And then only the company reacted…

And then only the company reacted…

If numbers are true the monthly issue rate is more than 10% (680,000 units lifetime sales, 80,000 pm complaints), seems pretty high. Is this normal, anyway to benchmark against competitors global or local.

It would be interesting to see if Bhavish’s behaviour on twitter will have an impact on the share price tomorrow. Every second post on my feed is yet another person calling him out.

What is the reason for this show cause notice?

Good reports, covers both negative and positive.

Disc: Baised and invested as indicated in past post.

Let me start with a disclosure: I am invested in OLA, and my views are biased, so take them with a pinch of salt. This is for educational purposes.

For investors, it’s important to see through the noise. There is a lot of noise in the market—so heavy that it seems OLA will be out of business soon. However, on the other hand, most brokerage reports are very positive.

There is a scarcity of data, and it’s difficult for investors to find reliable data. Hence, it’s important to view opinions/data holistically and read between the lines.

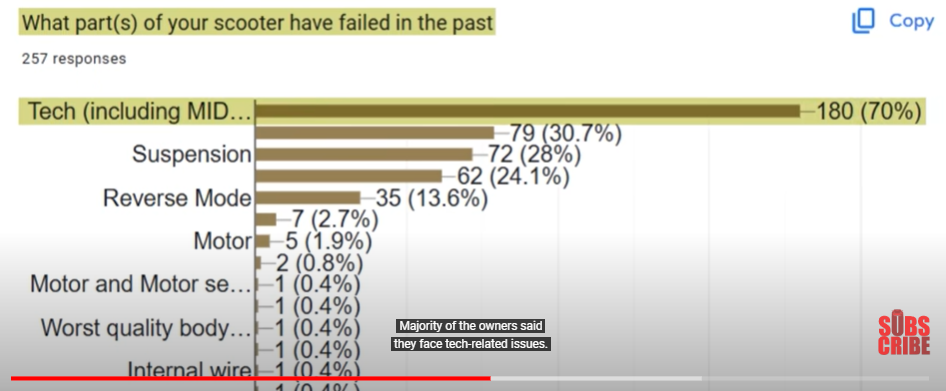

A YouTuber did a small but reliable survey. His 257 subscribers who owned OLA responded. It is reliable because he asked his subscribers to post pictures of their OLA vehicles along with their responses.

The enclosed screen is taken from the video.

According to it, 63% of complaints are tech-related. The YouTuber rightly pointed this out as well. And if you add suspension complaints (25%) and reverse mode (12%), other complaints are literally 1 or 2. Reverse mode also seems to be tech-related glitches, so you could say 75% of complaints are software-related, and the remaining 25% are suspension-related. If you look at it this way, it seems easily manageable.

The book, Innovator’s Dilemma, is a must-read. According to it, tech revolutions often start with inferior products and eventually improve in quality, replacing incumbents who ignore the tech revolution, thinking it won’t match their quality.

Disc: As indicated above.

I’d offer a different perspective.

1- EV scooters are not really a tech innovation in strict sense of the word. Plus tech on scooters, bikes, cars are nothing new. It’s a mature space and has been around for years.

2- The fact that other players (Bajaj or TVS) are not facing these complaints means that it’s a company specific issue.

3- I have heard from many investors who bought Ola stock hoping to get similar returns as in Zomato. I believe that hope is partly driven from the perception that Ola is a tech stock. But it’s a wrong perception. Ola end of the day makes scooters and their unit economics will be the same as any other 2-wheeler maker which makes me question whether premium valuation 8 x sales (even at stock price of 90) is sustainable when players like Bajaj or TVS are going at 4-5 x.

4- On purely brand level Ola still doesn’t have the same strength as a Bajaj or TVS. And since there is really no difference between product features, one needs to question why customers will pick an Ola scooter over a Bajaj or TVS unless there is a big difference in prices.

5- Speaking of #4, can Ola play a price game? This is anybody’s guess. What I think is unlike big players Ola doesn’t have deep pockets to engage in a prolonged price war and will be at the mercy of capital of their investors with an already burgeoning debt on their books. Big players on the other hand will have no problem playing a price war taking a temporary and small hit on their strong balance sheet.

A case in point here is Tesla. Company and stock did very well when it was the only player producing a high quality EV car. But as soon as new entrants came and BYD started nipping at their heels Tesla ended up losing market share and investor confidence. Stock got severely punished too.

In Ola’s case they don’t even have the luxury of Tesla to build critical mass without worrying about competitors. And steep loss in their market share since entry of big players is a worrying sign. So even if they could fix all the product issues, going for Ola will keep getting tougher.

https://www.youtube.com/watch?v=2UDUFMFqkAo

Sucheta Dalal reviews Ola in her weekly video update

Another incident/accident - 24th Oct, ola scooter catches fire in front of showroom.

Ola had an earning call today. Below is a briefing note generated using NotebookLM:

Date: 8 November 2024

Sources:

Key Highlights:

Key Quotes:

Analyst Concerns and Responses:

Disclosure: Not invested as of now, had exited earlier position almost flat. Looking to re-enter at a price which factors in all the negatives.

When asked about customer complaints and quality issues, below was the management’s response (briefed using NotebookLM again ![]() ):

):

Overall, the sources provide limited information on specific customer complaints. They do indicate that Ola experienced service capacity issues that led to a backlog of requests. However, the company addressed the backlog and stated their product quality is in line with industry standards. They highlight improvements in each generation of their scooters and anticipate further quality enhancements with Gen 3.

(NotebookLM breif ends)

I have been tracking OLA for long and wanted to buy it even at 100 but with all the negative market sentiment waiting to see how much can price go down.

Looks like the long-term story is still intact and Ola will be able to cross this rough patch. At this price point and all the negativity priced in this looks like a good time to buy.

Dic: Planning to enter soon.

OLA’s market share has been declining and TVS and Bajaj are catching up fast.

Ather has a much better product and management.

I am a close observer of the EV industry and feel that OLA is only able to sell at a discounted price.

It’s quarterly loss in around 500 crores. There was no talk to on concall that from when the company will start making profits.

No one even asked this question which was even more surprising.

Valuing a loss making business as 31000 crores with no clear path to profitability makes me very nervous.

Bajaj and TVS are catching up extremely fast.

OLA’s product and service are extremely poor, have heard that from every OLA owner I know.

At this price point Ola is still priced at 6 times sales vs 2.5xsales for hero motors and 2.5xsales for TVS both of whom are in the EV space and the latter being a strong player in ICE scooter too.

So before thinking if current price is attractive for Ola, one should ask the following:

1- Why should Ola trade at higher price multiple compared to other bigger and better players who are gaining market share at expense of Ola?

2- Are other vendors getting ICV discount or Ola is getting EV premium? Although there is nothing to suggest either, but for the sake of argument if that were the case I see better value unlocking from buying something like Hero or even TVS. If that’s not the case why would Ola not correct to Industry’s average mean multiples considering that they really don’t have any differentiators over the other player?

I cautioned people about not getting into Ola at 115 in August this year, even when it was getting upgrades from brokerages. I would still caution even when it’s corrected 50% from the top. It’s better to wait and watch and see how the company executes, even if it means giving up a few percentages points on potential up move.