Every IT system integrator across globe is OFSS partner. e.g. Accenture

https://partner-finder.oracle.com/catalog/scr/Solution/SCSP-ZZTVPBTE.html

If you search Oracle partner finder with banking you will get list of 100s of companies.

Every IT system integrator across globe is OFSS partner. e.g. Accenture

https://partner-finder.oracle.com/catalog/scr/Solution/SCSP-ZZTVPBTE.html

If you search Oracle partner finder with banking you will get list of 100s of companies.

This is parent website and it seems to represent system integrators for their ERP suite and not OFSS products…

OFSS doesn’t have own website

OFSS annual report is out. Has good content in Letter to shareholder and Management Discussion and Analysis for understanding of products and market position.

Bloomberg has Dolat Capital’s analysis of annual report (It is behind pay-wall)

51f9f4d5-5818-4f96-b1b2-9e498a968a90.pdf (2.1 MB)

Results are out and Slowly but surely this mnc giant continues to awaken. They hit their highest ever revenues and profits in Q1Fy21 and have now beaten even that to record a new high at 1397 crores revenue and 524 crores profit for Q1FY22. Deals seem to be pouring in as per disclosure with Operating margins still above 50 percent and net margins at 38 percent… Considering the lumpy nature of the business and the chance that margins will cool a bit the next few quarters may not be as great but the trajectory is fantastic and hopefully continues with this YoY improvement. Market is rewarding it too by taking the price near all time high. The IT Bfsi space is looking very interesting.

Disc: Invested since end of February. The 6.7 percent dividend yield alone made this a good buy back then and the operating margins + return of growth(though whether this continues remains a wait and see with no management guidance) and now obvious tailwinds in this Bfsi space could continue making this a dark horse in the IT sector. Cautiously optimistic.

Q1 tends to be their highest quarter as parent Oracle FY ends on May 31 and there is lot of ales push in the quarter.

Revenue growth is still very tepid, compared to Temenos, or even Intellect Design. OFSS has a very strong product, but management is not very aggressive in chasing growth.

Banking Technology space has a lot of tailwind, but OFSS needs to capture it. OFSS is also among the lower paying companies in the space, and I would not be surprised if attrition becomes a big challenge. Last quarters calls by Nucleus and this quarters call by Intellect design management have highlighted that attrition has become a major challenge. Unlike service companies, for product companies, attrition is a bigger risk, as domain and product architecture expertise is not very fungible.

Disc: Invested and holding since a while. Firm believer in the Financial Technology Products space, also invested in IDA, Nucleus, and reluctantly sold out Majesco when they got acquired by Thoma Bravo.

Decent results last quarter.

CAGR of 7% projected for revenue for a long period. Oracle in leader pack may manage higher growth. Profits will easily grow at CAGR of 12%+

Still valued fairly compared to other IT services and products companies at 20PE

This has been a 5000 bagger for Ajay Bagga. He talks about this in this video

Although I was not expecting bumper results but was certainly not expecting QoQ degrowth. It is clear that new capabilities like cloud are not playing out well for OFSS.

@nav_1996 - Wanted to get your & other investors view who are invested sincerely with good percentage in this stock. When entire IT industry is having tailwinds and OFSS is struggling for growth, is it worth a higher allocation? What is not working for its Cloud & new offerings?

Disc: Invested & hence critical. It is my highest allocation by cost in IT basket started around couple year back. Seems very soon it is turning out to lowest allocation by current market value, hence evaluating my investment. not a buy/sell recommendation. I can be wrong in my assessments

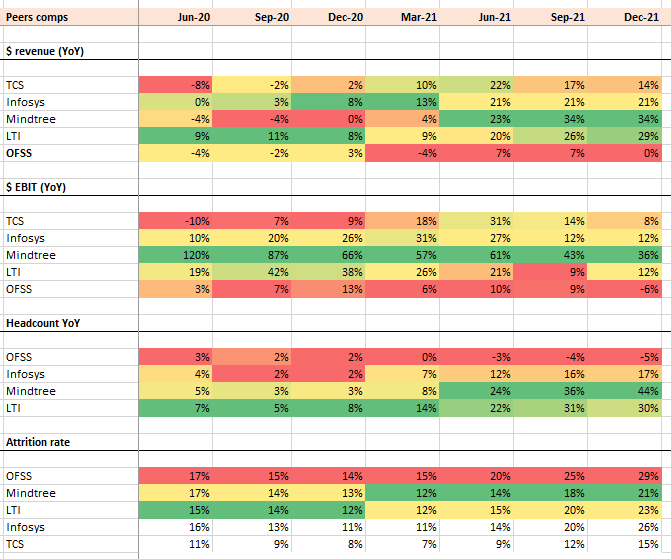

Growth: OFSS reported 3Q revenues of US$169mn, which was a 2.5% QoQ decline and flat YoY. This was weak and follows previous two quarters with 7% US$ rev. growth. This is also the lowest versus most IT peers who have reported thus par. Peers, infact, have seen an acceleration in QoQ growth rates. Two-year CAGR for OFSS is 2% versus mid-teens for the sector. The products business grew 3% while the services piece declined 4%.

