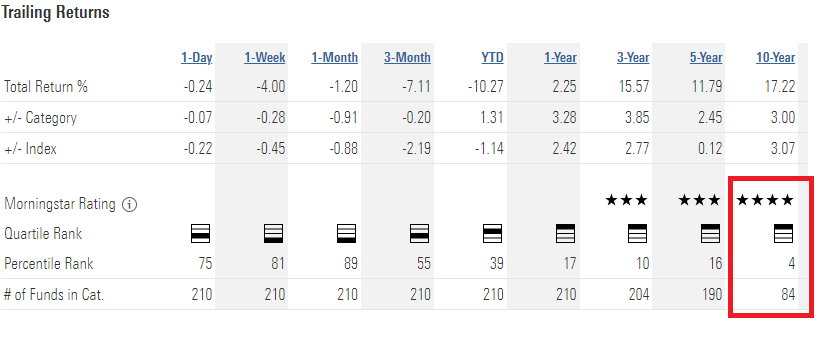

I will be completing 7 years with IDFC tax advantage ELSS next month and IRR as on today is descent 17.29% for seven years. I am personally very happy with the result. If I have to give one reason because which I was able to pull-out this result then it will be - holding my nerves and units I managed to gather from Jan 2018 to Mar 2020 when fund was underperforming benchmark over 5 years and when 5 years returns were low single digit. Axis long term equity is going through similar patch right now which is testing my patience. Following short note explains IDFC fund house style and ends with short comment on Axis’s underperformance

To Start with - Why I am investing in Multi cap strategies?

Some investors prefer combination of Large cap + Small cap funds but I personally prefer category which gives complete freedom to fund manager to execute their strategies. The real essence of fund management style comes out when manager has complete freedom to choose across market caps. The true art of fund management for Naren and Prashant Jain comes out in their multi cap strategies. It also becomes relatively easy for an investor to judge underperformance as compared to judging underperformance of small cap fund compared to peers.

Difference between IDFC and Axis strategy

IDFC amc’s (Anoop Bhaskar’s) way of looking at diversification is by looking at number of sectors in the portfolio rather than number of stocks. within a sector then they take exposure of multiple companies with lower % allocation to each company. For example - If they decide to own tyre companies they prefer to own three-four tyre stocks at 2-2.5 per cent each instead of one stock at 9 per cent. This feature of capping exposure to individual company, gives them edge to construct portfolio small-mid cap heavy. Higher weightage to small- mid cap makes portfolio - high beta in nature and that is why portfolio usually takes blow in the bear market but in bull market – they compensate more than they lost in bear market. This also gels well with the way Anoop bhaskar looks at AMC business which he has spoken about few times – ‘’contrary to protecting down side in bear market, it is important to do well in bull market as most of the fund inflows come in bull market’’

Even in their factsheet, IDFC AMC represents portfolio structure with their core philosophy of diversification as mentioned above . You can see fund manager tries to include as many sectors as he can. All of their multicap schemes have this as a common salient feature

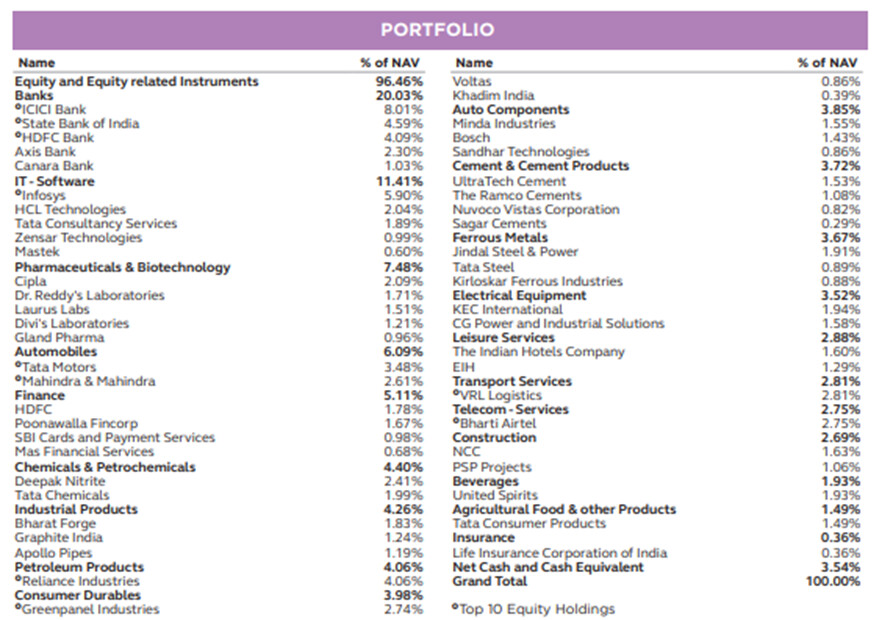

Axis style, as everyone knows, is sticking with so called ‘’Quality’’ companies and since most of these companies are large cap in nature, their way to create alpha is by concentrating on their bottom up selection. Example – They have 10% allocation to Bajaj Finance and 5% to Bajaj finserv. For 33,000 cr fund – Top 20 stocks contribute 85-90% allocation.

