Om Metal Pallacia Project Update:Already 80% Pallacia Project works completed before 2 months, revenue visibility approx 800 crore,I think one of the mispriced bet,Discloser :I own and added more at lower level

i)https://twitter.com/i/status/1026324728363999233

Hi Somitosh,

Did you get chance to go through the annual report ? I could not get transcript of the last concall as well. No new order announcements in the last quarters.

Rgds

Raghu

Investor presentation

Quite a good presentation after sometime…

Highlights

Strong order book pipeline

The company has been exploring bid for projects worth of USD

60 million in International markets

In India, the company on the verge of bid for orders worth of Rs

2000 crore

The company is expected to close its order book at Rs.1500-

1800 crore by FY19

Execution of the two key real estate projects; Om meadows (Kota) and

Palacia (Jaipur) are going well. In the next three years, considering that

the reality market to do considerably well, we expect about Rs 100 crore

revenue from Kota project and about Rs 400 crores from Palacia

March 2020 Result:

June 2020 Result :

Investor Update

Annual Report 2020 :

Great News for Om Metal…

[https://www.bseindia.com/xml-data/corpfiling/AttachLive/181736fd-3f6d-4ced-8832-64dd5c4ea1b0.pdf]

1 Like

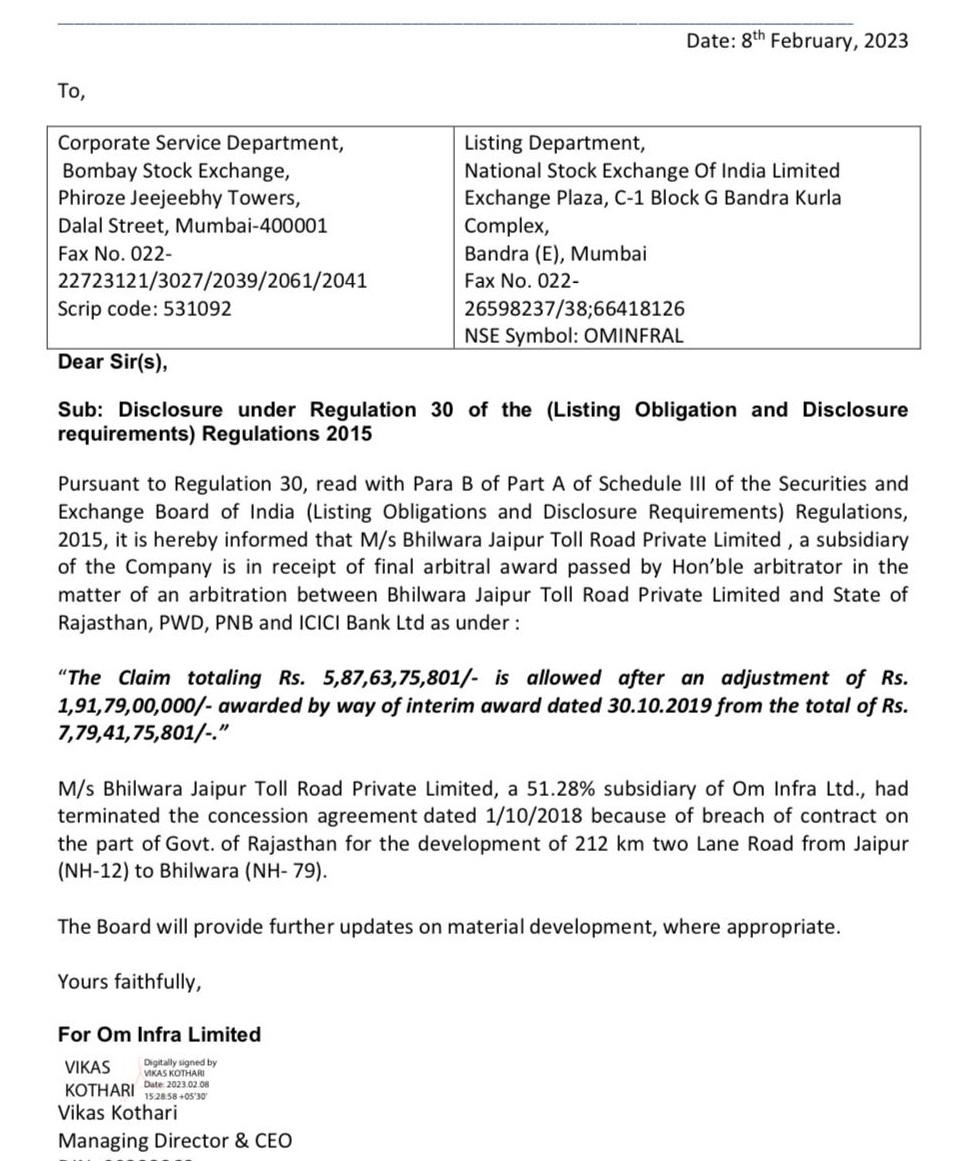

OM INFRA

*191 Cr interim relief for Road project

*PWD has taken over the Road project as per HC order

*Final arbitration award ruling expected soon

This was a major stress factor for the company from 2018 . With this new development, company will get into a new growth path now on

[https://www.bseindia.com/xml-data/corpfiling/AttachLive/1c2ab1a7-c88a-4bf0-92d2-9757e9944a78.pdf]

