Story:

In India’s rapidly changing retail landscape, most investors focus on big names like Avenue Supermarts (D-Mart), Reliance Retail, or Jiomart. But beneath the surface, there are smaller players quietly building local brands, focused on regional markets. One such company is Osia Hyper Retail Limited, the operator of the Osia Hypermart chain.

Founded in 2013, Osia has grown steadily by setting up large-format retail stores in major cities of Gujarat, including Ahmedabad, Vadodara and other fast-growing urban areas.

The Business Model :

Osia follows a value retail model, targeting the urban middle class with a wide variety of products at affordable prices. It positions itself as a “one-stop shop” for family needs, offering:

Grocery and FMCG products

Apparel and fashion accessories

Home and kitchenware

Electronics, footwear, luggage, and more

What makes Osia different is its regional focus: instead of spreading thin across India, the company has built a strong presence in Gujarat — a state with rising disposable income and growing demand for modern retail.

Revenue Growth :

The Indian retail industry is massive compared to a company like Osia Hypermart. So, Osia’s growth depends more on how well the management runs the business than on the overall industry growth.

For large companies like D-Mart, the overall retail industry performance matters more because of their size. Even if D-Mart’s management tries hard, it’s difficult for the company to grow at 30% per year now due to its scale.

Quick commerce (like 10-minute deliveries) is growing fast, but it doesn’t impact Osia much. That’s because Osia targets middle-class and lower-middle-class customers, while quick commerce usually charges high delivery fees, which don’t suit this segment.

Osia’s management has set an ambitious goal: 150 stores, 2.1 million square feet of retail space, and ₹3,500 crore in revenue over the next 2–3 years. However, this seems too aggressive. In the last 3 years, the company has opened only 18 new stores and currently operates 47 stores. Going from 47 to 150 stores will take time.

Based on a more realistic view, Osia might open up to 160 stores over the next 10 years, with each store averaging ₹35 crore in annual revenue. That would bring total revenue to around ₹5,500 crore—about one-tenth the current size of D-Mart.

EBIT Margin:

Osia Hypermart currently has an EBIT margin (earnings before interest and tax) of 4.5%. There isn’t much room to improve this due to the nature of the retail business. Globally, the average retail EBIT margin is around 4.02%. So, it’s fair to assume Osia will maintain similar profit levels going forward..

Reinvestment:

