How do we know OFSS is not being managed for cash given where margins are.

Given they have struggled with growth for many years I am guessing they will need new products to drive commercial traction. Has management given any clarity what specific products/ areas are they investing in?

@nav_1996 I have been studying the Bfsi sector intently and have decided that the best way to play it’s growth would be via the digitization angle. The price drop got me interested too… just had a couple questions

Apart from the annual report and news articles Is there any way of tracking the company? They haven’t conducted Concalls or given presentations for a while. Does the parent company conduct Concalls and if so do they talk about ofss?

Company has about 3 years worth of profits available as cash. Dividend wasn’t paid in FY19. Was this to grow the company ie develop new products/upgrade existing ones/cloud centers? I’m not too worried about whether it is a cash cow for the parent or not since we LL get a hefty dividend if that’s the case but if not dividend where are they spending the money?

This business is very sticky since switching seems to be too high a cost and unnecessary. However, is there any data regards how much their existing customers have paid them over the last decade and how much they are currently paying them annually? There seems to be no data regards new clients so wondering how they leverage existing clients for growth

There was an other income that rose from 100 or so crores to 674 crores and has since fallen back to 100 or so crores this year. Any idea what this other income was and why it’s decreased back to 100s again?

Considering operating profits alone OFSS has grown at a respectable 75 percent overall since 2014. Nothing crazy but more than the rate of PAT which has grown under 50 percent overall since.

Very interested to add it to my IT/Tech Bfsi basket since it offers downside protection currently with the Tailwinds in its sector and the huge amount of cash in hand allowing them to atleast maintain a healthy 80 percent dividend payout if not the current inflated percent yield. Add to this the fact that Operating profit has increased from around 2185 crores to 2444 crores over the past 1 year (TTM Vs previous 4 quarters) ie at 12 percent(higher tax rate and lower other income made the PAT look a bit flat) and hence looks like there really is potential for some growth for the core business. The problem is its difficult to pinpoint what is causing this growth and what the future plans are since communication seems to be nil from management. Any colour to help with the questions above would be much appreciated. Thanks.

Disc: not invested. Invested in Intellect design arena And expleo in my BFSI basket. Not a sebi advisor.

I don’t have answers to most of questions you have raised. It operates like a typical MNC subsidiary. Look at Bosch/3M/Honeywell.

If management would come forward and gave those details, it would be trading at least at 25 PE and not 15.

But I am confident that US companies like Oracle/MSFT etc operate with fairly high level of corporate governance.

I look at broad picture and don’t over analyze. Feel comfortable where this company is headed. My hurdle rate is just 10% returns with downside protection. This is definitely not like stocks which double every year.

@nprao They operate in Banking have complete suite of banking products and yes they keep upgrading their products to remain relevant. Please read AR to get complete picture.

You can refer to Dolat report on OFSS. You may need to login on trendlyne to access this. This is free

Cheers @nav_1996

Literally the only thing preventing me investing is the lack of management commentary. Do they talk about ofss in their parent concalls abroad? Il do some digging to find out.

Btw mastek thread there’s talks about huge demand for Oracle cloud(as seen through evosys) so there could be something huge brewing here and downside looks protected currently. Dolat capital covered it in November and mentioned new deals and traction in bfsi too. The way I see it is they could have a good few 5 or so years where they’ll be generating more cash than they could possibly need and we could see bigger and bigger dividend payouts during this virtuous cycle along with 8 to 10 percent growth which makes the current price a bit of a steal. Problem is we need to extrapolate info randomly from other sources to figure this out and not directly from management

Disc: Not invested. And not a sebi advisor.

Agree with what you say, but how I see it is this way - Investing is all about extrapolating. Even if we take case of those management who do concalls and give all data, we at end of day are only extrapolating “what they say”, “what they make us believe”. And many times, They go wrong. They are but “only humans”

But I agree, not finding any significant data about this company is a bit annoying at times. And main reason could be as you say with management itself not sharing enough data.

There is no denying the fact that they have one of best BFSI product for core banking and also Insurance related products. They have backbone support of Oracle cloud. Oracle (parent) does not seem to be behind in cloud anymore. Also, I see OFSS also evolving their offerings with ongoing digital and analytics. So - These are indirect data I have to do an intangible extrapolation. BFSI would grow, need for technology in BFSI would grow and I have an MNC from stable of Oracle here. It will be a pity if Oracle does not end up growing this capability of theirs they acquired from I-Flex.

I do not see a point on why they acquired this business in first place if they do not intend to grow it or it is not their focus area. (Unless any significant top management change, along with Strategy change, happened since then…Would be good to have more insights on any change in Strategy of management since they acquired this business)?

Disc: Invested and biased, gradually building more position. Pls note above are just personal thoughts and I maybe completely wrong. Not a buy/sell recommendation

Alphabet and Google (GOOG +4.2%, GOOGL +4.3%) will stop using Oracle (ORCL +3.3%) for its internal financial software in the next few weeks, CNBC reports.

Although linked to parent Oracle, but this doesn’t seem to be related to OFSS in any way. (as per my understanding of OFSS business line). OFSS is erstwhile IFlex and its product is Flexcube, which is used by Banks, Insurance companies etc.

