Your story is fantastic but screwed up in valuation

Why don’t you do DCF?

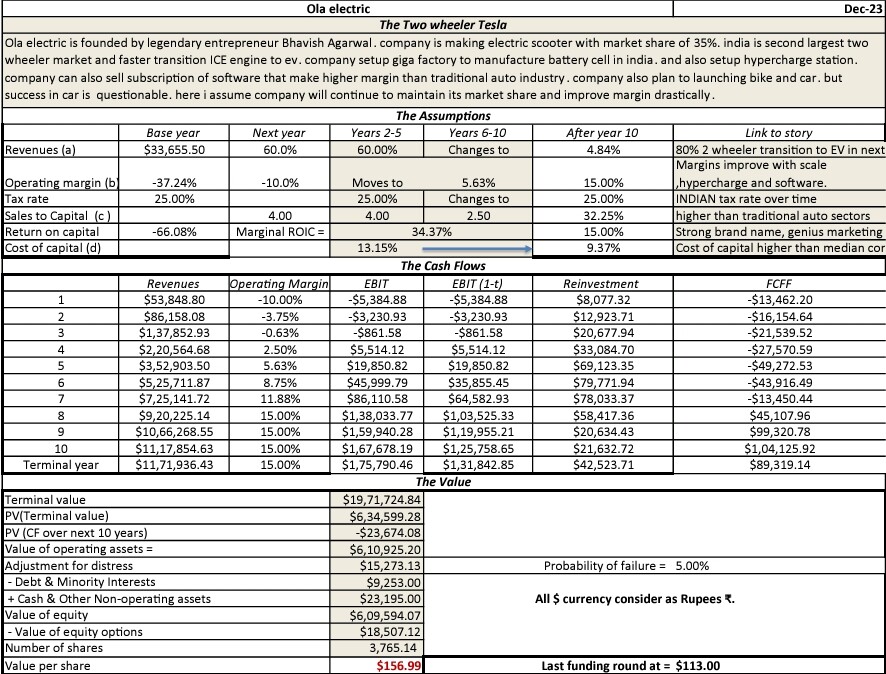

I did it before IPO.

[Ola Electric.pdf|attachment](upload://aSFTgVeKTImiYHd7QDQnF7i

5TaA.pdf) (240.8 KB)

Your story is fantastic but screwed up in valuation

Why don’t you do DCF?

I did it before IPO.

[Ola Electric.pdf|attachment](upload://aSFTgVeKTImiYHd7QDQnF7i

So you are saying 10 years from now stock should be valued at just 150?

After IPO listing, I heard on a business-news channel (CNBC I think) that there is lot of institutional buying happening even at 100/per share, and not just frenzy retail. I don’t think they would be investing in something just to get 50%, or even 100% when talking about 10 year horizon. There’s obviously something missing in your analysis, first thing it being a 10-year prediction. A lot changes in 2-3 years, that should be the horizon unless talking about a bluechip player with strong roots in it’s segment.

The truth of the matter is, the expansion capex put into Ola E has yet to show it’s true capability…

The future factory and it’s like are yet show the scalability of Ola.

Existing players might be slow to adapt, but they have scale.

And I don’t think any competitive advantage Ola has in manufacturing will stay for the long term.

Customer base of Ola are livid. I don’t see growth prospects that will make this company the next Tesla

Thanks Vivek for sharing this. Wish you may have shared earlier.

Being non-financial backgrowrd, need some time for me to study this.

I have some questions, wondering if you kind enough to answer it please.

Any website / YT to understand this excel, post if available? Thanks.

Just because china has max global share of EV 2 W, I think this is nothing to do with business strategy of indian incumbents. Infact I regret not buying into these strong and clear head businesses couple years before when they were downtrodden because of EV saga…

Now this is real scary and reason enough for me to be cautious

No, I am telling If you buy at 150 you will get CAGR return of 13.15% ( which rate I discount cash flow) every year for next 10 years.

In other words Stock will trade around 540 after 10 years.

All amount in millions.

My base year revenue 33655. Which is TTM from Dec 23. I did valuation year ago.

I can provide excel. You can update latest number and get latest value.

Ola Electric.xlsx (246.5 KB)

Latest EV sales data and market share of players:

Electric 2W sales at 88,471 units in August rise 41% YoY | Autocar Professional

Ola’s market share is down, but still at 31%. In long term, seems like a safe guess would be 20-25% market share, as other players will definitely do some catch-up.

What increases Ola’s sales is the overall expanding EV market, which is up 41% YoY for the month of August.

I find very hard to predict stock price even 6 months down the line so it’s impressive to such confident forecast of 540 (an interestingly precise reference) for 10 years down the line.

I have seen too much faith being put in DCF but methodology has been mostly rejected by highly seasoned investors including Mr Buffett.

Considering that investing in equity market is far from exact science and one has no clue about the future, all one can do is to find a fairy good company run by capable management and hope for the best. That’s how Mr Jhunjhunwala found Titan when no amount of DCF would have justified his bold call on the company.

Thx, As per my story, later part of journey, company in 2030 will be young, 10 yrs old, they will be still growing mainly international market, with this growth, I considered 40 PE. Said so this is wild estimation only.

Ola Fy 24 Revenue Approx 5000 cr and loss is 1500 cr

Aether Revenue 1800 cr and loss is 1050 cr,

motamoti…

Just for info only.

