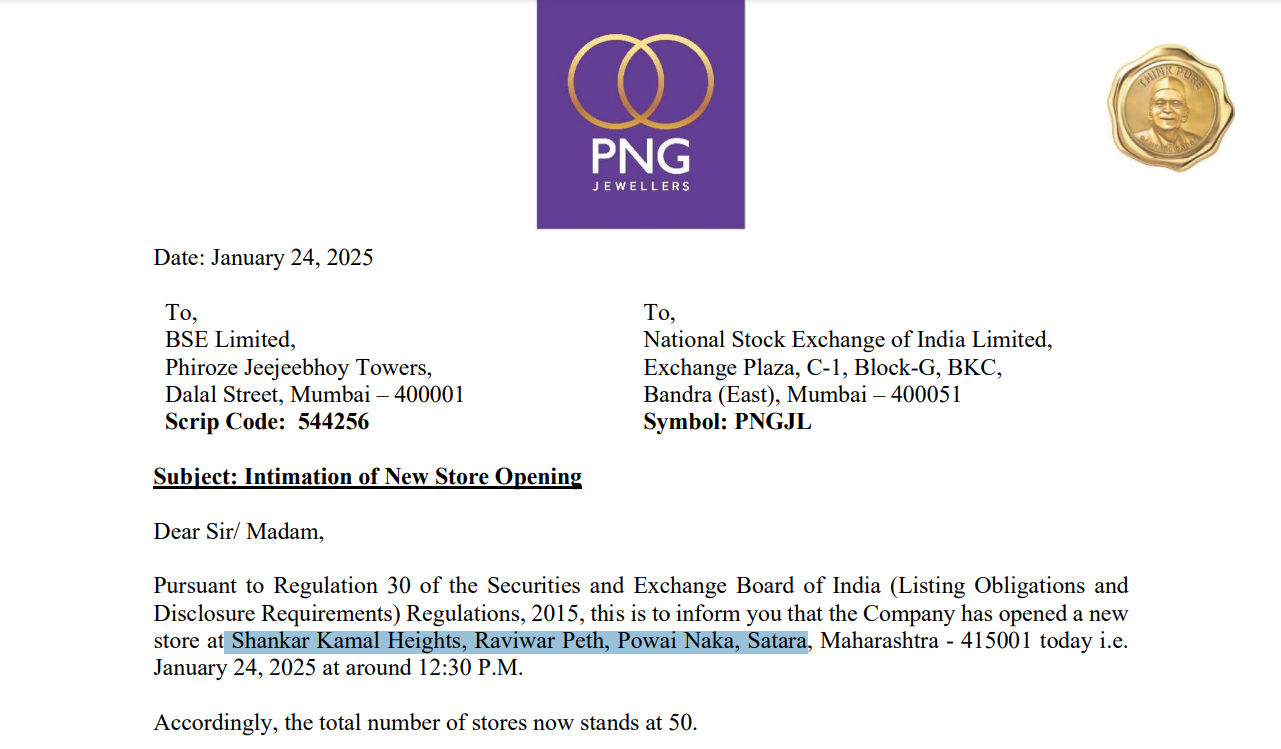

Aggressive Growth: Opened 9 stores in 9 days during Navratri, reaching 48 stores.

Current Total Stores: 50 stores, targeting 53 by March 2025.

FY26 Store Expansion Target:

25 new stores, a mix of Company-Owned (COCO), Franchise, and Lifestyle stores.

8 COCO stores, 8 franchise stores, and 10 lifestyle stores.

Lifestyle stores to target younger consumers, with lighter-weight jewellery and 15-20% EBITDA margins.

Geographical Expansion:

Entering Madhya Pradesh, Chhattisgarh, Jharkhand, Bihar, and Uttar Pradesh.

Initial focus on company-owned stores in new states.

Exploring Karnataka for future expansion.

International Expansion: First U.S. store in Seattle set to open in Q1 FY26.

Expansion Funding: Growth will be funded through internal accruals, ensuring no negative margin impact.

Product & Consumer Trends

Studded jewellery ratio increased 39% YoY to 7.4%, targeting 12-13% in 2-3 years.

Rising demand for Polki & Jadau jewellery (Polvi brand).

Changing Consumer Preferences:

Lightweight rose gold & white gold jewellery gaining traction.

18-karat gold jewellery (chains & finger rings) introduced as a pilot project.

No plans for lab-grown diamonds under PNG brand, but may consider for lifestyle stores.

Future Financial Outlook

Q4 Expectations:

Wedding season & Gudi Padwa sales expected to drive growth.

Seasonality impact expected but company remains confident.

EBITDA Margin Stability:

Expansion costs will not impact margins, supported by strong internal accruals.

New stores expected to break even in 9-12 months.

Future Expansion Model:

Expansion to leverage brand loyalty & community connections in new regions.

Exhibitions & customer engagement activities to build awareness.

E-commerce model to complement offline expansion, with ready-to-ship & made-to-order options.

Others

Margins in online sales are at par with offline stores.

Custom Duty Impact: The 3 crore impact of previous reductions has been fully absorbed.

Debt-Free Status: IPO proceeds used to repay debt, maintaining a strong balance sheet.

Gold Price Impact: Despite gold prices rising to 80,000 per 10g (vs 72,000 YoY), demand still increased by 5%.

Bullion Business: Gradual reduction in non-retail bullion business focus.

Disc:- invested added more recently.

3 Likes

As margins are improved significantly in this Quarter, Growth trajectory may not continue in Q4 as Q3 is strong due to festival demand.

Expecting some rerating on basis of margin improvement.

2 Likes

Management already said in concall that (Take with a Pinch of Salt)

Wedding season & Gudi Padwa sales expected to drive growth.

Maharashtra has a strong gold-buying culture during weddings.

The December-May period sees peak wedding purchases, including bridal jewellery, gifts, and family purchases.

Gudi Padwa has cultural significance is considered an auspicious time to buy gold. Many people purchase jewellery, coins, and other gold items as a tradition.

It also marks the start of the Hindu financial year, influencing investments in gold.

And its better to analyze seasonal business on a year-on-year (YoY) basis rather than quarter-on-quarter (QoQ) to get a clearer picture of trends.

2 Likes

@ Varsh : Con call summary well summarised , thanks

-

What’s the outlook for sales and PAT in Q4 : Can we assume ~ 2k cr of sales and 70 cr of PAT ?

-

What’s the sales growth outlook for FY 26 ? With no of stores moving from 53 to 78 and SSG of 25% , can we assume 40-50% sales growth in FY 26 ? and whats the margin outlook for FY 26 , will the aggressive expansion next year eat away margins and profit growth would be lower vs sales growth ?

1 Like

One more questions , There has been some news of increase in Interest rate on GML ? Does anyone has any views here ?