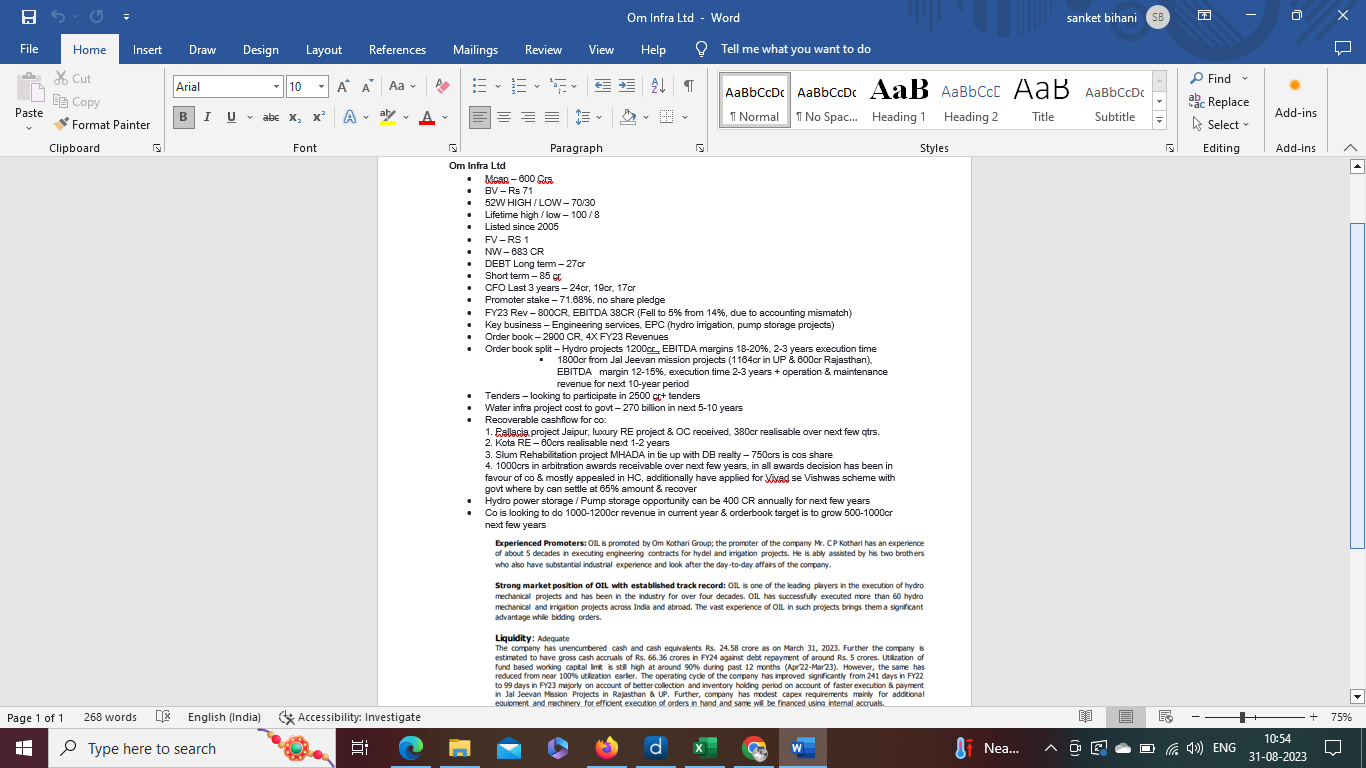

Om Infra Limited – Mcap 336 Crs – CMP 35

Om Infra Ltd is an infrastructure co. having diverse business activities and interests related to Hydro-mechanical equipment, turnkey solutions for steel fabrication, Hydropower developments, Real Estate.

Few points which makes this company interesting at this price:

o Order Book of 3350 crs Plus in Water Infra and related projects. These orders are majorly under Jal Jeevan Mission, Hydro Mechanical Projects, Irrigation Projects and Dam Water Storage Projects.

o Enormous opportunity size for Water Infra companies in Hydro Power, River Linking, Water Supply & irrigation. Jal Shakti Abhiyan and Jal Jeevan Mission are major government focus areas.

o Company recently won an arbitration award of 587 crores from Rajasthan High Court. This is won by Subsidiary Bhilwara Jaipur Toll Private Ltd. Where company owns 51% stake. Co. is likely to receive award in coming few months.

o Company won an award of 190+crs in the same case earlier.

o This arbitration award win is bigger than the current market cap of the company.

o Company’s premium real estate project in Jaipur Palacia is 50% sold and rest is selling quickly, approx. 350 crs cash flows from this should arrive in next 2 years. Real estate activity in Jaipur has improved considerably post Covid.

o Bandra MHADA Project which has been delayed for many years is likely to pick up soon as Mumbai’s Real estate market is hot. Company estimates a saleable area of 250000 sq feet which is valued at 750 crs as per company. If this materialises it will be huge for the company.

o Company has a debt of around 140 crs which is easily manageable for its size.