As you can see both the styles are exactly opposite – 1) IDFC prefers diversification, Axis prefers concentration 2) IDFC is small mid cap heavy, Axis is large cap heavey. This also shows in their fund performance. When IDFC underperformance, axis outperforms and vice a versa. This also makes my life easy as when one fund underperforming, the performance of other fund acts as a guide to decide whether this is BAU or permanent

Small Note on the side – What I also observe that, we as retail investors discuss lot about ‘’Number’’ of stocks in portfolio but fund managers decides strategy and ‘’number’’ of stocks is the by-product of the strategy. Number of stocks is not a primary strategy

Commenting on Axis underperformance

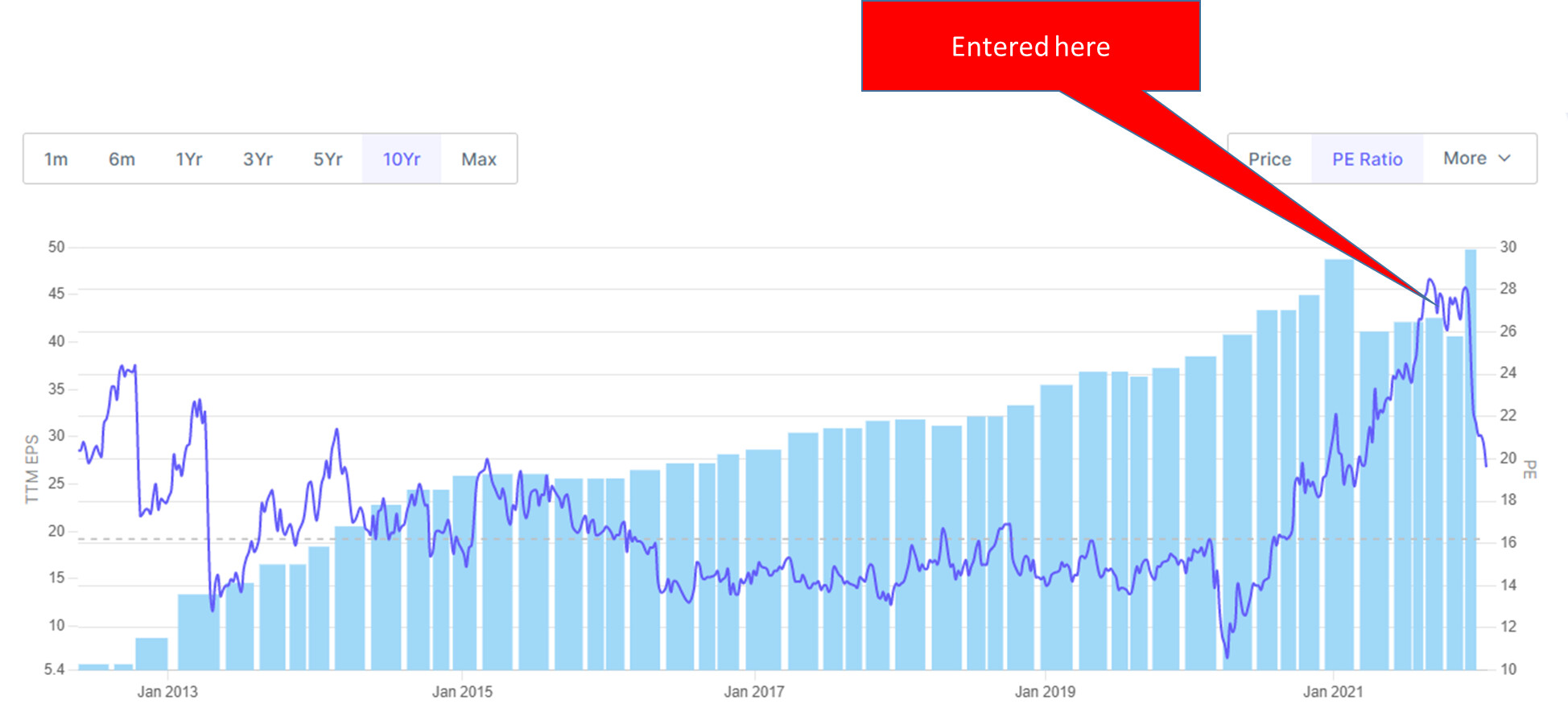

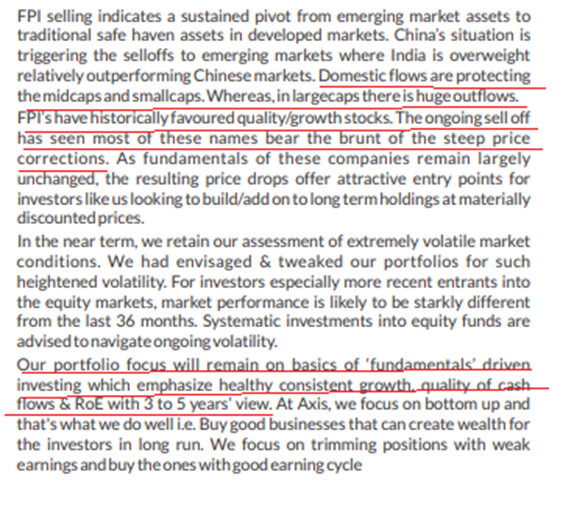

We are at very interesting juncture in the market where both the schemes – IDFC and Axis - are showing diametrically opposite performance as expected but this time IDFC is outperforming when market is in bear grip. The part of the reason can be the start of new cycle with rising interest rates which is mean reverting the valuations of ‘’Quality’’ stocks. Also Axis MF, attributes this to heavy FII selling as mentioned below in their last month’s factsheet

Overall I think, this underperformance can last for longer. My judgement is this is business as usual and long term IRR will be jump back to high teens to twenty% once the cycle turns.