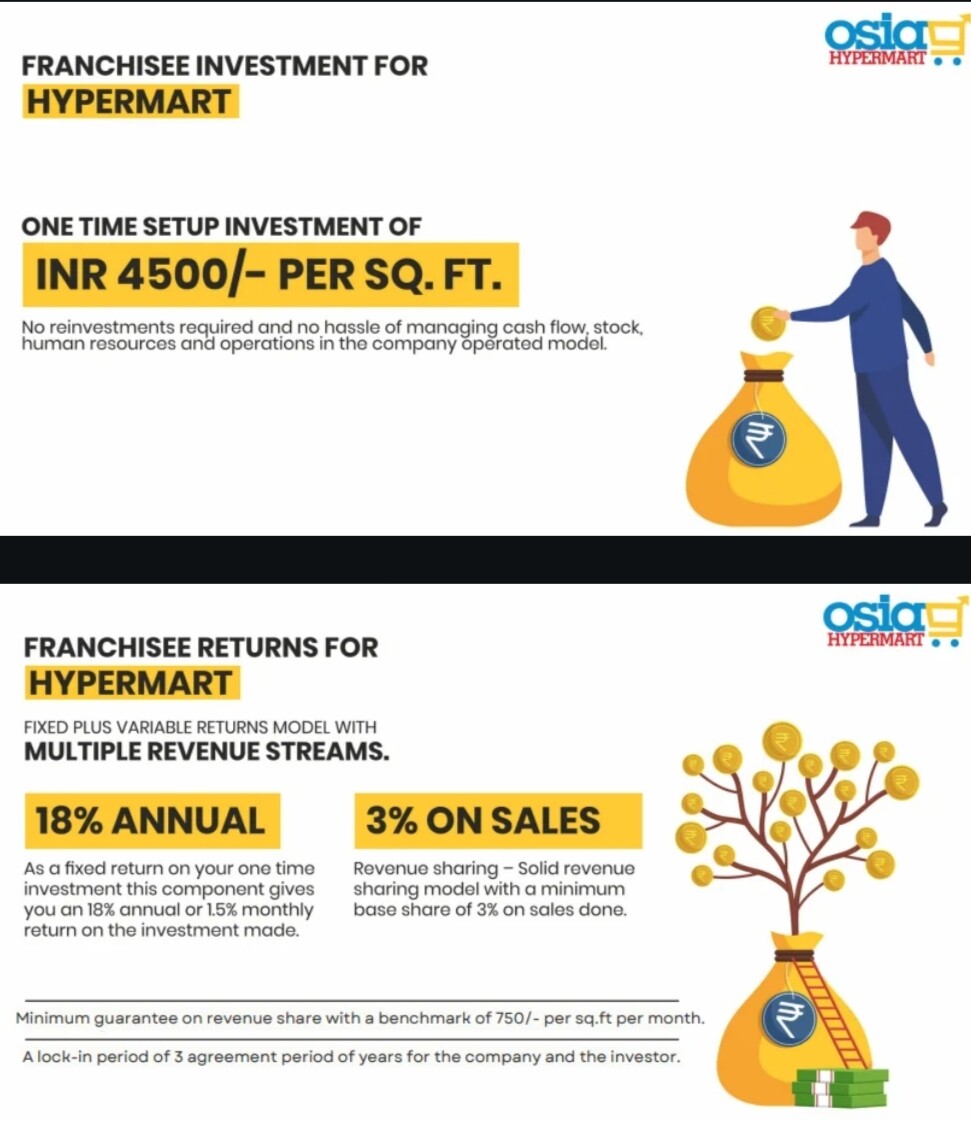

Osia uses a FOCO model—Franchisee Owned, Company Operated. This means the franchise partner provides the property and infrastructure, while Osia runs the store operations. franchise partners get:

Around 18% fixed annual return on their investment

An extra 3% of the store’s monthly net sales

Breakeven in 2–3 years, helped by Osia’s centralized procurement and vendor tie-ups

Because of this franchise model, Osia doesn’t need to invest much of its own money to expand. Thats why company has a high sales-to-capital ratio of 4, meaning it can generate ₹4 in sales for every ₹1 of capital invested—an efficient use of funds.

Risk/Failure rate :

Osia sells essential, daily-use products like groceries and home items — stuff people always need. That’s a good thing. It means Osia’s business is stable and less affected by market ups and downs. This is why it has a low beta (0.62), meaning it’s less risky than the stock market overall.

But here’s the catch:

Osia doesn’t have anything truly unique. There’s no strong brand moat, no exclusive product lines, no cutting-edge tech, or deep loyalty programs. Its FOCO (Franchisee Owned, Company Operated) model is easy for others to copy. Bigger players with better pricing, faster delivery, and stronger supply chains can quickly take market share.

On top of that, there’s a major red flag:

Credit rating agency Crisil downgraded Osia to ‘D’, meaning default level. That’s serious. It happened because the company delayed payments under its vendor financing system (TReDS) — and also didn’t share its financials with the agency.

But here’s the confusing part — Osia mostly runs on a cash-and-carry model, where customers pay before they buy. So who’s not paying on time?

One possible reason: Osia may have business clients (B2B) or institutional partners who are delaying payments. Since the company hasn’t clarified the details, we’re left guessing.

Because of these warning signs — weak competitive moat, cash flow stress, and poor communication with rating agencies — we estimate a failure risk of 35%.