o In Q3FY23 company recorded its highest revenue of 209 crs where profitability was subdued due to Inflation. EBITDA was at 4.74% which is likely to see major improvement in Q4FY23.

2 Likes

My thesis around OM Infra ; Looks very promising especially if you see how market is looking at some companies in this sector like Patel Engineering:

3 Likes

Om Infra Ltd

CMP: INR 88.70 | Market Cap: INR 8,380 Mn

Financial Overview

Margins in Jaljeevan Mission range from 12-15%, while in Hydropower, it’s about 15-20%,

ensuring a stable income source. Blended margins 10-12%.

Volatility in margins attributed to global raw material price fluctuations, impacting steel and

cement costs.

Regular payments within 15-30 days under Jaljeevan Mission ensure consistent cash flow for the

company.

Business Diversification

Om Infra engages in both hydropower and dam projects, with hydromechanical equipment

supply constituting a significant part.

The company has its own in-house manufacturing facility, enhancing efficiency and control over

the supply chain.

Foraying into pump storage projects, classified as renewable energy, aligns with the

government’s focus on clean energy sources.

Real Estate Monetization

Anticipated revenue of INR 300 crores to INR 400 crores over the next 2 years from real estate

projects like Jaipur and Kota.

Margins expected to be around 10 to 15%, with minimal additional investment required.

Future cash flow may lead to an increase in dividend payouts for investors.

Limited land bank for monetization, primarily Bombay project near Leelavati hospital.

Order Book

The current order book is over INR 3,000 Crores with a mix of hydro and water projects.

