Sharing some notes found valuable

Source:-x.com

2 Likes

e0363399-d98d-4a4a-92ad-4eb0afeb88a3.pdf (1.3 MB)

Q3 Update - mgmt has not included the same store sales growth rate for this Q. The retail revenue growth is at 42% which is at par with big boys like Kalyan and 40% growth in diamond business given that they only do natural diamonds and not LGDs.

Also if anyone could point out what do they mean by “24% YoY consolidated growth” growth as in what? revenue, volume, ssgr?

1 Like

The “24% YoY consolidated growth” mentioned in the PNG Jewellers quarterly update refers to a year-over-year increase of 24% in their consolidated revenue (total revenue across all operations ) compared to the same period in the previous financial year (Q3 FY24).

Reported numbers and segment revenue growth is a mismatch.(may be i m missing something)

• PNG Jewellers highlights individual segment growths such as:

• Retail: 42% YoY

• Franchise: 87% YoY

• E-commerce: 98% YoY

• Diamond category: 40% YoY

• Yet, the overall consolidated growth is reported as only 24%.

This mismatch could indicate underperformance in other revenue streams

Actually posted lower than expected numbers.

Kalyan jewellers reported 39% on consolidated basis and Titan jewellery unit reported 26% growth and domestic jewellery unit posted 25 %.

3 Likes

In the last Q concall mgmt said that they have two different business i.e retail and non-retail.

Retail is their physical in-store sale and non-retail is their ecommerce and refinery sale, mgmt guided last concall that they will be focusing more on the retail side of business which is high margin. This time the retail business growth is fine.

So it looks like the non-retail business have taken a hit this time, this also mean that earlier the non-retail business growth would have been more than the retail.

It could be the bullion sales drop which earlier contributed to much of their growth in non-retail segment this, time it’s not the case hence we see only 24% you growth. Titan grew at 26%, kalyan at 41%, png at 24%, senco left. All in all a serious rerating could be underway.

Markets have been quite selective lately 24% yoy rev growth is a huge let down, even Titan being the mammoth it is grew sales at 26%

6 Likes

with 24% revenue growth YOY, the 9 months total revenue would be ~5300 crores and there seems to be higher chances that company would miss the 8000 crores revenue guidance. Stock may get a beating tomorrow…

4 Likes

Agree. 24% yoy growth is below expectations.

they must have reported or provided some details about the performance of their non-retail segment (e-commerce, bullion and refinery sales), as it is a key part of their business.

PNG Jewellers’ top-line (revenue growth) may slow due to a shift away from the lower-margin non-retail segment (e.g., refinery sales). However, their bottom-line (profitability) is expected to be least impacted because of higher-margin retail sales, leading to margin expansion. This may be a strategic focus on profitability over aggressive revenue growth.

1 Like

As per my estimate , their bullion revenue would be 30-35 pc of overall revenue last year and operating margin of retail business would be 6/7 pc and bullion would be 2/3 pc and 4-5 pc blended margin

With this hypotheses , out of 1940 cr of top line in Q3 FY24 , retail would be 1240cr and bullion 700 cr , blended operating margin was 4.6 pc ( assumed 6 pc for retail and 2 pc for bullion )

For Q3 FY 25 , My estimation is overall at 24 pc growth , they would have done 2420 cr of top line , with non bullion growth at 50 pc and bullion de growth of 10 pc ( 1800 cr non bullion and 620 cr of bullion ) with blended operating margin of 6 pc ( 7 pc for non retail and 2 pc if bullion ) ; with this number their operating profit might be 144 cr and Pat of 86 cr , growth of around 55-60 pc in both operating profit and PAT .

