Yes they have given reason for all actions,but still stock price have fallen moren than 20% from listing.I know that there were also other headwinds.Any way i booked 30% loss and exited this company.As a stock market participant it is very important to learn chart reading and technicals.If i would have waited for 1 year before entering this story i would have saved my money.Fundamentals and Technicals both matters. TechnoFunda is the thing we should do.

4 Likes

10× Jump in Receivables: Serious Risk to Earnings Quality? | What’s the Outlook Now?

4 Likes

The market expected PM-KUSUM 2 to be announced in the Budget with a headline allocation of ~₹50,000 crore, and the absence of such an announcement was interpreted negatively. However, this appears to be a misreading of the situation.

In FY25–26, the allocation for PM-KUSUM was only ₹2,600 crore, whereas in the current budget it has been increased to ₹5,000 crore — nearly a doubling of annual support. This clearly indicates that the government continues to see merit and execution potential in the scheme.

The lack of a headline announcement does not negate the possibility of PM-KUSUM 2. The original PM-KUSUM itself had a total outlay of ~₹34,000 crore spread over multiple years, while annual allocations remained modest in the early phases. A similar approach is possible now: PM-KUSUM 2 could still be launched with a multi-year outlay of ~₹50,000 crore, starting with ₹5,000 crore in the current year and scaling up gradually over time.

In this context, the market reaction seems driven more by expectation mismatch and missing headlines rather than a deterioration in policy intent or industry fundamentals.

I would like to know opinion of others on this.

5 Likes

The official announcement from the government notes that the new KUSUM scheme will be announced after the current phase ends in March 2026. To quote

On PM-KUSUM, he [Pralhad Joshi] noted that after initial reluctance, the scheme has now gained strong momentum across states, with demand for additional allocations from Chief Ministers. He announced that the second phase of PM-KUSUM will be launched after the present phase ends in March 2026.

There were also stakeholder consultations on the design and implementation of PM-KUSUM 2.0. These deliberations aimed at aligning state action, industry inputs, and policy reforms to accelerate renewable energy deployment across the country

[Emphasis mine].

The various stakeholders have been in meetings with the ministry for a long time now, and many more states are now eager to participate, as noted by Mr. Pralhad Joshi in this interview. 15 minutes worth watching. Summary: “Had to get more buy-in from states, and they now want the scheme to be bigger. MH’s successful model to be used as an example. Simplification. Better financing for farmers. Current scheme to be sunset by 2025/03/30”

Individual states have been announcing their own schemes, and aren’t waiting for KUSUM 2.0. For example, see this article citing the Madhya Pradesh CM. Some quotes

Crop turns into gold if water reaches a dry field. We will ensure that every farm in the state gets water

The farmers will now receive a 90 per cent subsidy for the installation of solar power pumps, up from the earlier 40 per cent

Yadav said farmers are being provided 32 lakh solar pumps on subsidy, enabling them to generate surplus electricity and sell it to the government. The state has expanded its irrigated area to 52 lakh hectares and set a target of 100 lakh hectares

[Emphasis mine]. Similar schemes have been announced by Maharashtra. And if you’re keeping tabs, Oswal and other recently got their first ever orders from Karnataka.

The Pralhad Joshi interview also mentions that the request for the approval has now been sent to the PM office. My guess is that it may go up to June before any new announcements are made. But it may take longer (and meanwhile, the work won’t stop as states are being proactive).