Execution period is around 2-3 years and 4-5 years for hydro power projects…

The company plans to participate in upcoming tenders for hydropower and pump storage

projects.

The GoI has renewed its focus on hydropower development - new opportunities for the

company.

In the pipeline to bid for about 2 to 3 thousand crore projects.

Expectation to increase bid capacity with revenue growth.

Projects take time to materialize, up to 12-16 months from announcement to finalization.

Slowdown foreseen in states with upcoming elections, potentially delaying project finalizations.

Unpredictability in project timelines due to litigations and election-related disruptions.

Despite a substantial pipeline, the order book could be impacted by the model code of conduct

and state-level uncertainties.

Open to venture outside india, already have presence in africa

Outlook: Om Infrastructures, positioned at the nexus of hydropower, dam projects, and real

estate, paints a promising future. With the Indian government renewing its commitment to

hydropower, recognizing it as vital for meeting peak power demand, Om Infra stands to benefit

from the country’s extensive river resources. Venturing into pump storage projects aligns

seamlessly with the clean energy drive, presenting a new avenue for growth. The anticipation of

substantial revenue from real estate projects over the next two years further strengthens the

company’s financial outlook.

1 Like

Om Infra Limited Q3 & 9 MFY24 Earnings Conference Call

Revenue and Profitability

-

Om Infra Limited reported its highest-ever revenue of Rs 818 crores in the 9 months ended December 31, 2023, an 81% year-on-year increase.

-

Profitability improved with an EBITDA margin of 7.8% and a net profit margin of 5.3% for the 9-month period.

-

The engineering segment maintained robust execution, while the real estate segment witnessed a pickup in sales, leading to overall revenue growth.

Order Book and Project Potential

-

The outstanding order book remains strong at Rs 2,500 crores, providing revenue visibility for the next 2-3 years.

-

The order book is well-diversified with a mix of hydro and water projects, Jal Jeevan Mission projects, and pumped storage projects.

-

The company sees substantial potential in India’s hydro and water sector, particularly in hydropower and water supply projects.

-

Om Infra aims to secure a significant market share in hydro mechanical equipment and generate steady revenue through project operation and maintenance.

-

Growth prospects are enhanced by the emergence of pump storage projects, interlinking projects, and Jal Jeevan Mission projects.

Project Updates

NTPC Tapovan Vishnugad Hydroelectric Project

- NTPC paid 65% of the total claim amount (Rs 46 Crores) under the Vivaad Se Vishwas Scheme in December 2023.

Bhilwara Jaipur Toll Road Project

-

Arbitration award reinstated after PWD government of Rajasthan’s appeal was dismissed by the commercial court.

-

PWD government of Rajasthan has the option to appeal against the decision in the high court of Rajasthan.

MHADA Bandra Project in Mumbai

-

Arbitration award partially in favor of the consortium.

-

FSI enhancements and some reliefs granted, but additional rates applicable on BFSI enhanced FSI.

-

Operationalization of the award subject to further legal proceedings by MHADA.

-

Consortium has appealed against the arbitration award seeking additional relief.

Financial Highlights for Q3 FY24

-

Revenue growth of 24% YoY to Rs. 245 Crores in the engineering segment and 140% YoY to Rs. 27 Crores in the real estate segment.

-

Unbilled revenue considered for items with billing within 1 month after the end of the quarter.

-

Income recognized from receipt of arbitration award under Vivaad Se Vishwas Scheme.

-

Non-current liability reduced from Rs. 96 Crores in March 2021 to Rs. 62 Crores in September 2023.

Revenue and Expense Mismatch Clarification

-

Change in revenue booking policy: unbilled revenue recognized only if billing is certain within one month.

-

Rs. 25 Crores of unbilled revenue not recognized in Q3 due to uncertainty of billing in January.

-

Expenses incurred for the work related to the unbilled revenue.