Pl provide your views

Disclaimer : Invested

4 Likes

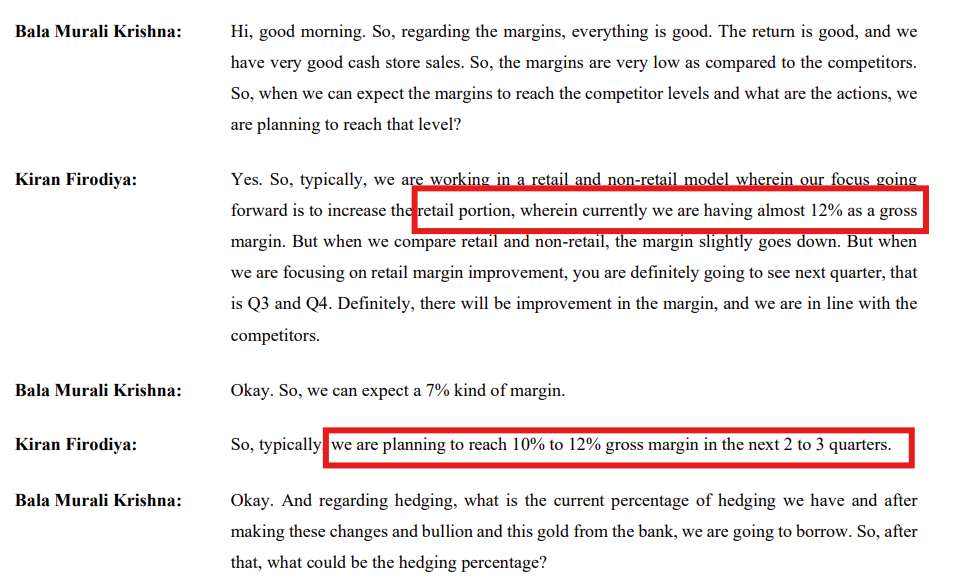

Few snaps of my question in Q2 call regarding margins.

In Q2 they have GM% ~7 and they want to take this to 12-13% in 2-3 Quarters.

12-13% GM is at par with the peers.

If they can push GM from current 7% to 10% then it will boost the EBITDA by 50-60 Cr

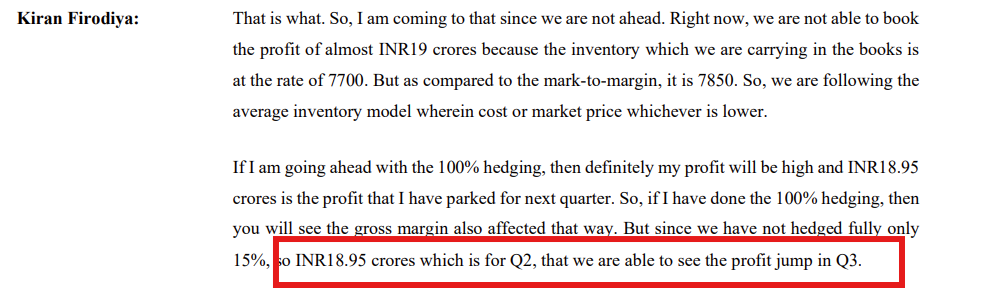

Below answers my hedging related question, frankly speaking i have not understood what they said but repeatedly he said ~19 Cr will add up in Q3.

8 Likes

Thanks Murali , This is very helpful , So what is the operating margin and Net profit you expect in Q3 ?

We can expect 4-5% operating margins in this quarter if they have executed the things as per the plan.

As Q2 has some other income in the form of income tax return, that will not be there in this quarter. In a very conservative estimate i am expecting at least 45 Cr of bottom line, which excludes the 19 Cr amount discussed in the call.

2 Likes

How do forum thinks about PN Gadgil’s growth for next few years and comparison with peers?

I felt 24% revenue growth is not very aspirational and inline with senco with higher P/E

1 Like

Retail business grew by 40% + in Q3 , if they grow by average 30 pc plus for next 3 years with retail mix of 90 pc their margin would improve appreciably, which will help Pat growth of 50 pc

Will get more clarity in the con call of Q3

Stock is currently valued at 38 times forward PE

1 Like

@murali603 : I think 19 cr is the inventory loss hit they took in Q2 which probably will not come in Q3

Moreover 4-5 pc operating margin is only 1-2 pc increase from last quarter , is this very conservative or realistic ?

