Dear Experts of the Group,

I am a relatively new entrant to the stock market. I would like to know the views of long term wealth builders here, on the currently overvalued stocks like Nestle, Page, MRF etc. I was planning to buy MRF three years back and I felt it is overvalued and see now where it is? What is the best approach in scripts like there? I have an investment horizon of 5-10 years.

1 Like

My understanding is that higher the ROE, higher valuation a stock will command. The value will hold at such levels until the company is able to grow at a good pace and maintain high ROE. But once the growth falters, then such high valuations will not sustain.

So if you find a stock with high ROE and if you are sure that it can sustain growing at a good rate for the next many years, then you can purchase such stocks. The challenge here is to assess how long the growth rate can be sustained which is no easy task (also called measuring a stock’s moat). It will take a number of years and painful lot of effort to learn to do this. If you just go by the current hot names, it is nothing more than spraying and praying and I do not think it will work out well (even if a stock is HDFC, HUL or Gruh Finance).

So investment in highly priced stocks should be based on your ability to measure such stocks moat.

10 Likes

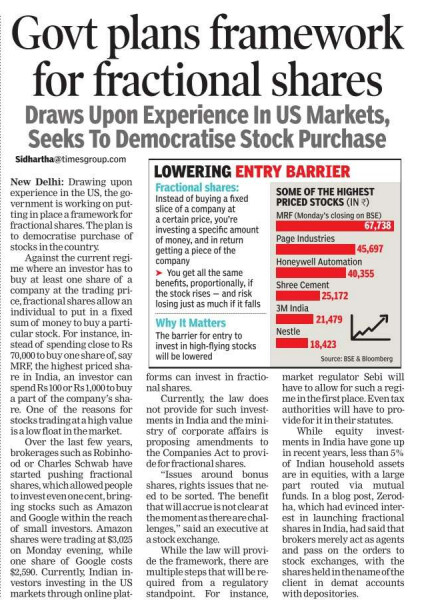

This was a good post -

My take is that if I feel the business has longevity ( true for FMCG ) then ok to regularly SIP into these stocks. These are the kind of stocks to be handed over to your children and so on…

I have read somewhere : Market can remain irrational longer than one can remain solvent.

So it all depends the period you are looking at.

Additionally, the biggest wealth is created in small and microcap stocks provided one can find quality & growth. Size itself becomes an issue for large companies and reversion to mean is bound to happen. The question is not why but when

Both are controversial statements and my take is to find the upcoming quality growth stories instead of waiting on when the multibaggers will fall or why they are not falling

5 Likes

Market seems to be paying for brands, longevity, predictability… For ex. Book value of 100/-, profits 60/- (~50% RoE), market cap 3000/-, dividend 50/- (means reinvestment in business is 60-50=10), 50 PE. Tbh It does not make sense to me.

2 Likes

4 years on and the valuations are even higher. I wonder if we will see the moated stocks going to pre pandemic PE levels.

1 Like

But only nestle has outperformed nifty. Other 2 haven’t. It makes sense to avoid egregiously valued stocks

3 Likes

Yes it does. Even the best moated stocks finally move towards fair value. BTW am a regular follower of yours on Youtube, Ishmohit. You are doing some great work there!