Sale of Land and Advances to Subsidiaries

-

Land sold for Rs. 16 Crores in Gujarat Silo SPV, amount lying in that company.

-

Rs. 25.93 Crores advances given to subsidiaries, Rs. 16 Crores already realized and will be paid to the main company soon.

Other Income Clarification

-

Rs. 19 Crores of other income is interest income from the Vivaad Se Vishwas Scheme.

-

Main supply income from the scheme classified under main income/turnover.

Pallacia Project Sales Update

-

60% of units sold as of December 2023.

-

Out of 152 units, 3,49,000 have been sold, with 2,96,000 remaining.

-

Revenue of Rs. 300 Crores expected from remaining units.

-

Rs. 313 Crores already realized from sold units.

-

Total cash flow realization of Rs. 370 Crores expected in the next 2-3 years.

-

Realization delayed due to stamp duty issues and people waiting to register units in their names.

-

Expected revenue from Pallacia by the end of the financial year: Rs. 35-40 Crores.

Pumped Hydro Projects

-

Current project: Kundah pump storage project in Tamil Nadu worth Rs. 150 Crores.

-

Potential for adding 25,000 megawatts through pumped storage projects in India.

-

Bidding process for these projects is slow due to DPR preparation, approvals, and financial closures.

-

Some projects expected to come up for bidding in the next 6-12 months.

-

Om Infra’s share in these projects could be limited to hydro-mechanical equipment (

4 Likes

![]() Triggers:

Triggers:

- Massive tailwinds in Hydro & JJM segment.

- High Entry Barrier business

- Backward integrated (own manufacturing)

- No competition (near monopoly)

- 2 solid future growth engines getting ready (Pumped Hydro Storage & River Linking)

- Expecting Solid Q4 (FY24)

![]() Business Segments

Business Segments

![]() Major

Major

![]() Hydro & water Projects (18-20% margin with execution period of 3-4 years)

Hydro & water Projects (18-20% margin with execution period of 3-4 years)

![]() JJM Projects (12-15% margin with execution period of 2-3 years)

JJM Projects (12-15% margin with execution period of 2-3 years)

![]() Bonus

Bonus

![]() Real Estate Projects

Real Estate Projects

![]() Robust Orderbook : 2500cr (3.1x of FY23 revenue)

Robust Orderbook : 2500cr (3.1x of FY23 revenue)

![]() 40% in hydro & water segment

40% in hydro & water segment

![]() 60% in JJM segment.

60% in JJM segment.

Read Full Detailed Analysis at:https://twitter.com/Bornwinner_VJ/status/1777176874138943734

1 Like

![]() Just watched great discussion on Om Infra and the whole water space…

Just watched great discussion on Om Infra and the whole water space…![]()

https://www.youtube.com/watch?v=66KemTonUiw&t=45s

![]() Points Discussed in the video:

Points Discussed in the video:

- Promoter background & company history

- Business vertical

- Tender process

- JJM (Jal Jeevan Mission)

- Company strategy- from pure play hydromechanical to diversification in water space

- Future growth areas - PSP (pumped storage project) & River linking

- Africa presence

- Bandra landbank

- Payment structure

![]() New insight I got which was unknown to me: Coal India plans to invest for PSP using their redundant coal plants…

New insight I got which was unknown to me: Coal India plans to invest for PSP using their redundant coal plants…

