Business Overview:

OneSource Specialty Pharma Limited (formerly Stelis Biopharma) is a specialty pharmaceutical Contract Development and Manufacturing Organization (CDMO), created through a strategic consolidation of soft gelatin, complex injectables, and biologics businesses from Strides Pharma Science and Steriscience.

Headquartered in Bengaluru the company focuses on B2B development and manufacturing of high-value dosage forms for global clients.

It offers end-to-end solutions including formulation development, tech transfer, scale-up, regulatory filing support, and commercial manufacturing. The company caters to global pharmaceutical innovators and generic companies, leveraging expertise in niche delivery systems and complex formulations.

Verticals:

a) Biologics

b) Soft Gelatin capsules

c) Complex and Drug-Device Combination (DDC)

d) Specialty Pharma services

Why DDC is preferable, you ask?

They are integrated products that combine a pharmaceutical drug with a medical device to deliver the therapy more effectively and safely. Examples include pre-filled syringes, auto-injectors (e.g., for insulin or biologics like semaglutide), inhalers, or drug-eluting stents.

Pharma companies prefer DDCs because they enhance patient outcomes, streamline administration, Competitive differentiation and IP Protection, cost efficiency in development and manufacturing, and align with regulatory and market trends

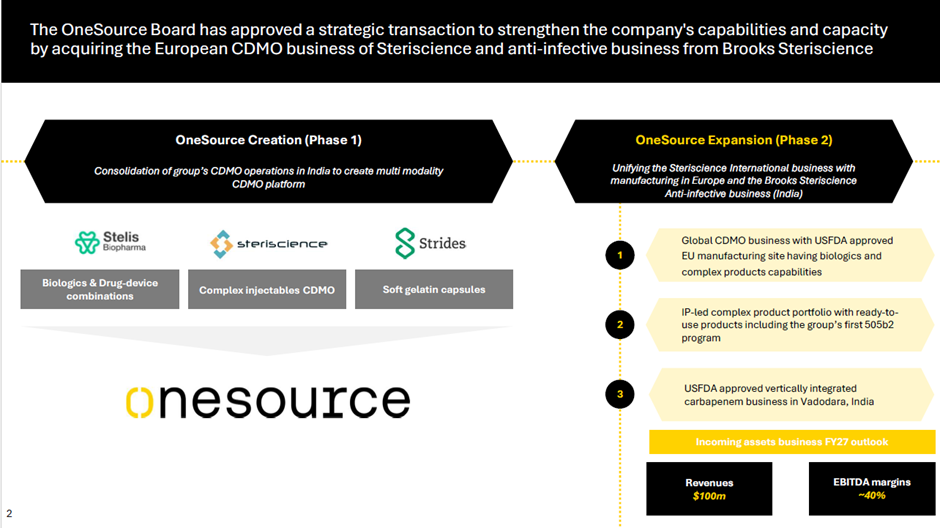

Strategic transaction:

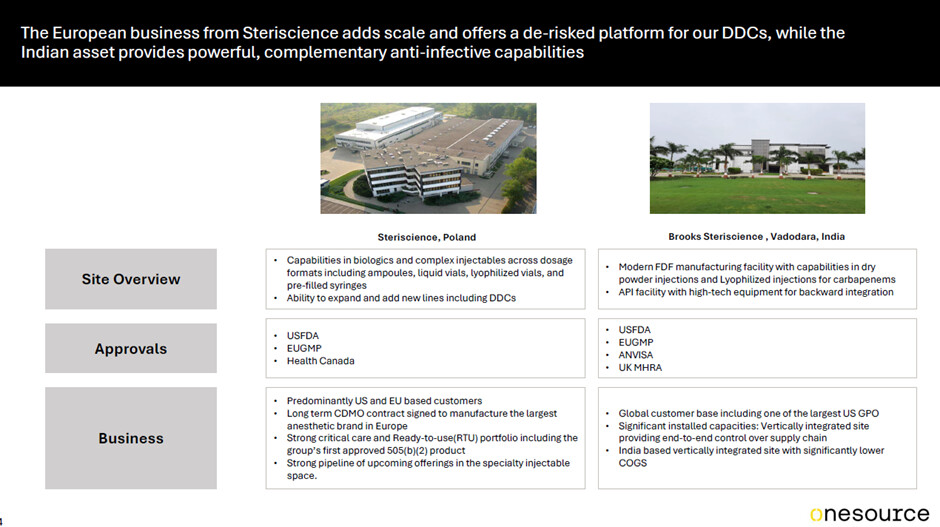

Stellis Biopharma and Steriscience have Plants in Poland and Baroda(India).

Key Investment Rationale:

GLP-1 Tailwinds:

OneSource is speeding up its capacity expansion plans (220mn cartridges by CY26) to leverage the generic GLP-1opportunity. Its base of over 20 customers for GLP-1 fill finish is likely to account for ~33% of the generic GLP-1 market. it is constantly endeavouring for more capacities.

Commercial supplies of semaglutide to start in H2FY26. It is estimated to have 33% of GLP-1 produces as client for Onesource Specialty Pharma.

