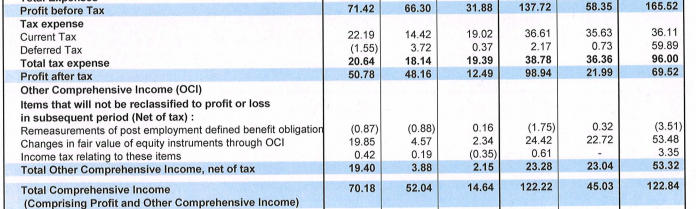

Total comprehensive income differ to the extend of 38% than Profit after tax. An entry Changes in fair value of equity instruments through OCI adds 19.4 crores to profit after tax of 50.7 crores which is quite substantial.

My question is What is Changes in fair value of equity instruments through OCI?

Other Comprehensive Income is income that is not routed through P & L, but you may want to route it directly through Balance Sheet as a matter of policy (as it does not belong to core business operation). In the present case, it seems some equity instruments held by the company are valued or sold at a price higher than their book value. That difference is being shown here.

Typically, OCI includes items like gains on derivative instruments, revaluation of pension plans, foreign currency translation gains and the like. Other Income generally includes items like interest on bank deposits, sale of fixed assets etc. There is no hard and fast rule as to what should appear where but as a matter of accounting policy, assets are classified beforehand as whether to be routed through P&L (called Fair Value Through P & L) or through OCI (called FVTOCI). You will find the details of this in the Annual Report.

Let me try to answer this but I am not an accountant so take it for what its worth.

Accounting standards are based on few principles

Income statement should give true and fair picture of results of operation of the company.

Balance sheet should give a true and fair picture of financial condition of the company.

Clean surplus accounting should hold true for each period. i.e. change in shareholders equity should be equal to retained earnings( net profits minus dividends and/or buybacks, assuming no new equity funding).

Companies have several items that go into preparation of statements like pension obligations, derivative instruments, forex holdings etc whose fair market value can change substantially from year to year. Carrying these at historical cost will violate principal 2. Carrying these items at market value on balance sheet without a corresponding entry in P&L will violate principle 3, and finally, routing it through P&L may violate principle 1 if these items are large and are not directly related to primary business of the company.

In order to meet all 3 principles at the same time, a new section is added to P&L called OCI where all such MTM adjustments are reported below the profit after tax (bottomline). this will ensure that P&L (upto PAT line) gives true and fair picture of results of operation, balance sheet will be marked to market so it gives a true and fair picture of financial condition of the company and clean surplus accounting holds (by using the total comprehensive income line instead of profit after tax line).

Total Comprehensive Income is like a second bottom line (in addition to the traditional bottom line PAT). Typically, there should not be a large difference between TCI and PAT but a large difference by itself is not an issue if there is a sufficient justification for it. A large difference mean than secondary operations or external factors are having a major impact on the company’s financial condition and that should be investigated.

Previously, there was no uniform treatment of OCI (FVTOCI or FVTPL) and companies would merge OCI with PAT either to smooth earnings volatility or show higher or lower earnings, or some other objective. I have written previously about CDSL here.