This isn’t based on a formula. It’s a gut call based on signs of stress.

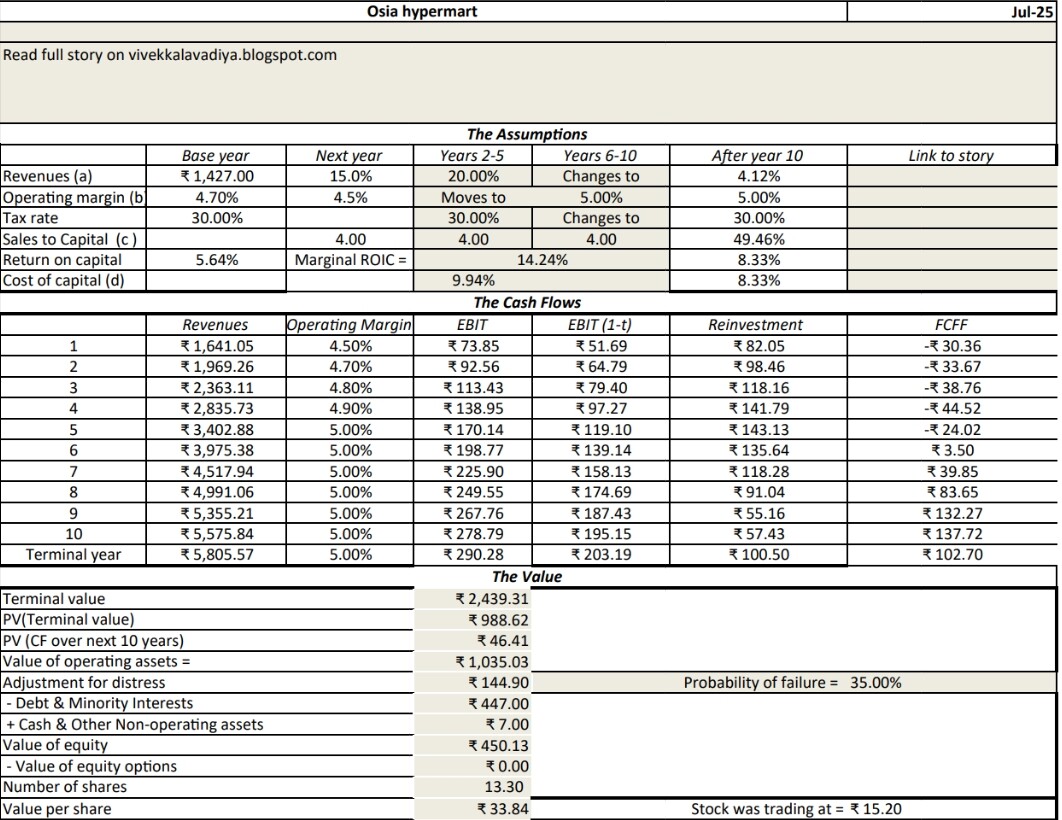

DCF valuation :

Data & Spreadsheets:

Edited after lock thread:

My intention is not to say whether the company is overvalued or undervalued. The purpose of this post is to show how easily you can value any company using a simple DCF model based on just four parameters: revenue growth, profit margin, reinvestment rate, and risk/failure rate.

Even a poorly run or distressed company can be valued using this method. If Osia’s management runs the business efficiently—like D-Mart has done—then the company could be worth ₹6,500 crore (about 4.5 times its sales), not just ₹450 crore.

I’ve already shared the Excel file. You can download it and put your own assumptions. Please don’t rely on my numbers. If you believe the company is a fraud, just set the failure rate to 100%—you’ll get a value per share of zero.

Uncertainty is part of investing. We can’t avoid a discussion just because it’s difficult. In fact, I prefer to study companies that are hard to value.

If someone wants to lock this thread and avoid discussion, that’s their choice—but I’m here to explore and learn, not to please everyone.