4 Likes

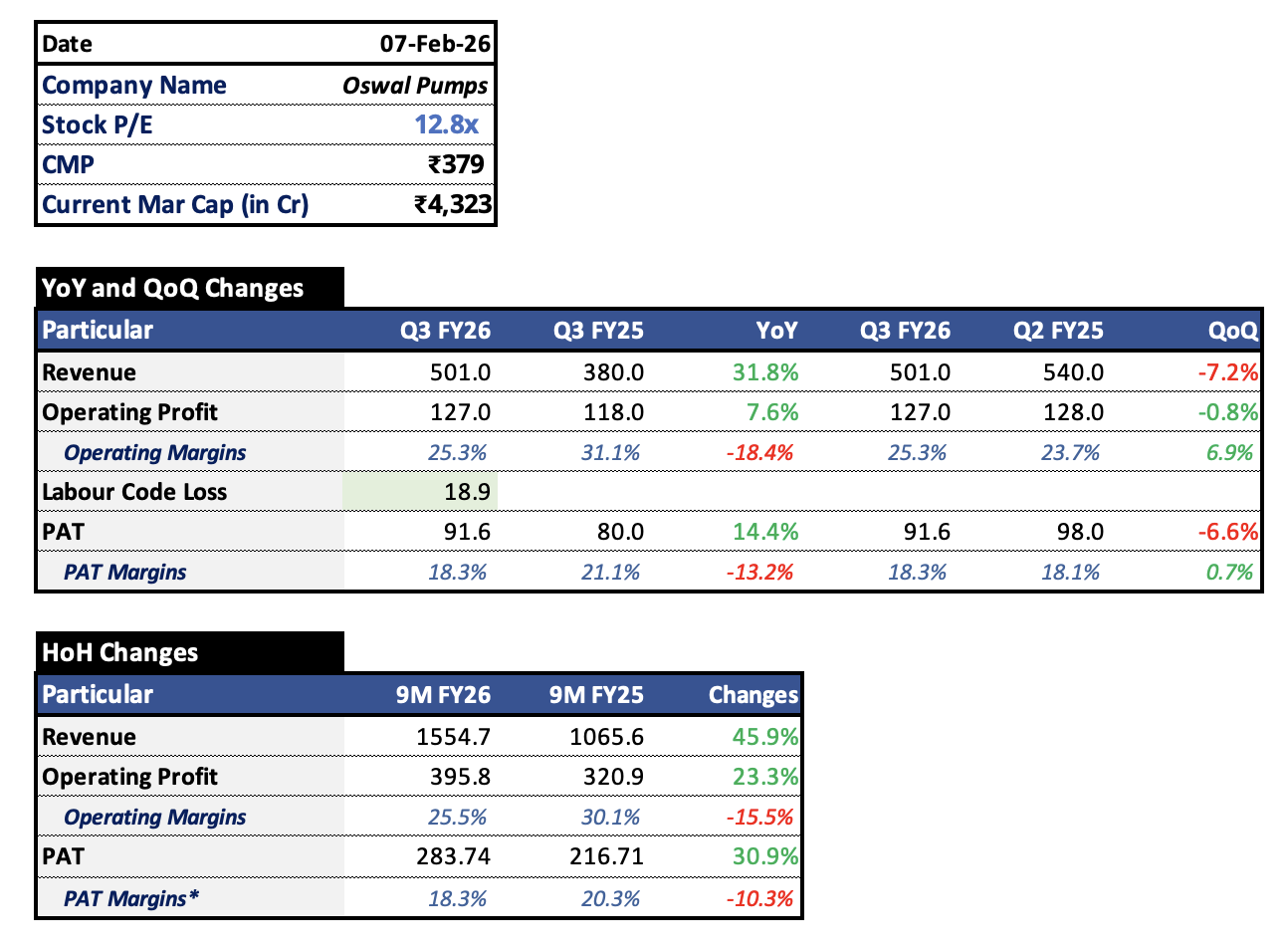

Q3 FY26 Results

Good Results by Oswal Pumps in Q3, margins recovered strongly despite lower topline, hoping strong Q4 with good recent orders inflow.

3 Likes

Rajasthan budget for 2026-27 announces 50000 solar pumps at the cost of 1500 crore: https://finance.rajasthan.gov.in/docs/budget/statebudget/2026-2027/pressnoteng2026-27.pdf

Note that the state government costs are usually 30% of the total cost of the pump installation.

