About

- Established in 2017, OBSC Perfection is a manufacturer of precision engineered metal products

- Part of the machining industry, with a key focus on the auto sector

- Not a direct OEM supplier but a Tier II/III one

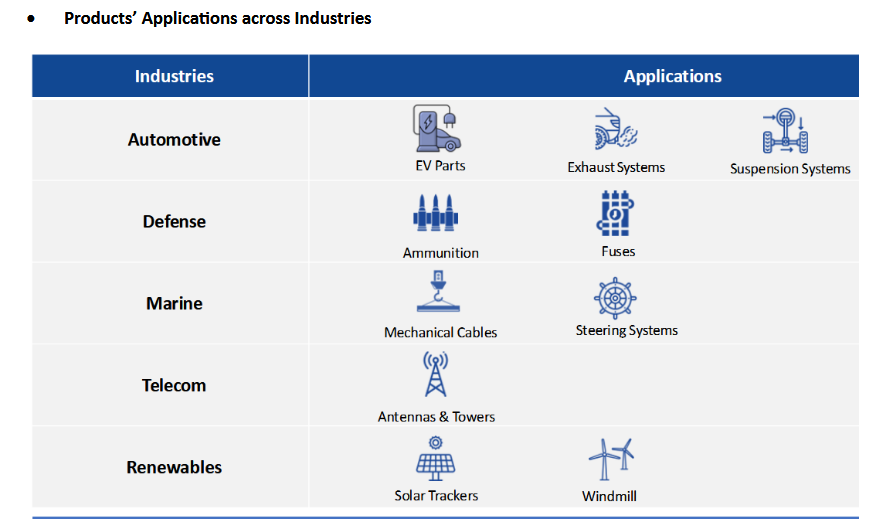

- It operates in four industries: auto (91%), defence (4%), marine (4%), telecom & renewables

- Part of the 55+ years old Anglian Omega Group which has presence in Bright Bar Steel, Electric Mobility & Auto Components Industries

Products

- Manufactures small products where Precision and quality

- Product portfolio spanning over 26 products (encompassing over 500 individual part numbers.)

- Top 3 categories by revenue:

o Sensor Boss – Precision turned parts used in exhaust systems; exported to Europe, the US,

and used by Indian truck/passenger vehicle OEMs.

o Shock Absorber Rods – OBSC is among the largest shock absorber rod manufacturers in India;

strong client base among top OEMs.

o Defense Parts – Includes ammunition and artillery fuze components, forming a growing third

category.

o The top 2 SKUs (Sensor Boss and Shock Absorber Rods) contribute approximately 40% of

OBSC’s automotive revenue.

Customers

- Top three customers as of May 2025 are: ZF Group (German €50 billion MNC), Tenneco Inc (American OEM manufacturing exhaust systems, suspension products, etc.), JTEKT (JTKT) (sparing system manufacturer)

Growth Strategy:

• Value Chain Up-Move : Addition of Hot and Cold Forging capability to move up the value chain; enabling them to make complex and larger parts

• New Industries: Strong focus on defense, marine and renewables. Under active discussions with multiple potential customers within these industries

• Exports: Increasing exports revenue exponentially; targeting to maintain 50%+ CAGR over next 3-4 years

• Advanced Machineries: Continue to invest in high-end machineries enabling to meet high level of quality to serve global MNC

