I have a question and if community can help me to clear up the confusion. I want to know the relation between net profit and operating cash flow. most of the time I see visible difference between net profit and operating cash flow. if the difference is quite stark, is it a sign of red flag. for ex, Asian paints. sharing screenshot. If you see there operating cash flow and net profit there is a visible difference and that’s my main confusion. Basically if any one can explain the correlation between PL statement and Cash from operation. Plz help.

Red flag is when CFO is much less than PAT, which usually means working capital needs are on the rise or all the profit company is making is being used to meet rising working capital needs. CFO is the fuel for the vehicle!

There is lots of content available online. Just research a bit yourself and you would understand.

There is usually a difference between Net profit and Operating cash flow due to non-cash transactions.

Major non cash transactions are Depreciation and Changes to working capital.

Depreciation is an expense considered in the income statement that the company does not actually pay in cash. Hence this needs to be added back to the profit in order to determine cash-flow.

Changes to working capital can be positive or negative to the cash flow. Increase in net working capital would reduce cash flow as cash is blocked in working capital. Decrease in net working capital would increase cash flow as cash that was blocked gets released.

For example: If the company makes sales, but does not get paid in cash, there is increase in receivables, which is an increase in net working capital, and would need to be reduced from the profits to arrive at the cash-flow.

Income statement and Balance sheet can be manipulated easily. Cash flow statement can not be manipulated. If there is huge difference between NP and CF then you need to dig deeper to know the reason. Also compare the Profit before tax with income tax paid to judge whether NP is manipulated or real.

In accrual accounting, income is recognized when it is earned and not when cash is received. Similarly expense is recognized when an obligation to pay is established and not when actual cash is paid.

There are also other non-cash items in P&L for which no cash is paid or received (.e.g depreciation, gain on sales of assets, etc.

Some items are also treated as investing or financing activities so these are added (or subtracted) to operating cashflow and subtracted (or added) from either investing or financing cashflow, e.g. interest income.

These 3 factors gives rise to difference between net profits and operating cashflow. A company should be able to convert net profits into cash fairly quickly and on a regular basis else it will not have any money to invest for growth or it will have to borrow money to invest or even pay its operating expenses. Such situation can get a company into a debt trap from which it may or not recover.

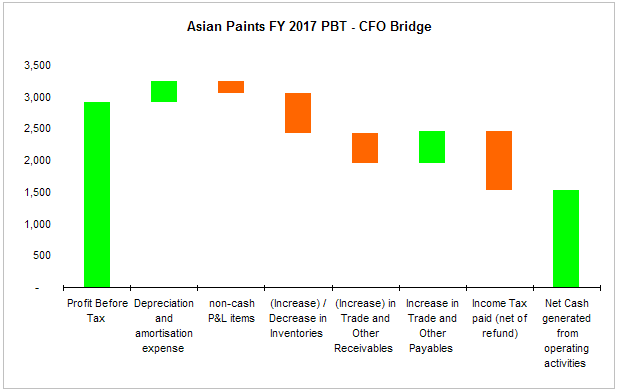

chart below shows a high level view of Asian Paints FY 2017 Profits Before Tax to Cashflow from Operations bridge.

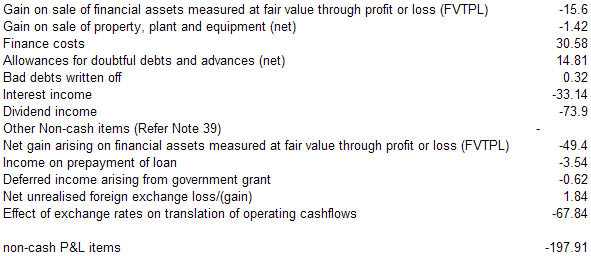

List of non-cash P&L items.

This shows that Asian paints’ CFO is lower than profits because increase in inventories and receivables is not fully offset by increase in payables. for a growing company like Asian Paints this is fairly common as working capital will grow over time and part of the profits will be invested in working capital. It still has plenty of cash left to buy fixed assets, pay dividends and retire debt.

If you observe CFO starts from Profit before tax(PBT) which also accounts for interest paid on various short and long term liablities of the organization. However CFO only records those transactions which involve inflow or outflow of cash in day to day basic operational activities. Interest payment is a financing activity(activities or transaction to finance the needs of org.) Henceforth Interest Payments are added back to PBT while calculating CFO.

Likewise Interest received be it on Investing(Mutual Funds etc, deposits,loans given) or Financing is not recorded in CFO since it’s not the mainstream source of revenues .So Interest received is deducted(As PBT also accounted for it) while calculating Cash from operations and added to CFI or CFF