2 Likes

I was going through the Investor presentation dated Feb 7 2026 on https://www.bseindia.com/xml-data/corpfiling/AttachHis/b30b1397-2dba-46be-9118-268b599d38f5.pdf

On page 35 under IPO Fund Utilisation there’s a line called “General Corporate Purposes” and it contains a significant amount 1678.96 of total IPO proceed of 8415.14. Does this high amount warrant any investigation or is it considered normal? It is at 19.95% of total proceeds without any further information.

1 Like

The maximum allowable limit is 25% as per SEBI rules. It is within the allowed range. Also, as per the law, the company is not obliged to disclose the amount used via line by line expenses. So they are compliant as per reporting rules.

2 Likes

As of today’s (19th Mar 2026) numbers.

The PE has fallen to 9.94, which is the lowest. Profits are growing, but it is not reflected in the share price.

1 Like

This stock has really stumped me. I am clueless why its going down & down with no particular reason - these type of incidents sometimes makes you wonder if the market is fair or completely rigged.

I am Tracking this and i will say There are enough reasons to justify why it is going down.

-

first reason is overall market downfall specially smallcap index

-

raw material prices of solar cell going up because of recent silver rally and a weaker INR against dollar [ purchasing contracts with Vendors are in USD currency]

-

Renewable energy theme specially Solar energy turned from bullish to bearish mode [see PE ratio of all other companies involved in solar related epc,manufacturing ]

-

No Future Visibility of New Orders because of No proper announcement of new PM KUSUM 2.0 Scheme So market is assuming downside trend in Revenue from Q1 FY27 onwards and we all know MR. Market hates degrowing companies.

-

Significant number of New players has entered this market When PM KUSUM 2.0 will Come Company Has to Face Intense Competition from existing+new players+Regional Players and it will lead to margin dilution.

-

Company is highly dependent on PM kusum and Government Schemes for its revenue. So its a B2G Company and Investor’s generally avoid B2G companies.

7.Total Trade Receivables are More than 50% of total company balance sheet [In my opinion TR days are long because of Industry standards and every penny is Secure and recoverable] but Mr.Market Hates Receivables and loves Actual cash flow.

-

In Latest Concall Management Acknowledged Pricing Pressure in Tenders and its biggest competitor SHAKTI PUMPS Margins has come down by 9% in Q3 [from 20% to 11%] compare to previous Quarters So market is assuming Oswal margins will follow SHAKTI pumps trend [ imo this is a genuine problem and matter concern for Investors]

-

90%+ Revenue is dependent on 2 States [Maharastra+Haryana]

Opinion {1}My Take will be if anyone is holding this its better to hold and Relax because above mentioned points are Already Priced in. {2}. If anyone is thinking of buying this Can buy but with little % of portfolio because of Risk and reward and good margin of Safety.

{3}. If anyone is holding this Stock by Leverage,MTF its will better to exit leverage positions when market will give chance or leveraged buyers can reduce position now if they find good opportunities in other sectors.

disc- invested, DYOR.

10 Likes

Risk Analysis from Q3FY26 Concall

- Working Capital Stress & Rising Receivables

· Net debt rose to ₹188 Cr (0.12x equity, 0.36x EBITDA) due to working capital stretch, with CCC worsening to 177 days (vs 157) and receivable days rising to 157 (vs 138).

· Despite management calling receivables “secure” (govt-backed), the continued QoQ deterioration signals cash flow stress and delayed monetization of reported profits.

- Maharashtra (Magel Tyala) Concentration Risk

· Around 70–75% of receivables are from Maharashtra, with delays linked to AIIB funding approvals + state treasury liquidity issues, making it a single-point working capital risk.

· Even management admitted recovery is not yet improved, relying on expected staggered fund releases till March

- Management’s Risk Control Stance (Positive but Telling)

· Management stated they may sacrifice revenue to protect balance sheet, and are exploring invoice discounting / bank lines to manage liquidity.