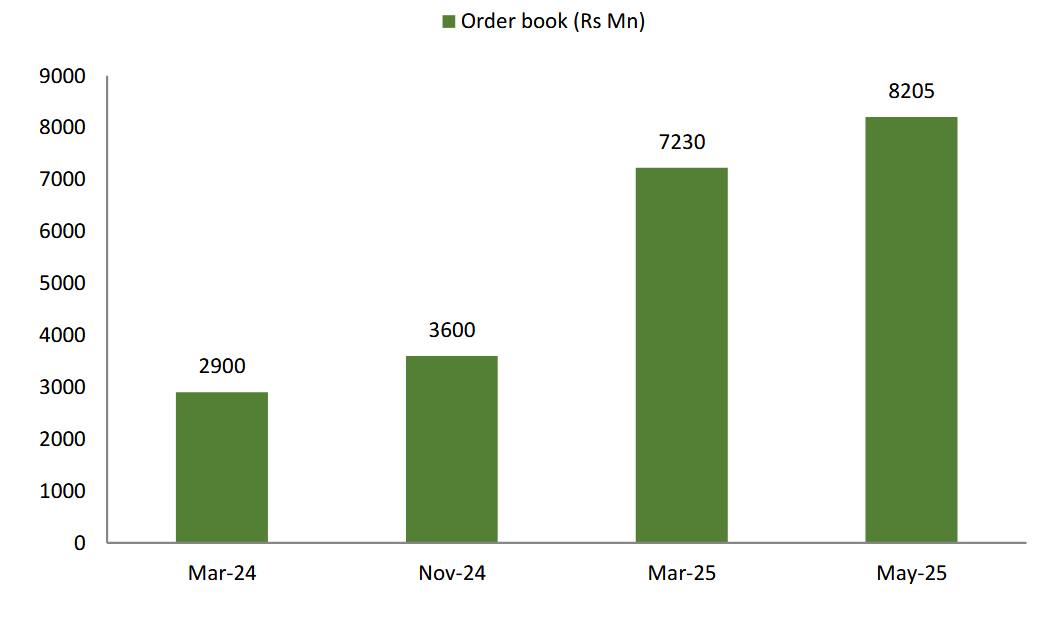

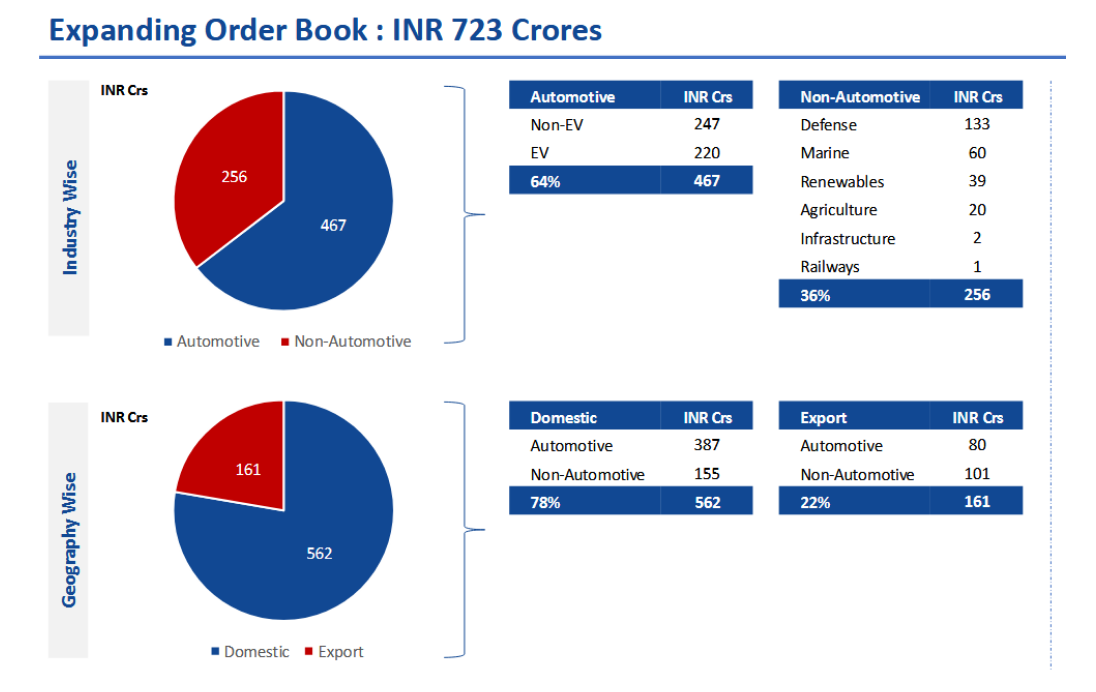

Order book

Highest ever Order wins (~4,380 mn) in a 6-months period- H2FY25

Order book more than doubled during the FY25

Execution Timeline:

- 130 crore defense order to be executed over 10 years.

- Remaining ₹690 crore to be executed over next 5 years

Industry Diversification

• Historically served Automotive Sector; rapidly expanding in Non Automotive such as Defense, Marine, Renewables sector

• Increasing order flow from non-automotive; contributing 54% of new orders received in last 6 months

• FY26 Revenue Split (Guidance):

o Automotive: ~80–85%

![]() EVs: ~25%

EVs: ~25%

![]() Non-EVs: ~60%

Non-EVs: ~60%

o Defense & Marine: ~13–14%

o Others: ~3–4%

• Shift towards non-automotive expected to accelerate over 3-5 years

• Over the next two to three years, automotive revenue is expected to be around 65%, with non-automotive contributing 35%.

• Defense and marine are foreseen to grow at a CAGR of at least 45% to 50%. This could jump much faster if pipeline discussions convert into real orders.