It will start booking semaglutide revenue H2FY26 onwards and customers are likely to sell the

products in markets like Canada, Brazil, Saudi Arabia, India and other emerging markets. Its DDC business is likely to touch INR 14.7bn by FY27E.

It is estimated to have 50% revenue and EBIDTA by FY2027.

CDMO Platform with Multimodal capability. Multimodal capability enables it to address a wider range of client needs, from development to commercial-scale manufacturing. The company’s ability to serve both innovators and generics positions it favourably in the global outsourcing market, which is witnessing strong demand for specialty formulations. Its focused B2B model and differentiated service offerings provide long-term visibility, making it an attractive partner for global pharmaceutical players seeking complex dosage expertise.

Strategic Backing and Legacy of Strides Group The company benefits significantly from the legacy, governance, and commercial networks of Strides Pharma Science, which enhances credibility with global clients. During its scale-up phase, access to Strides’ infrastructure and front-end U.S. presence reduces business development costs and accelerates market penetration.

Tailwinds in Specialty Dosage CDMO The global CDMO market is experiencing a structural shift toward outsourcing of complex formulations, driven by pharma companies focusing on R&D over manufacturing. OneSource’s focus on high-value segments such as softgels, injectables, and biologics places it at the center of this trend. Its capabilities in niche delivery formats attract premium contracts with longer lifecycle visibility. As clients increasingly prefer single-source partners for development and manufacturing, OneSource is positioned to capture higher-margin opportunities with sustainable annuity-like revenues, supported by sticky customer relationships and regulatory accreditations.

Margin Expansion and Operating Leverage Potential It will be supported by operating leverage, improved asset utilization, and rationalization of transition costs. Backward integration.. The transition from legacy contracts to higher-value CDMO engagements offers upside potential in both margins and cash generation, critical for long-term compounding.

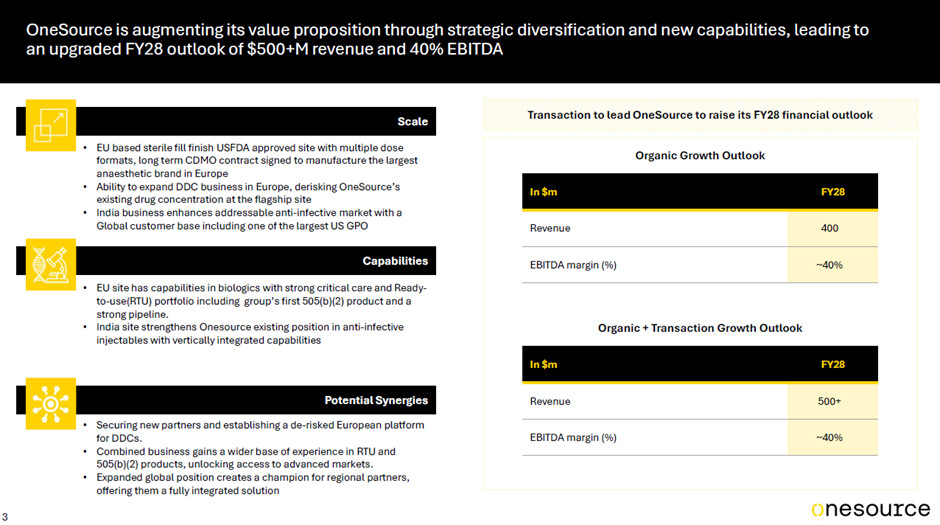

Growth Outlook:

Organic Growth Outlook of Revenue 400 million USD with EBIDTA margin of 40%.

Organic + Transaction Growth Outlook of Revenue 500 million USD with EBIDTA margin of 40%