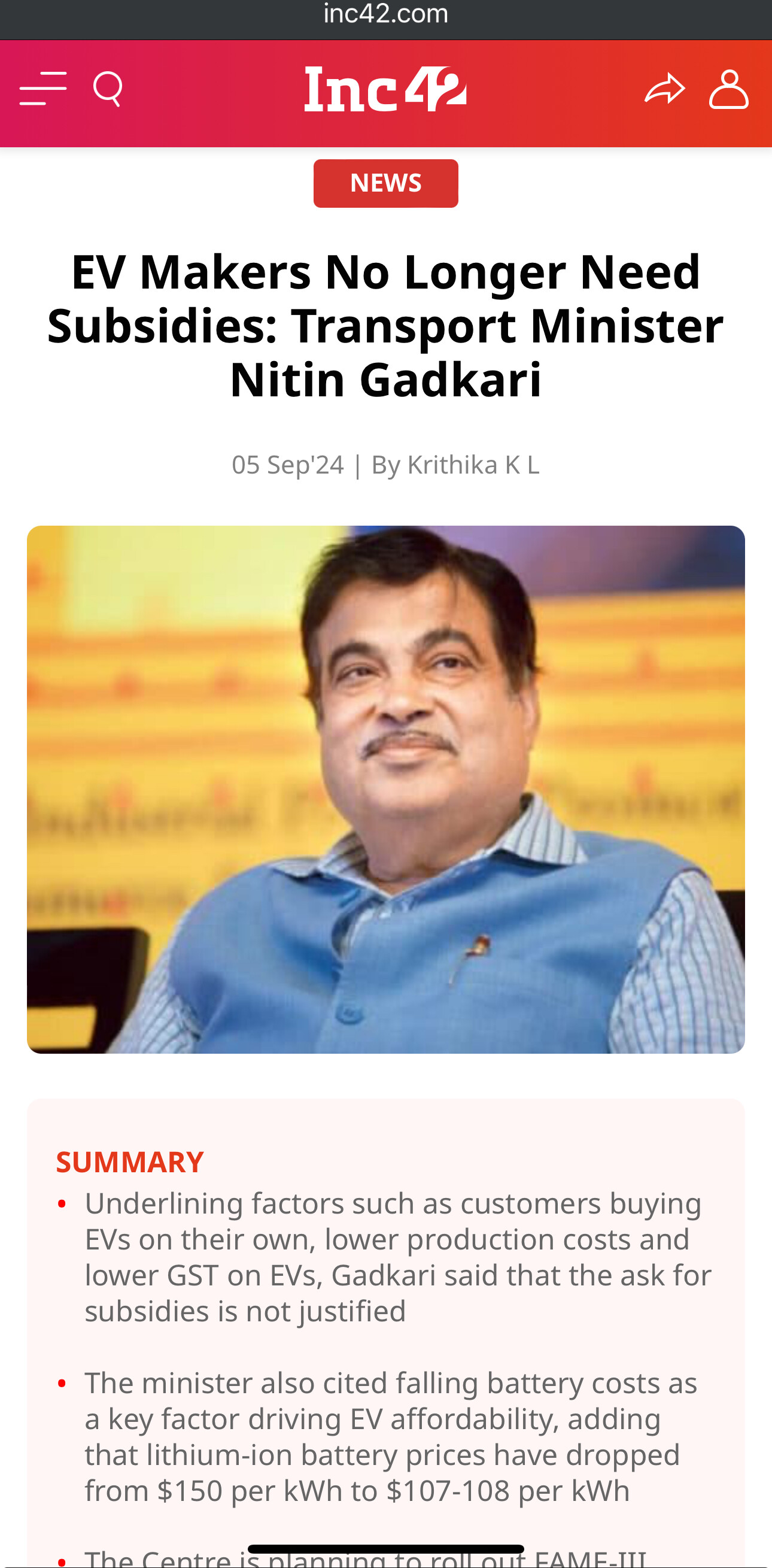

Aether is not getting the benefits of the PLI scheme whereas ola is, which again there is a chance is going to be taken away for electric vehicles as per indications given by Nitin Gadkari very recently.

Can you share some source of those ‘indications’? Two Ola models recently got certified under PLI, and there are talks of FAME-III being launched within two months.

Also, it’s yet to get any benefit of this PLI I guess, so the numbers are not including this. It’s not much difficult to guess the reason, for Ola already some ‘economies of scale’ is playing out, also that it manufactures most of the parts that go in an EV in house.

For Ather, things are not as streamlined as Ola as of now.

The founder of Aether systematically made it clear during a podcast with Nikhil Kamath that Ola gets PLI benefits for their Electric scooters whereas they don’t. Also gave the reasons/eligibility criteria for the same. Go have a look.

Nitin Gadkari is right with his arguments, but the industry body is not convinced:

And the govt seems to listen to them more than any single individual:

As for PLI, I was looking if OLA had already received some financial benefit in FY24. Not able to find anything, except about recent certification wins. The ‘PLI Benefits’, if I remember correctly, are only to be received at FY end if manufacturing/exports targets are met. So what Aether would have meant is that Ola is PLI certified and they aren’t. If that’s not the case, would appreciate if someone helps in figuring how much Ola already got under PLI.

If not, then that clears the point that Ola’s comparatively better financials are not because of PLI or any other advantage that Aether doesn’t have.

Kindly watch this video, like I was unaware that OLA had this much bad business guidance. Like they have very unrealistic guidance which led to their businesses shut down.

Goldman Sachs and Bank of America (BofA) set target prices of Rs 160 and Rs 145, respectively.

Goldman Sachs’ take: Ola can achieve earnings before interest, taxes, depreciation, and amortisation (Ebitda) breakeven in FY27, Goldman said. It expects FY24 to FY30 revenue growth of +40% compound annual growth rate (CAGR), implying FCF breakeven in FY30, and also achieving 11.9%/27% Ebitda margin/ROIC by FY30.

Numbers from GS may help in accessing valuation.

Disc: Invested and recently added, views are biased.