Dalmia Cement (Bharat) Limited (DCBL), ~85% owned by Dalmia Bharat Limited (a listed firm) and ~15% by PE fund KKR has made a disclosure to the stock exchanges on 16th Feb, 2015 regarding its intention to acquire of 26.7% equity shares of OCL India Limited (listed entity) at any time after 4 working days from the date of the notice.

As on date, DCBL already owns 48% equity shares of OCL India Limited and is classified as one of the promoters.

The acquisition of above mentioned 26.7% by DCBL is also from a promoter group headed by MH Dalmia.

Therefore the above transaction is being highlighted as inter- se transfer and the disclosure to stock exchange is an intention to seek exemption from an open offer.

Quick Facts

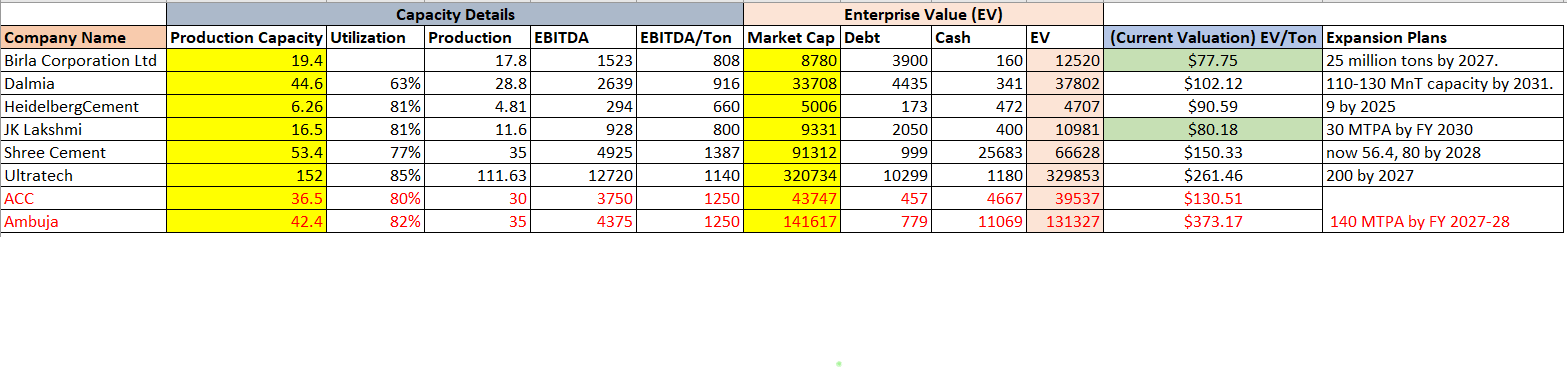

OCL has its cement manufacturing capacities in the eastern India (the region has a stable demand a supply dynamics) and has been consistently profitable. Company has recently expanded its cement capacity from 5.4 to 6.7 MTPA.

Financials a 9M FY15, Rev a Rs. 1560 Cr and PAT a Rs. 78 Cr

MCAP a Rs. ~3300 Cr, CMP 575

Company seems quite well placed and can be gauged from couple of research reports attached.

Shareholding a Promoters 74.93%, Others a 25.07%

Dalmia Bharat Limited is one of the oldest cement manufacturers in India and owns 85% in DCBL (15% by KKR), which has cement manufacturing capacities primarily in South totaling 11.5 MTPA. DCBL also owns 100% in Calcom Cement (3.1 MTPA), 76% in Adhunik Cement (1.5 MTPA) and 100% in Jaypee Bokaro (2.1 MTPA).

Total Capacity 18.2 MTPA.

With above transaction, OCL will become a subsidiary and total capacity of DCBL will swell to 24.9 MTPA.

(Some of the capacity is under expansion and is poised to complete by FY15 end)

Financials a 9M FY15, Rev a 2200 Cr and Loss a Rs. 100 Cr

MCAP a Rs. ~3900 Cr, CMP a 465

Clearly dampening immediate result and curtailed financial history in a cyclical business makes it difficult to analyse.

Special Situation + Interesting Viewpoints

W.r.t OCL Shareholders

)- The acquisition price of shares cannot exceed Rs. 725 and the minimum threshold is Rs. 580.

)- So it depends on promoters decision but what we need to arrive at - will it be at armas length / commercial nature of negotiation will prevail or not.

)- Little homework tells me that though the transaction is within promoters but there are two different families involved. So, each party will work for its best interest and the transaction price should be somewhere in between the above range. Also since DCBL is engaged wherein KKR has a 15% direct stake a I do not doubt the commercial nature of the transaction.

)- Bad point is, in most probability there would be no open offer. There can also be a chance that they might not get the exemption for open offer (although remotely).

)- Good points are, there will be strong benchmarking of the OCL share price and can be a base for any further rerating due to merger and/or delisting and/or any corporate action or even might be due to its own performance (which looks quite robust)

W.r.t Dalmia Bharat Limited

)- I believe this is where the meatier action should prevail. Company has literally graduated from a regional player to the top 5 pan-India cement player but valuation lags (both due to its performance and corporate structure)

)- Some homework tells that focus clearly is on value unlocking on the corporate side and efficiency on the operational side.

-Valuation will appear lumpy on conventional matrix, but when put in terms of capacity and prospect better sense prevail.

)- Coverage in both the counters is limited, one might expect rapid price actions once the transaction catches public glare

)- Combination of value accretion due to corporate action, performance and undervaluation seems to be at work

)- Running the company through the usual parameters, keeping the corporate action aside

- Growth a Macro driven, capacity in place,

Prospect seems good in East + Central India, neutral in South and subsidy aided in North East

-

Profitability a Volume driven, Focus on efficiency and costing, have access to captive raw materials and power (refer concall transcripts and AR)

-

Capital Mix a Heavy on Debt but no further capex, future FCFF to aid in debt reduction, OCL consolidation will give immediate boost to financials

-

Management a Decent, Established and importantly Ambitious. Adherence to corporate governace + KKR

-

Returns and Capital Intensity a No doubt itas a cyclical business, returns compressed as on date but any uptick in general trend should directly feed returns

-

Risk a Timing of upshot in general Demand, Cash flow mismatch etc.

Risks

-

Promoter does not go ahead with the corporate action (although less likely as it is being contemplated since long but no formal announcement has ever been made)

-

Donat know if any of the company is bidding in the ongoing coal auctions and any impact thereof

Refer the below link for couple of Research reports on OCL, Dalmia and notice to stock exchange which I could fish out from the internet for ready reckoner.

https://www.dropbox.com/sh/5ip8ccue8hojmg1/AAB4W4zSCq82bzVvyfupJIOFa?dl=0

https://www.dropbox.com/sh/yeq8szig0lara1m/AACjFoMt6tfbuIdvkaecIZoxa?dl=0

https://www.dropbox.com/s/mrbt1vo5z9dr8le/OCL_India_160215_SAST_by%20Dalmia%20Bharat.pdf?n=390225598

Request for other members view on the same. In my sense OCL has a good short term prospect whereas Dalmia scores on medium to short term.

Best

Mayank