· While prudent, this indirectly signals that growth may not be as smooth as guidance suggests if working capital remains stretched.

- Tender Price Compression (Structural Pressure)

· Tender prices have declined 13–14% in recent bids, with management admitting pricing has been “slashed quite a lot.”

- Raw Material Inflation + No Pass-Through Ability

· Input costs (especially metals like copper/stainless steel) are at all-time highs, but cannot be passed on due to fixed-price government tenders (locked for ~1 year).

- Margin Defense Strategy (Execution Risk)

· Company offset ~15–16% combined headwinds (price + cost) using value engineering, supplier renegotiation, and consolidation, limiting impact to ~1–1.25% margin hit.

- Margin Guidance vs Reality Gap

· Management guides Q4 EBITDA margin: 25.5–26% and FY26 PAT margin: 17.5–19%, with claimed impact limited to ~1–1.3%.

1 Like

| Column 1 | Column 2 | Column 3 | Column 4 | E | F | G |

|---|---|---|---|---|---|---|

| Metric / Guidance Item | Original Guidance / Target (Source) | Timeline | Q1FY26 Actual | Q2 FY26 Actual | Q3FY26 Actual | Status & Remarks |

| Revenue Growth (FY26) | 50 to 60% YoY growth in FY26 (Q1FY26 Concall, pg 4), reiterated in Q2, reiterated target of 50% YoY growth in Q3 | FY26 | ₹513.9 Cr; +36.8% YoY | ₹539.6 Cr (+73.9% YoY) | ₹501 Cr revenue (+31.9% YoY) | At Risk (Timing mismatch) — 9M growth strong (~46%), but Q3 growth lower vs guidance run-rate |

| EBITDA Margin | in the range of 27-28%” (Q1FY26 Concall, pg 7). Q2 update: Q3 target 25.5–26%, Q4 target 26.25–26.75%,Q3 Guidance:25.5–26% in Q4 FY26 | FY26 | 27.40% | operating EBITDA 23.7% (–888 bps YoY) | 25.40% | On Track — despite tender pressure, margin stabilized QoQ |

| Net Profit Margin | around 18-20%” (Q1FY26 Concall, pg 7). Q2 revised to 17.5–19%, Q3 comment: 17.5–19% FY26 PAT margin | FY26 | 19.10% | 17.8% YoY | 18.00% | On Track — within guided band |

| Receivables & Recievable as a % of Revenue from operation | 353.57 Cr for H1FY26, 353.5/(539.64+513.95)= 33.55% | |||||

| Receivable Days & Cash Conversion Cycle | “Target to reduce receivable days to 90 to 100 days” (Q1FY26 Concall, pg 5) | FY26 | 126 days | Receivable days 138 as of Sep’25 vs 126 in Jun’25 . CCC worsened from 136 → 157 days. | CCC is 157 days (vs 138) | Miss (Worsening) — clear deterioration due to Maharashtra delays |

| Capacity expansion – pumps | Increase pump capacity from 2 lakh to >5 lakh within a year” (Call p.15)[1]. Q2 PPT: intent to invest ₹898.6 Cr in plant & machinery/civil work for automation & expansion, target 5 lakh pumps by H1 FY27, Q3 Commentry: Capex ordering by Q4 FY26, completion by Q2 FY27 | By Q1 FY27/BY H1FY27/ByQ2FY27 | 2 lakh installed; expansion orders placed[1] | utilization already high (SS pumps 93.9%, CI pumps 83.5%). | Ongoing | On Track — execution phase ongoing |

| Order Book | 29961 pumps, 700 to 800 cr, Q3 Concall: 24,500+ pumps + 25,000 pipeline (expected, not order intake) | By Q3FY26 | 29961 | Q2 order book 18,800 pumps (~₹500 Cr equivalent using same ASP math), pipeline >30,000 pumps. | No major order intake | Stable but Not Expanding Aggressively — no major jump QoQ |