3 Likes

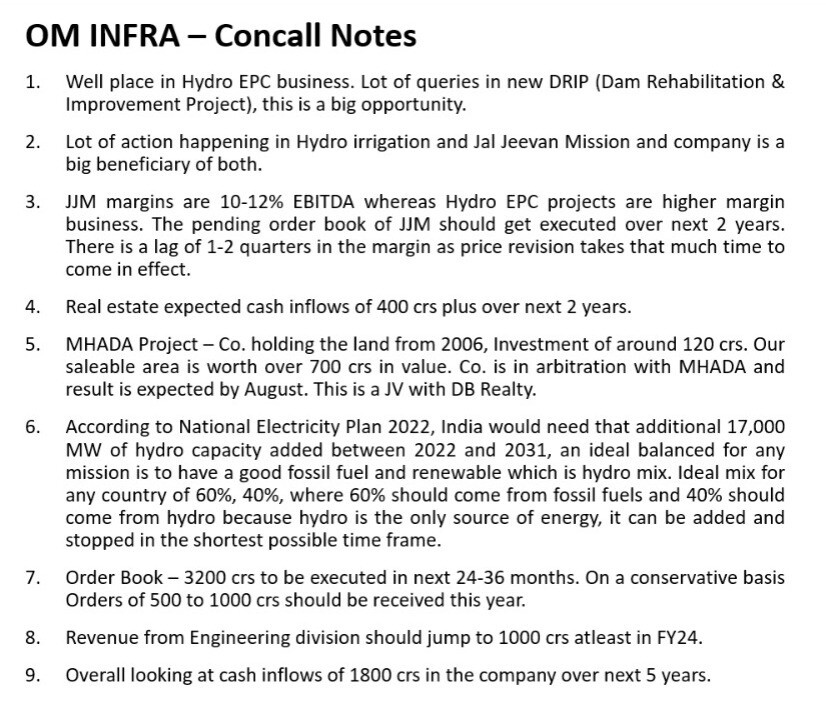

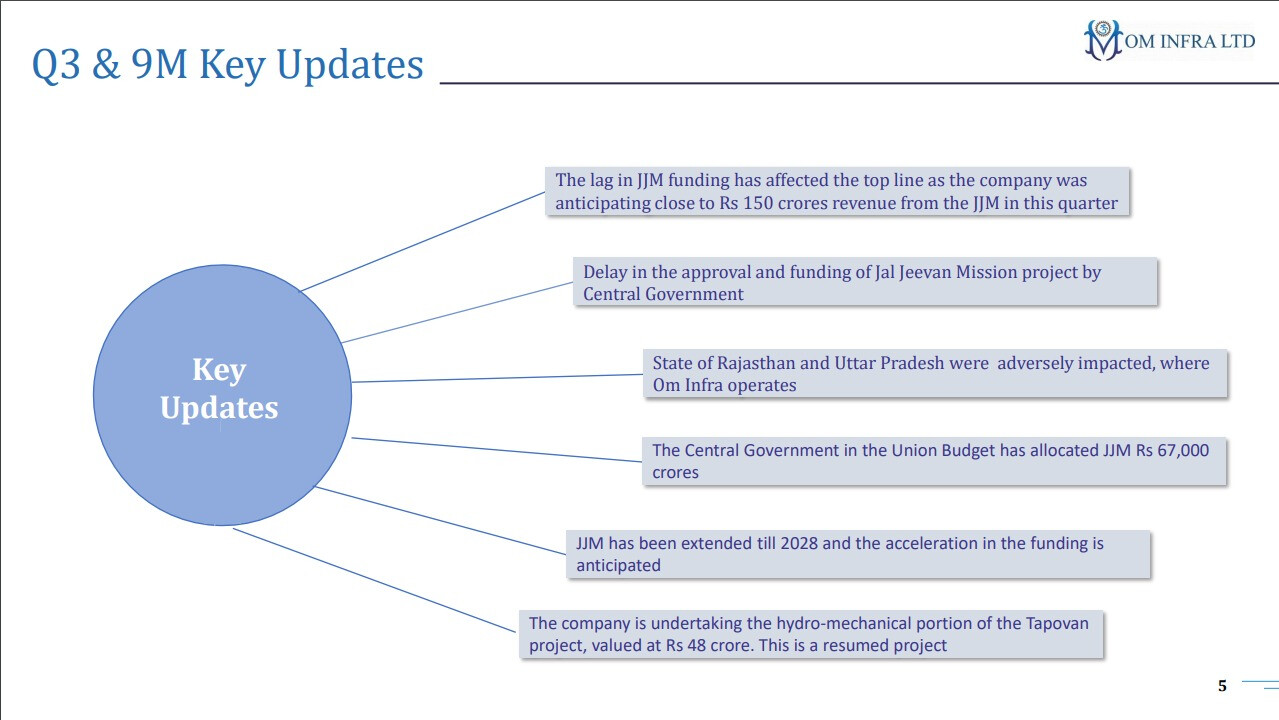

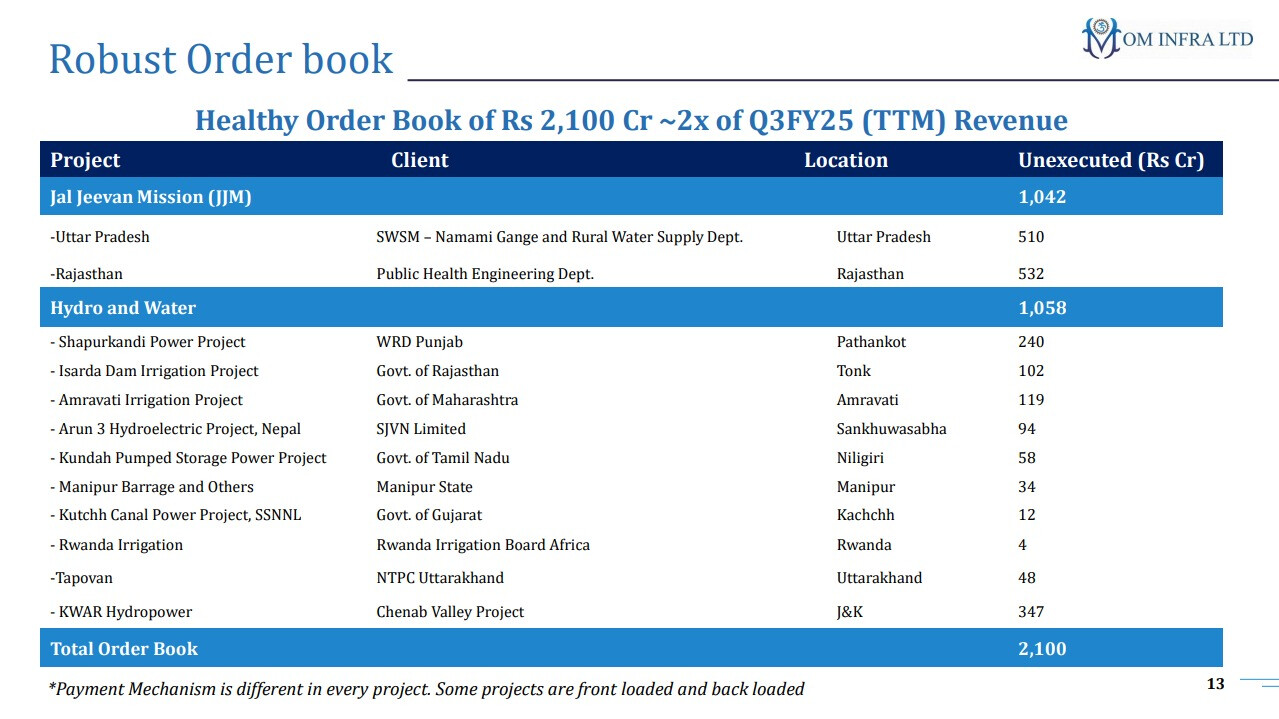

OM Infra Q3 Highlights:

- Delayed JJM funding affected revenue, with Rs 150 crore expected from JJM this quarter.

- Funding and approval delays from the Central Government, impacting operations in Rajasthan and Uttar Pradesh.

- Union Budget allocated Rs 67,000 crore for JJM, extended until 2028 with accelerated funding expected.

- OM Infra is handling the hydro-mechanical portion of the Rs 48 crore Tapovan project.

- Order Book stands at Rs 2,100 crore, approximately 2x of Q3FY25 (TTM) revenue.

2 Likes