• Profitability: EBIT margins for the quarter declined 320bps; this was in-line with the margin erosion seen at peers, and likely reflects 1) higher wage costs due to supply side challenges 2) marginal comeback of travel and marketing costs. However, note that OFSS’ margin contraction was sharper than peers. This is despite the positive mix as high margin products segment grew ahead of services. This may be mildly indicative of pressure on OFSS’ pricing structure with clients.

• Deal wins: OFSS signed new deals worth US$16mn this quarter which was down 18% YoY. TTM basis, deal wins have fared alright and have grown 6% YoY. However, deal wins have come off over the last two quarters after peaking at US$38mn in the June-21 quarter. The slight moderation in deal activity is in line with what has been seen for the wider sector but will remain a key monitorable.

• Headcount metrics remain substantially weaker versus peers; OFSS’ headcount declined for the last three quarters (3Q was -5% YoY) which is surprising given peers have shown very strong headcount addition at 25-40%. This is partly explained by the revenue decline in the IT services business which is more headcount driven versus the products business. Nevertheless, this is worrying given headcount is the building block of any IT services business.

• Attrition has reached 29% in 3Q, which is double of last year and is reflective of acute talent shortages in the sector currently. We have seen a sharp pick up in attrition across the board with most companies at >20% for the Dec quarter. Here too, OFSS is higher than peers. ~30% attrition means competition is poaching OFSS’ employees and this can impact the company in two ways 1) higher wage costs via retainer hikes or resorting to expensive subcontracting 2) headcount shortages leading to project execution delays which is a risky affair.

Do you have any data points on the cloud part of their business? Are they working on making their product offering more inclined towards Cloud and digital. Is there any SaaS aspect seen currently or in future as part of their vision of their Products?

I think above points are more important for long term growth. Any data point is welcome

Core banking is still a very on premise kind of product, mostly due to security concerns, but also fear of disruption in the change, so “dont fix it if it is not broken” continues. Migration to cloud/public cloud will be slow. Looks at the slow progress made by HDFC Bank on the tech side, despite the severe rap from RBI.

The big opportunity for OFSS is replacement of older custom systems at banks, and Temenos has done really well there. OFSS is very profitable business for Oracle, but unfortunately they are not very aggressive in investing for growth. And they dont communicate much abut their plans, so visibility for investors is low, unlike Intellect where Arun Jain is very vocal about what he is thinking. And Oracle Inc. probably wants to delist it as and when they can, so low communication makes it easier to drive prospective investors away.

Disc: Invested, am not expecting fireworks from OFSS, but expect it to be a steady low growth company, with a decent dividend yield.

Agree, so that should be bread and butter for OFSS…but for growth there should ideally be value added/new topping/new products which would be in pace with ongoing/upcoming technology…which is cloud/digital/SaaS at present

Will OFSS not have to compete with Temenos and other players like Quartz (TCS), Finnacle (Infosys), Intellect etc. for this piece?

When Intellect is focussing on Cloud & SaaS, I do not understand why this market leader, at least among Indian listed firm in this space, has no focus in this space…inspite of the parent being one of leaders in Cloud - Oracle Cloud, Oracle Fusion etc…

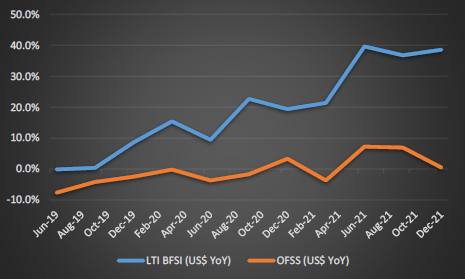

Just to sight an example, LTI works with competing platform products made by Temenos, etc for their BFS practice. And their growth of the BFS vertical versus that of OFSS gives some cues.

[quote=“Investor_No_1, post:127, topic:34, full:true”]

Problem is lack of focus on growth from the parent, this division is a very tiny fraction of revenues, in a slowly growing market, which has fierce competition. Look at he planned divestment /defocus of the services business, it is slowly bleeding to death. They tried to sell it, but did not get a good price and have just left it to die slowly on its own. Not a sign of very dynamic management that wants to get on with things.

Yes it is a very competitive market, and the sales cycles are very log drawn, we can see this in the “destiny deals” discussions on the Intellect earnings calls. Temenos/ Finastra/Intellect would be the major competitors. TCS relevant product is “Bancs”. Quartz is their DLT product, I doubt that has serious traction. Everyone talks about it and have sandboxes, but not much real work is going on with DLT at banks. And TCS /Infy are ore focused on the services they can upsell, so the core Finacle/Bacs does not really work like a prodct, it is heavily customized. Nucleus has the same problem with its lending suite.

Oracle Inc is actually a laggard in the cloud, despite trying very hard. The best of breed planers like Salesforce in CRM and Workday in HCM, Financials are far ahead.

Yes, Temenos is executing very well ( 20 % growth last qtr), and their partners have good traction too. However, not strictly apples to apples comparison, LTI is services business with NPM of 15 % and they have a lot of custom integration, migration etc work, other is a products business with NPM of 35 %.

And looking at Temenos vs Ofss, the markets have rewarded the growth with a PE of 50, despite significant debt on the Balance sheet, while OFSS trades in the High teens, and is a cash rich company.

The upside is there if OFSS shows decent growth, does not have to be blockbuster growth. Till then I see it as a Dividend paying utility, like the other sleeping beauty - ITC !.