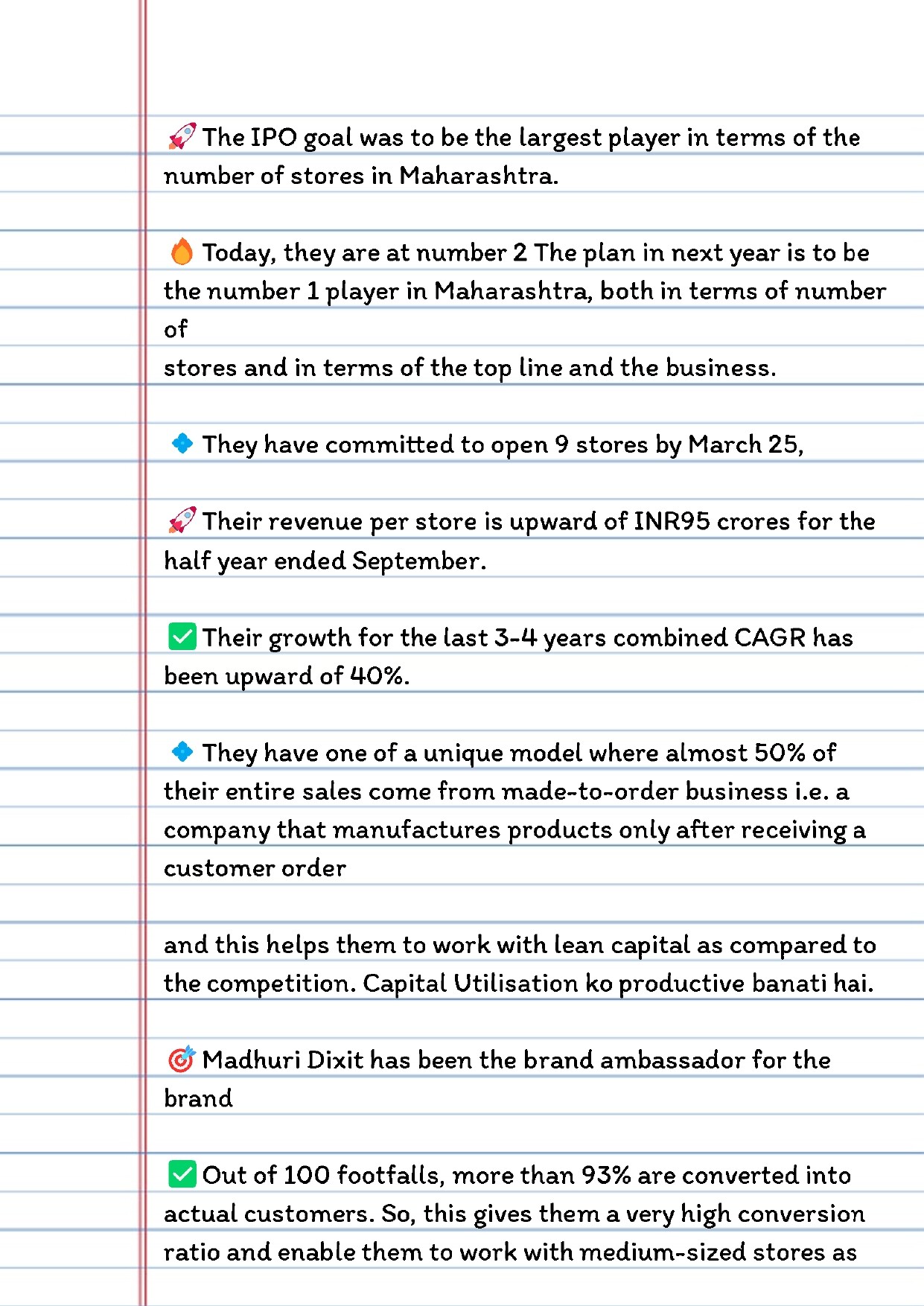

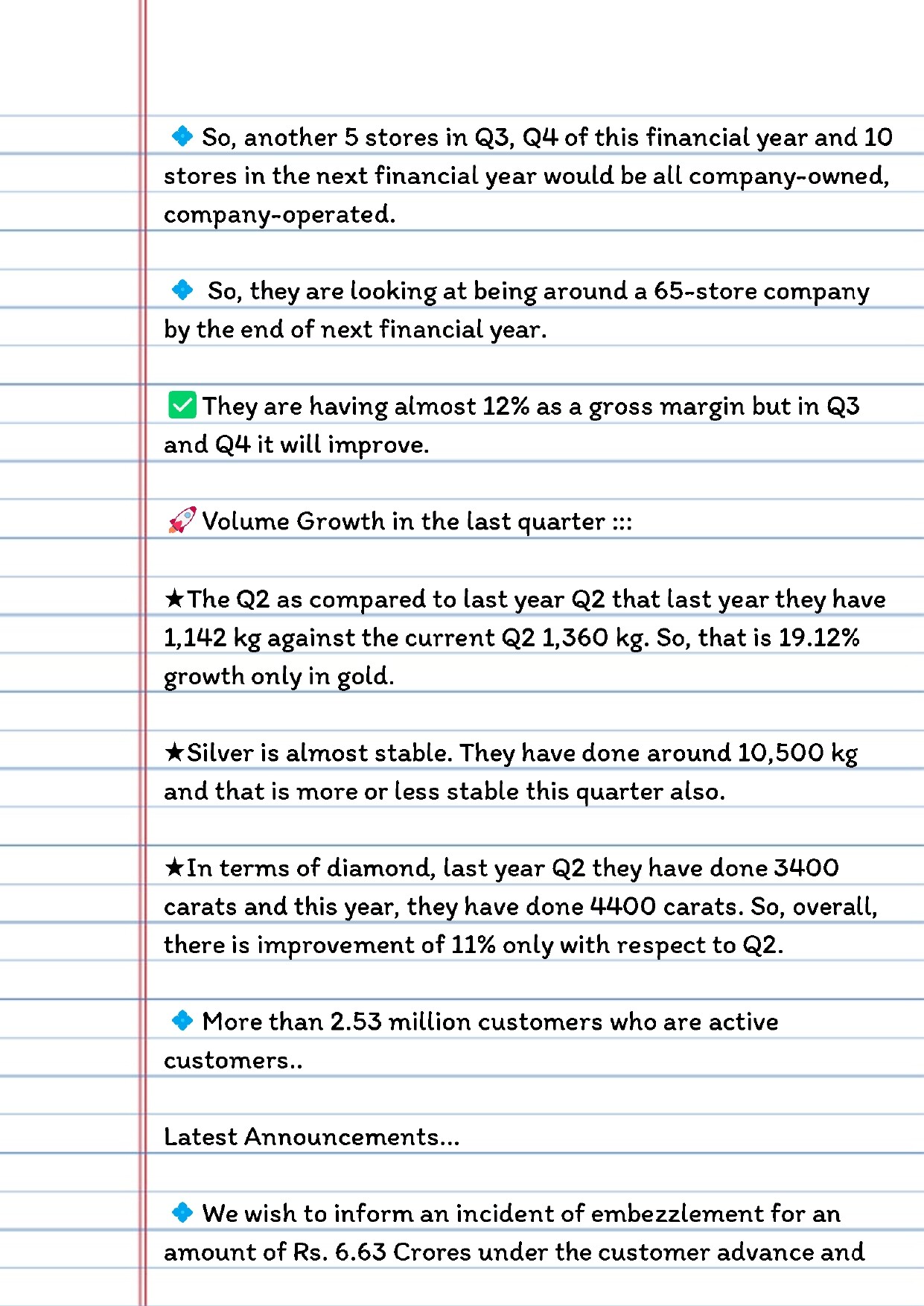

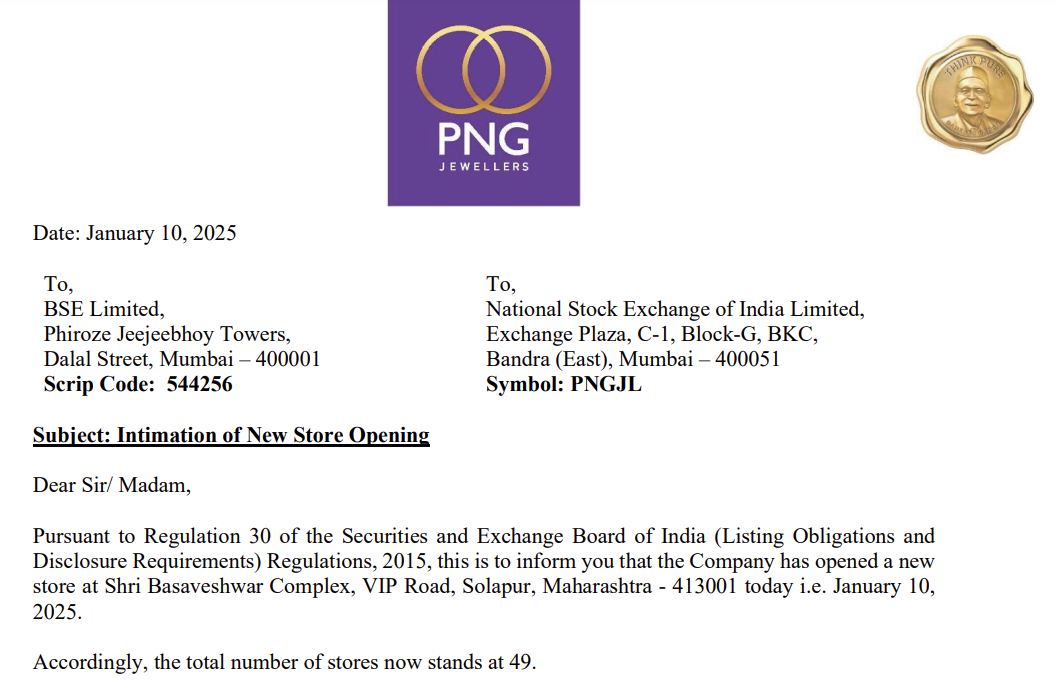

PN Gadgil | Press Release

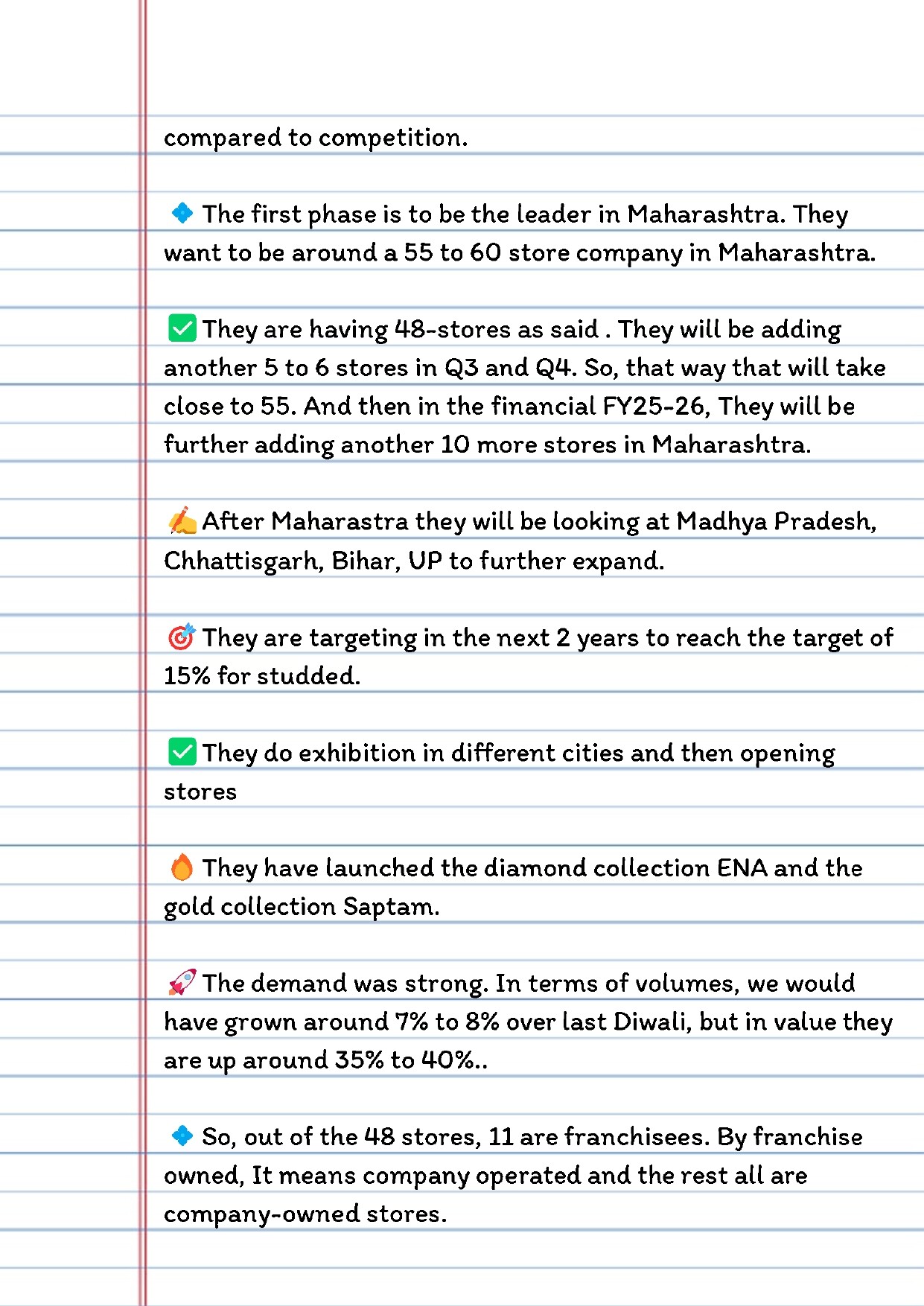

a. New store opening at Solapur

b. Store count stands at 49

c. Revenue per store is upwards of 95 cr/store

d. Company have committed to open 9 stores by March '25

e. Strong Footfall to Conversion Ratio: Out of 100 footfalls, more than 93% are converted into actual customers

Source: Concall + Press Release Note

1 Like

Future would depend on the OPM?

If margins are below 5% for the next 3 quarters, then it would be not easy ride…

Q3 con call and q4 decide the faith of this company.

1 Like

@Arka , where have they committted to open 9 more stores by mar 25 ? as per my understanding they are likely to open only 2 more stores by mar 25 ; this is in line with 12 stores committed in RHP , 9 open in Navratri , 1 now and 2 in future

2 Likes