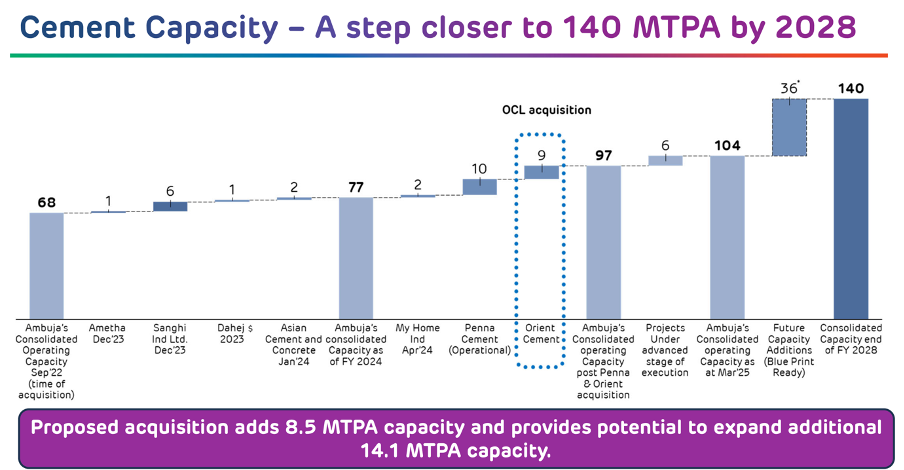

CMP: Rs. 138/-; Market Cap: Rs. 2835 Cr ; Total Debt : Rs. 1300 Cr; Total Capacity: 8 Million Ton at present and going to go up to about 11 MT ton by end of 2018.

I look into Cement sector companies when earnings are depressed for a company who has established capacities and capabilities for itself and running at low capacity utilization; having easy availability of raw materials at close proximity to the plants;, have captive power plants and low transportation cost to reach end customers vis a vis it’s neighboring competitors. Second level parameters to check are macros… Like if we are getting into lower interest rate cycle, if the sectoral tailwind is available for the infrastructure and housing sector and if the company is having new capacities coming on stream when demand pick up and price pick up is highly likely. Added to these possibilities we find two more general characters of successful Cement play which are critical to benefit the industry biggies … No significant new capacity in the greenfield are expected to come on stream in coming 3 - 4 years in the market catered by target companies and a large production capacity across geography which can withstand sudden local adverse developments which can sqeeze volume or margin in a specific state or geography like sudden flood, political disturbance or election or other local issues.

Orient Cement, the C K Birla Group company has 8 million total capacity ---- 3 million integrated plant in Adilabad in AP; 2 million grinding unit in Jalgaon in Maharashtra and new 3 million integrated plant in Gulbarga, Karnataka. Post acquisition of 74% stake in Bhilai Jaypee Cement Limited (BJCL) and Nilgrie Grinding unit from Jaypee Power venture Venture Limited would subsequently increase the theoretical capacity to 11.5 MT soon. It would also make Orient Cement a formidable pan India player.

Presently, the old two plants are running at capacity utilization of about 58% with poor realization . The reasons for poor performance are manifold … Rain in the manufacturing area in AP resulted in a lower sale and higher power and fuel cost due to wet coal usage; closure of power plants in Jalgaon Area of Maharashtra substantially reduced availability to Fly Cash in Jalgaon plant resulting in lower sales and higher freight cost for bringing Fly Ash from distant location to run the plant. The newest plant in Chttapur, Gulbarga, is running at below 50% as it is not yet fully commissioned. We can expect at least 2.1 MT sales from here in FY 18. In FY 17, total sales from here can be at most 1.4 MT. But for last two months power plants in Jalgaon resumed operation and post monsoon, we can hope wet coal issue may not be there and also the company commissioned a new stacker reclaimer which would reduce the problem.

The acquisitions of two new plants are value accretive. The BJCl plant consists of 1.1 MT of clinker, 2.2 MT of grinding (with committed slag availability from Bhilai Steel Plant) and 2 MT grinding capacity with Jaypee Power Venture unit assuring ready availability of Fly Ash. The acquisition of 74% stake in BJCL would cost Rs. 1450 Cr and purchase of Nilgrie Grinding unit would cost Rs. 500 Cr. Both together seems to be bought at a good price of US$ 98 / Ton which compares well with recent purchases apart from Sagar Cement purchase of BMM Cement which was stuck at US$ 78 / Ton. The cost of grinding unit was one of the very competitive for recent time at only US$ 35 / ton and almost same as the price paid by Shree Cement even though Shree bought a lower capacity plant.

We feel, the price of cement and growth of cement demand would likely to be high for coming few years especially in Eastern, Central, Southern and Western Region where in one year time, the orient Cement capacities would be fully available post integration with Jaypee plants.

Historically Orient Cement is an efficient producer and having a good track record with 2700 + dealer network across its target geography. But the sluggish demand recovery has depressed its financials in recent time.

The balance sheet is bloated due to recent capacity expansion and may further bloat due to Jaypee deal of about Rs. 2000 Cr. We expect, it may raise loan of another Ts. 650 Cr and also may raise a QIP for the balance amount.

However, three likely trigger can work in it’s favor … New capacities going on stream, demand pick up in the target geographies and better price realization due to demand and consolidation of suppliers and absence of new capacity.

We feel net sales volume, realization and EBITDA / Ton to grow significantly in coming two years and with reduction im interest rate, we feel the overhang of high level of borrowing may not be detrimental to interest of minority investors.

The ROE generated by Orient in better times were in the range of 30% … If things go as per way we are projecting, by next two years, unless significant dilution takes place, ROE can climb back to previous level or in its vicinity from current abysmal low level of 7.5%. But these turnaround times provide best risk adjusted upside scenario for a new investor.

Views invited.

Mandatory disclosure: The author is SEBI registered investment adviser and NISM certified Research analyst and runs investment advisory firm https://aveksatequity.com. The author is invested in the stock and advised the members of his website to buy it at a lower price level than current price. No trading has been done in the stock in last 30 days by the author or his family members or business associates. This is neither a recommendation to buy or sell or hold the stock. This discussion is purely for analysis purpose. Please do your due diligence before making any decision to invest or seek help from your SEBI registered investment adviser. .