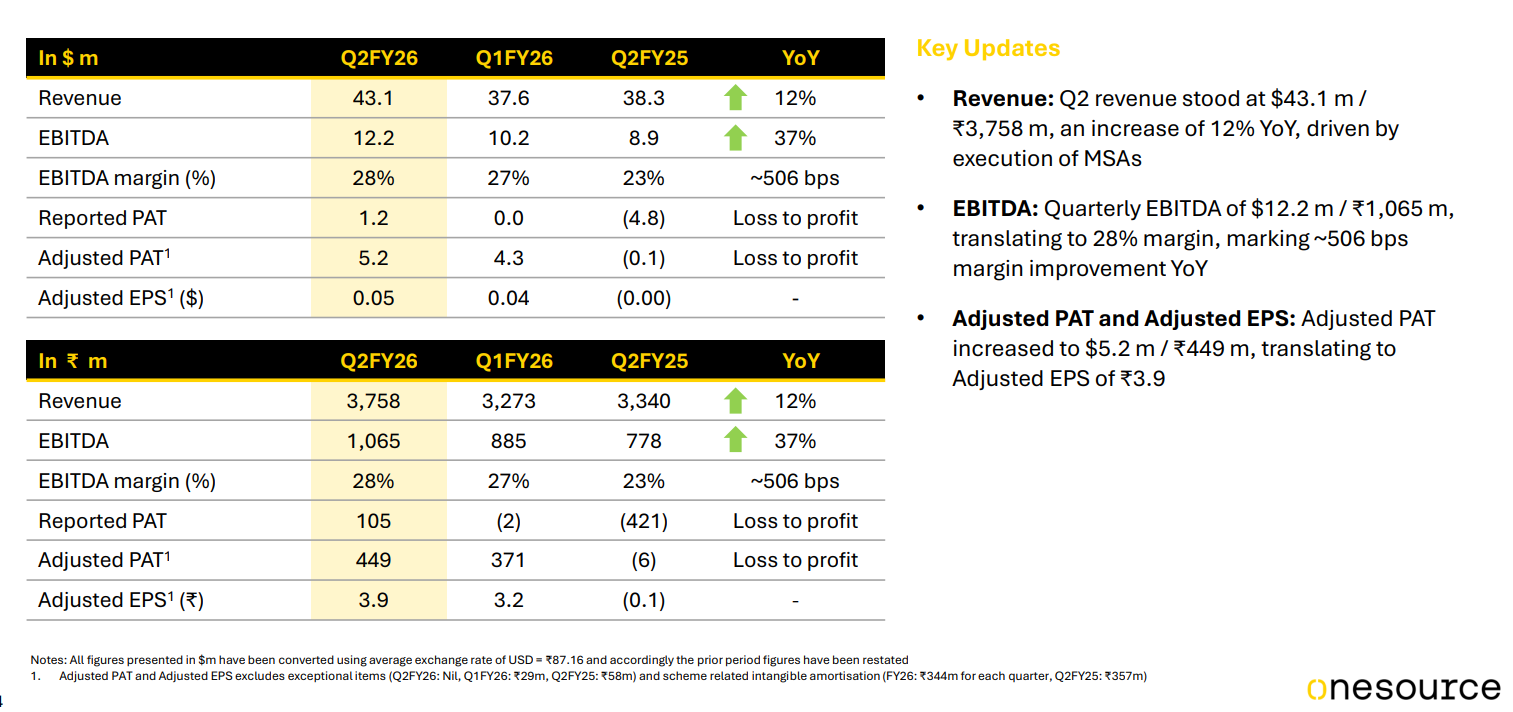

Q1 2025 Conference Call Highlight:

Generic market for semaglutide (GLP-1) is likely to open up from Q4FY26.

In H1FY26, the company has focused on executing Manufacturing Supply Agreement (MSA) contracts and H2FY26 onwards commercial supplies of semgaglutide will begin.

Most of its customers have increased their supply forecast for GLP-1 products for next 18-24 months. Most of the contracts entered by OneSource with its clients are take or pay.

What is take or pay, you ask?

A take-or-pay clause obligates the client (e.g., a pharmaceutical company) to either:

Take delivery of a minimum agreed quantity of products or services (e.g., manufactured drugs like semaglutide) from the CDMO, or

Pay a specified amount to the CDMO, even if they do not take the agreed-upon quantity.

This ensures the CDMO is compensated for reserving production capacity, resources, and investments, regardless of whether the client fully utilizes the committed volume.

The company has expedited phase 2 capacity expansion and now plans to have cartridge capacity of 220mn (40mn currently) in CY26. In FY26, it will have cartridge filling capacity of 40mn; in FY27, it will have the entire 220mn capacity in place.

The company expects limited number of companies to be present at the time of generic market formation, as the product is complex to manufacture.

The recent cut in guidance by Novo Nordisk is unlikely to have any material bearing on the potential market for generics.

In Brazil, company will initially launch gOzempic while gWegovy launch may happen post that.

In Q1FY26, it secured six new contracts and received 25 RFPs across all its offerings.

Strategic partnership with Xbrane strengthens its drug substance capabilities and accelerates regulatory inspection for the facility. The company has initiated tech transfer process, and it will take 12-18 months to complete.

Risk:

Client Concentration and Competitive Pressure**:**

Being an emerging CDMO, OneSource may have significant revenue dependence on a few anchor clients, including those transitioned from Strides. High client concentration exposes it to contract renegotiations, pricing pressure, or volume variability. Additionally, competition from established global CDMOs with larger scale and regulatory track record could challenge its ability to secure premium contracts, impacting long-term growth and margin sustainability.

Execution and |Integration Risk:

As Onesource required to migrate from stride pharma system to it’s own standalone system possess a risk for service delivery and operation efficiency. Delay in capacity ramp up, cost absorption and technology transfer etc also can materialize.

Regulatory:

As a CDMO operating in highly regulated markets such as the US and Europe, OneSource faces stringent audits, quality standards, and frequent regulatory inspections. Any non-compliance, warning letters, or delays in approvals can affect client confidence and contract renewals.

Valuation:

Rough calculations:

As per management guidance of FY2028, looking for revenue of 4400 cr ( 500 million USD). With 40% margin EBIDTA of 1750 cr (200 million USD). Net Profit of 1380 cr. EPS of 120.

Attractively placed compared to peers.

It is difficult to value such companies based only on PE ratio, as happened with me for NATCO, where once blockbuster drug goes away, what to do?

Disclosure: Invested