Google etc. seem to stop using the Oracle Finance ERP module from parent Oracle and OFSS products is meant for financial institutions…

Agree that it looks attractive at this price and the FCF yield. But isn’t the above analysis a bit too simplistic? Stock has been flat for five years and I dont think it compounds at 10% (screener grab below). Surely, I am missing something here. Thanks.

The only issue with this growth is that INR depreciation accounts for 5% of this. So the constant currency sales growth and EBIT growth would be 3-4% at best versus double that for other IT cos. So lets assume for a bit that INR remains here for the next five years; you will have sub 5% growth.

Also my more fundamental worry is that there is something wrong with this mid cap IT company if even the IT behemoths compound earnings steadily at double its rate. I could be wrong just sharing my two cents.

PAT(Consolidated) has taken a huge jump YoY but it doesn’t look sustainable since margins were improved due to travel costs etc. Revenue has dipped a bit though for the year overall it’s flat(and not negative).

The good news is that dividend of rs. 200 declared so buying it at under rs. 3000 seems to have offered a nice MOS which will be supported by this increasing yield every year. As usual information is scarce but they have added this slide:

Looks like they have a lot of interest in their products and hopefully the annual report + AGM gives us a clue regards what to expect in FY22. Quietly confident to continue holding it from lower levels and watch FY22 play out

Thanks, I am ok with the results…was expecting slightly QoQ improvement though maybe 2%…but its ok for me.

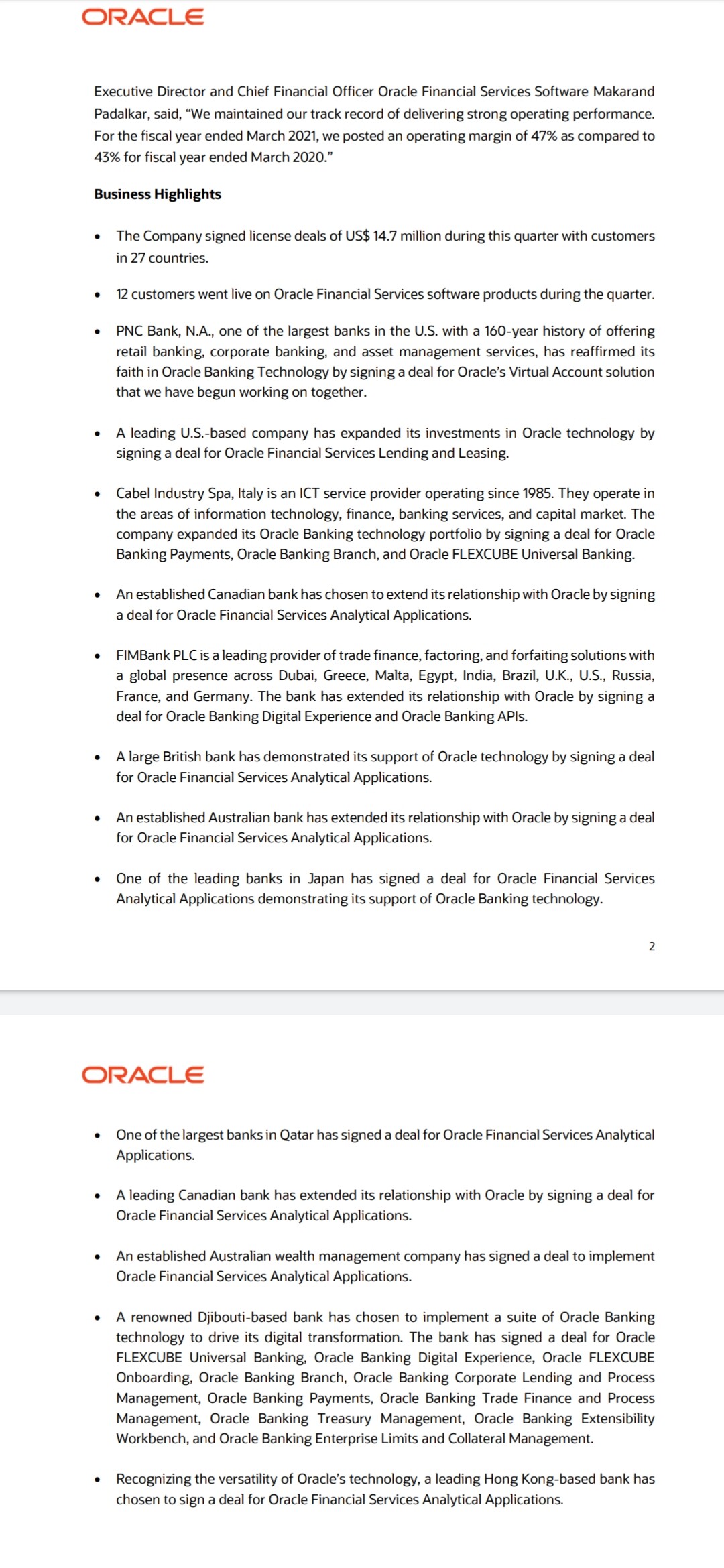

Whats something I would want to dig deeper is that 27 new licence deal in this Q is worth only approx 15 million $. Thats too less, when even small companies like LTTS are signing two 25 million $ deals and quite a few 10 million $ deals in the Q.

