This is an auto ancillary company. Established in 1983, the company specializes in sheet metal components, tubular components and machined components.

It caters primarily to 3 industries- 2 wheelers industry (Hero), railways and Commercial vehicles (Tata Motors)

It has nine Manufacturing Plants in India-Link

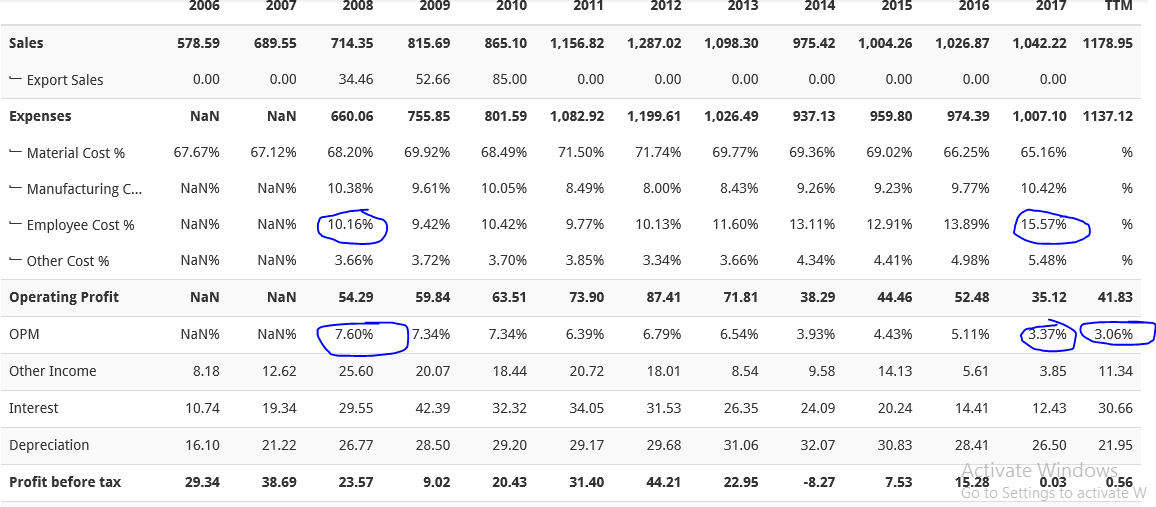

It does annual revenue of 1150-1200 crores with mkt cap of 340-360 crs.

For past few years, the company had been languishing as its revenues and margins are linked to growth in commercial vehicle, railways and 2 wheeler industry. With GST coming in, truck demand is going up as we can see in sales of Ashok leyland and Tata motors. Also, Railways is planning big capex, and had recently awarded an 800 crore order for bio-toilets in late 2017 out of which 250 crores order was won by Omax auto.

In addition, the co has done restructuring, has laid off some employees and have shut down a loss making plant. They have also indicated one time employee terminal benefit expense in the results. As a result of this exercise, the margins have improved, and last quarters gross margins were at 6-7% vs 2-5% range historically. The company also did some write offs etc in this restructuring in early 2017 and posted losses at that time.

The co didn’t pay any tax probably because it had been posting losses earlier and would have carried forward losses for the same.

Recently, co has posted update on BSE that it is doubling the railways steel capacity. Also, the company is restructuring manesar plant.

The debt equity is 0.7 and ROE is very low (less than 10% as of now). However, the promoter has indicated reduction of debt going ahead, and ROE shd improve to 12-16% as margins stabilise going ahead.

The risks are many- slow down in CV, 2 wheeler ind, inc in raw material costs etc.

One of the promoters Warun Mehta has sold some stake in open mkt recently. His Facebook profile tells that he is very young 23-24 yr kind of guy who may be doing some startups etc.

Disclosure - invested