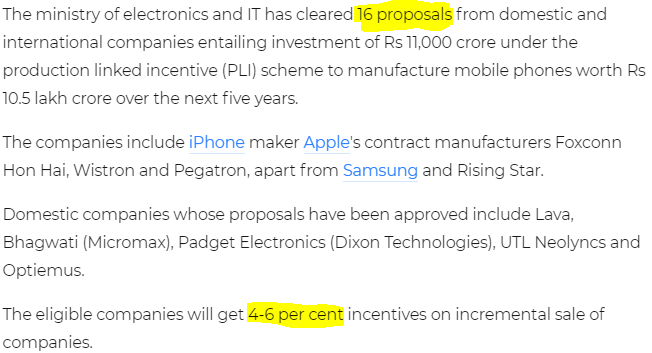

16 companies have got PLI scheme approval for mobile manufacturing.

Read more at:

Disc: Not invested, find this very speculative

16 companies have got PLI scheme approval for mobile manufacturing.

Read more at:

Disc: Not invested, find this very speculative

adding this image in a separate post, due to VP guidelines preventing new users from attaching multiple media items in the same post

Very Interesting comments here by A Gururaj, MD OEL:

Disc: Invested

23K Cr for Wistron

Noise had last year partnered with Optiemus Electronics Limited (OEL), a wholly-owned subsidiary of

Optiemus Infracom

NSE 9.52 % Limited, to manufacture products locally.

OEL is designing and manufacturing hearable products for Noise at its two plants in Noida.

“We have a very strong joint partnership with OEL. So we are with them as an exclusive partner. We have built that R&D arm with them who are helping us in building …

Read more at:

Truke Kick-Starts its Make-in-India Initiative Aiming to Produce 2 mil Audio Units/Yr by 2023

949d9d8d-02e0-4949-9ef0-7cce5db27176.pdf (3.1 MB)

Here is a great article by Forbes which acts as a starter for investors like me who want to decide on whether the company will walk the talk or fail yet again.

With this article I understood about the Management’s “Openness to Learning”. They have failed miserable in B2C business back to back with blackberry and then their own brand Zen. Hence, they have now imbibed the role of backhand manufacturing and hence B2B. Second, learning was that they have learnt from their earlier mistake and has moved beyond product concentration by diversifying their product mix.

Also, I observe that the appointment of Mr. A Gururaj has sparked the Optiemus 2.0.

Disclosure: I have entered a tracking position and will carefully watch the next quarters for whether or not these new advancements (partnerships + new factory +new* forray into hearables, laptops,etc) translates into growth of the company’s revenues. This will help me analyze and determine if the company can really scale upto the promised 38k Crore revenue in the next five years.

Wistron already has a tie-up with Optiemus for assembling iPhones at their Noida plant.

I am a bit surprised with this news as to why would Wistron be looking for another partner for the same project even when their existing partner already has the advantage through the PLI scheme?

In case a Tata-Wistron deal goes through, and Wistron continues with the Optiemus agreement too, I doubt that Tata Group will want to play second fiddle to Optiemus.

So where does it leave Optiemus’ upcoming Noida plant and their plans to reach the 38k crore revenue mark?

As far as I can see its not the same project.Wistron has facilities in Bengaluru that manufactures Iphones . The OIL JV was for other stuff…

Anyway, your link itself says that tatas can buy equity in wistrons India ops or create a new facility .None of it hampers OILs plans in anyway.

Disc. Invested

market is too vast and there is enough for every one. not only Taiwanese Indian brands will also look for manufacturing partners. Rift b/w China and Taiwan is another long term positive for India from manufacturing point of view. keep an eye on sales data, as long as it keep on rising ride the stock.

The stock has been range bound since last one year and given tie ups with Harman, Noise and plan to set up more factory, growth should explode in a few quarters then stock will cross all time high. Holding with patience since Dec 20.

Next quarter should be even better given increase in capacity, festive season. At some time it will come into radar of institutions also given vertical climb of revenue expected then will explode in valuation…

interesting article leads us to conclude OIL is in cusp huge market opportunity …

Interesting talk by Mr. A. Gururaj, MD of Optiemus Electronics on electronics manufacturing and design in India.

Dixon result and guidance both really poor. In a low margin business volume is vital. Hope optimums delivers this quarter as it will show tenacity of its business execution as it has announced many tie ups and it was festive season. They can do better in corporate governance also and make results timely and more transparent. It seems a convincing long term story, will hold irrespective of result

With Optiemus so strong focus on wearables and Mr. A Gururaj as a leader now, I expect Optiemus to deliver good results.

6 % topline, EPS growing by 75% QoQ at 1.46 quarterly and can hit double digit for next 12 months too going forward with PLI subsidy… Future looks bright