But guess thats how this Product business is.

What I want to dig deeper is that above 15 million $ is only the licence fees and not the full deal value? As I would anticipate for full deal value, OFSS would milk the new licencee over time with maintenence, upgrades and support? Insights would really help here from those more aware of Product licence business!..specially how say a 25 million $ deal of LTTS is different from 15 million $ licence deal of OFSS (via 27 new licencees for eg.)

Also as @Rohit_Kadam rightly pointed out, this stock and its revenues have hardly done anything over almost a decade…

My investment thesis in this company was never QoQ growth though…for that I have chosen other IT services in the basket. It forms approx 2% of my portfolio only and idea here is to remain invested for any spurt in growth with any new Product and/or Product extension…however if 27 new licences mean total deal value of only 15 million $, then my thesis of spurt in growth with Product extension needs revisiting…

Also, MNC restructuring, buybacks, dividend would make this behave like an FD until any spurt happens, if at all it happens. In due course, I might sell if I see the management not intended to grow or if I feel the MNC parent is not serious about this Indian subsidiary.

Disc: Not a buy/sell recommendation. Only my though process on this business. My thoughts can change anytime in future and I can be completely wrong in my assessments

We need to keep in mind that OFSS has clientele evenly distributed across globe not just west. Now western clients are getting comfortable with deal making in digital mode. Clients from asia and africa still want to have face2face meetings. This Q is first Q in most countries when new deals discussion start. Now 2020 same Q travel was on whereas in 2021 travel was minimal. So any discussions with customers for new deals which would have ideally got concluded in F2F meetings will take longer.

Also, customers are themselves likely to be impacted.

So, OFSS is likely to have an impact due to Covid, unlike IT services companies where bulk of revenue comes from US.

Also, one shouldn’t read too much in a Q results.

Temenos revenues grew 8% in same Q. So demand is there.

I am betting on cyclical play of banking software upgrade. Last decade was tepid so growth should play out this decade.

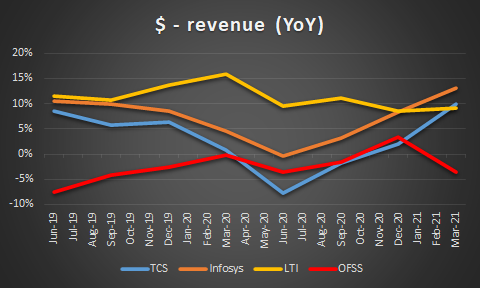

OFSS sales were showing an acceleration in line with peers until 9mFY21 however 4Q diverted from this as most peers continued to exhibit the accelerating trend in 4Q versus a decline for OFSS. On a sequential basis as well, most peers grew sales versus a decline for OFSS.

Sir, I’d recommend you leverage your professional network, if possible, and connect with OFSS employees to understand what is happening. Then you will understand why the market is valuing the company the way it is.

It wont be much of an exaggeration to say that OFSS at this stage is a collection of sunsetted products. OBP was supposed to be the next gen platform that would put the company back on growth track, but apart from maybe one or two big wins such as NAB it achieved no commercial traction.

The company is now working on a new cloud native product although this is happening at Oracle (not OFSS) with only loaned resource from OFSS.

All signs point to OFSS being managed for cash. In my opinion they will not return to material growth notwithstanding industry tailwinds.

Curious if that cloud native product is in Banking & Financial services domain, why it is not a part of OFSS but instead of parent Oracle? Is that Product a part of the Oracle Fusion ERP suite?

I wouldn’t just write them off based on people’s perception of them based on the past few years.

Q4 took a small hit since most of their deals came from developed countries only ie 10 out of 13. Developing countries demand was low. This is obviously due to covid being less of a threat in the developed countries and throwing developing countries in disarray. Developing countries will start contributing deal wise once covid dissipates. They had 13 new deals in Q4 but most of them were from Analytics/digital offerings which are lower ticket with just 4 being core. So demand is still high. Just that the mix of region and types of deals lowered the revenues this quarter. You can see this short term issue in results of other Bfsi companies in this space too.

Q1 is usually their best quarter for deals and I won’t be surprised if they show signs of breaking their revenue ceiling from Q1FY22 itself. Of course some of their costs will come back to normal so margins could drop a bit (but still be fantastically high above 45 percent) so profit may not grow at the same rate as revenues.

Growth is literally the only missing piece from this company(fantastic margins/cash flows/cash in hand/no existential threat/generous dividends/huge brands/good pricing power) and I wouldn’t be surprised at all if they start growing at double digits again soon and I wouldn’t be too quick dismiss it as a cash cow of the owners.

Disc: invested since lower levels and I’m very happily holding. Not a sebi advisor. Not a buy or sell recommendation. With contra bets like this a big margin of safety is required and I’m not sure it offers one after the runup to 52 week highs.