| New product launch — helical/industrial pumps | “First helical-pump samples by end-Q3 FY26; other industrial pumps to follow” (Call p.16) | Q3 FY26 | N/A | Q2 FY26: no revenue contribution yet disclosed; | planning a market launch, but is delaying as product perfromance not satisfactory | No Progress Update (Red Flag) — silence in Q3 |

| Solar Pump Installations | “Target to install 1,10,000–1,20,000 solar pumps” (Q1FY26 Concall, pg 9) | FY26 | N/A | In Q2 FY26 Oswal installed 23,000 solar pumps out of 48,000 total pumps; | 90,000+ executed till Jan’26, 20463 solar pump sold in Q3 | On Track — strong execution continues |

| Total Pump Installations | “Plan to install 2,25,000–2,35,000 pumps (solar + non-solar)” (Q1FY26 Concall, pg 9) | FY26 | N/A | Q2 FY26: 48,000 total pumps vs 51,000 in Q1 – i.e., 99,000 pumps in H1.Needs acceleration. To hit mid-point 2.30 lakh, H2 must deliver ~1.31 lakh pumps (≈32–33k per quarter above Q2 rate). | Not explicitly disclosed in Q3 | Data Gap — transparency issue |

| Private Market+Export | Q2 Concall: Aggressive push on dealer-distributor & export network — “FY27 will show strong private & export business” | FY27 | N/A | Included in order book but % not disclosed | Slow Progress — still govt-heavy | |

| Capex – Solar Module Line | “1.2 GW solar module manufacturing capacity to meet DCR compliance” (Q1FY26 Concall, pg 12). Use IPO proceeds of ₹1,536.6 Mn to increase module capacity by 1,500 MW, in two phases: 0.75 GW in FY26, 0.75 GW in FY27; also integrate aluminium extrusion (₹433.6 Mn) and EVA manufacturing (₹268.1 Mn). Q2 concall: project shifted to adjacent land, but timeline unchanged. Q3 Concall: 1 GW by Q1 FY27, +0.5 GW by Q3 FY27 | FY26 commissioning/Phase-1 by FY26; Phase-2 by FY27 | N/A | Current installed module capacity 570 MW, with H1 FY26 utilisation 72.9%. No new capacity yet reflected in numbers; land shift approved. | Ongoing | On Track — phased execution |

| Magel Tyala Scheme Execution | “Maharashtra Govt target: 5 lakh pumps; Oswal current order: 8,500 pumps” (Q1FY26 Concall, pg 10) | Multi-year | N/A | Q2 FY26 disclosure: only aggregate KUSUM + Magel Tyala revenue; specific Magel Tyala revenue for Q2 is not broken out; order book includes Magel Tyala within 18,800 pumps. | Major contributor to growth | Double-edged — growth driver but causing receivable stress |

| PM-KUSUM Dependence Mitigation | “Explored large non-subsidy market; SBI loan tie-up for farmers (97% LTV)” (Q1FY26 Concall, pg 14) | FY26+ | N/A | Q2 FY26: revenue mix still 70–75% solar (mostly PM-KUSUM), 20–25% non-solar, implying >80% of revenue still subsidy / tender-linked; exports targeted at ~4% of FY26 revenue but Q2 contribution not yet highlighted as material. | No meaningful shift yet | Not Achieved — still highly dependent |

| PM KUSUM 2 | Q2 Update: to begin in Jan 26 | Jan, 2026 | N/A | Not yet launched | Pending Catalyst — key uncertainty | |

| Tender Rate Pressure | new EPC players are aggressively bidding lower – future tenders may see further rate pressure, though Oswal believes backward integration will protect margins. | N/A | Margin impact visible but controlled | Structural Risk — competition-led compression continues |

3 Likes