Automotive:

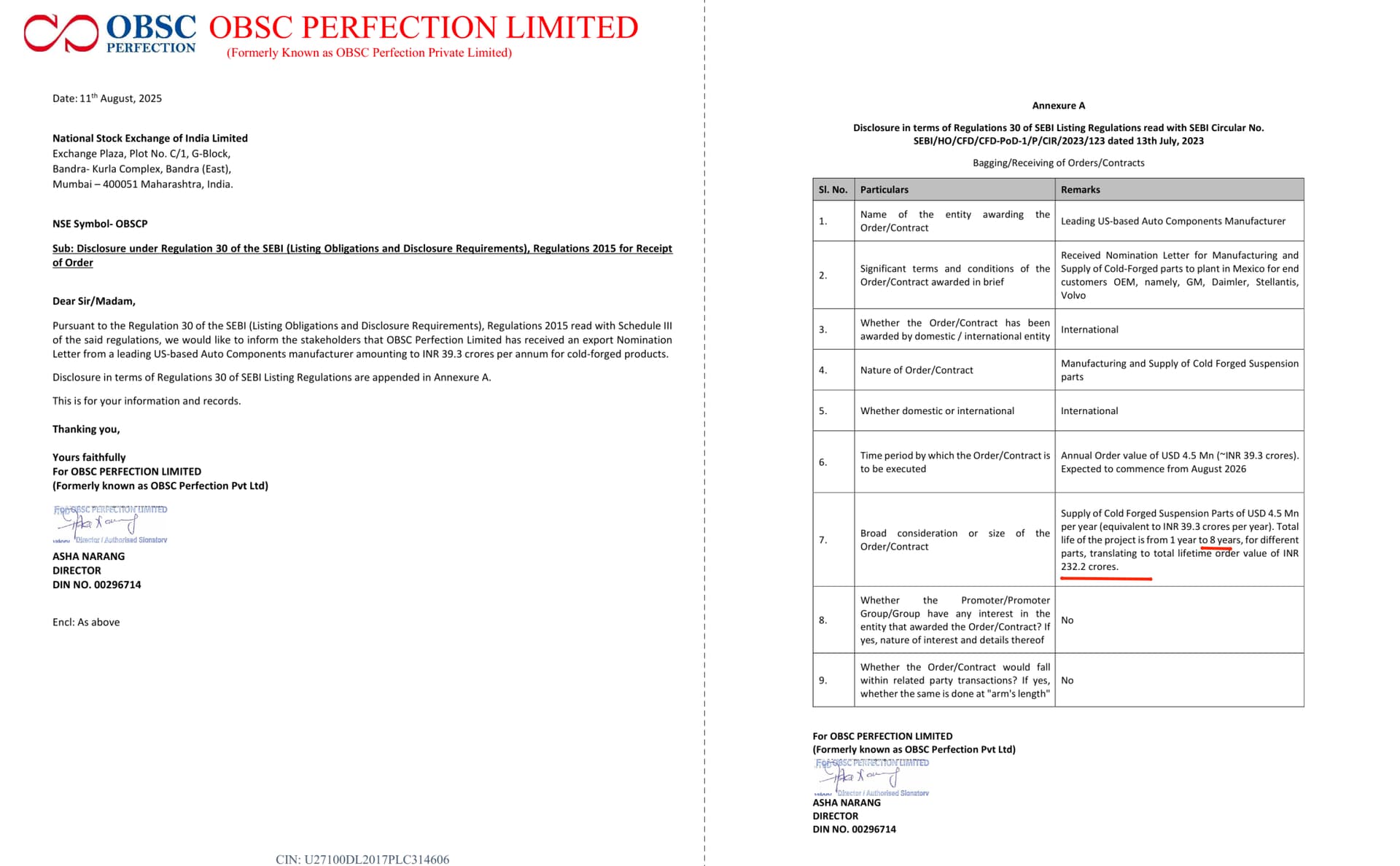

• Order Book: 467cr + 97.5 cr = 565 cr

• For a particular Tata AutoComp (TACO - a significant supplier to Tesla ), OBSC Perfection is the single source supplier from India for parts being developed for the first time in India. Tata AutoComp is expected to become one of the largest customers very soon

Marine:

• Order book: 60 cr

• Actively in talks with multiple US-based marine component manufacturers.

Marine:

• Order book: 60 cr

• Actively in talks with multiple US-based marine component manufacturers.

• These companies are looking to outsource patented production processes to India due to Tariff-driven

supply chain realignments between US and China and Need for a trustworthy and proven Indian partner

• OBSC is at an advanced negotiation and relationship-building stage with these clients

Aerospace

• For the aerospace sector, the company recently started the AS9100D certification, which is required to enter this sector

• Parts under development and validation; no confirmed orders yet, but RFQs received and expressions of interest are high.

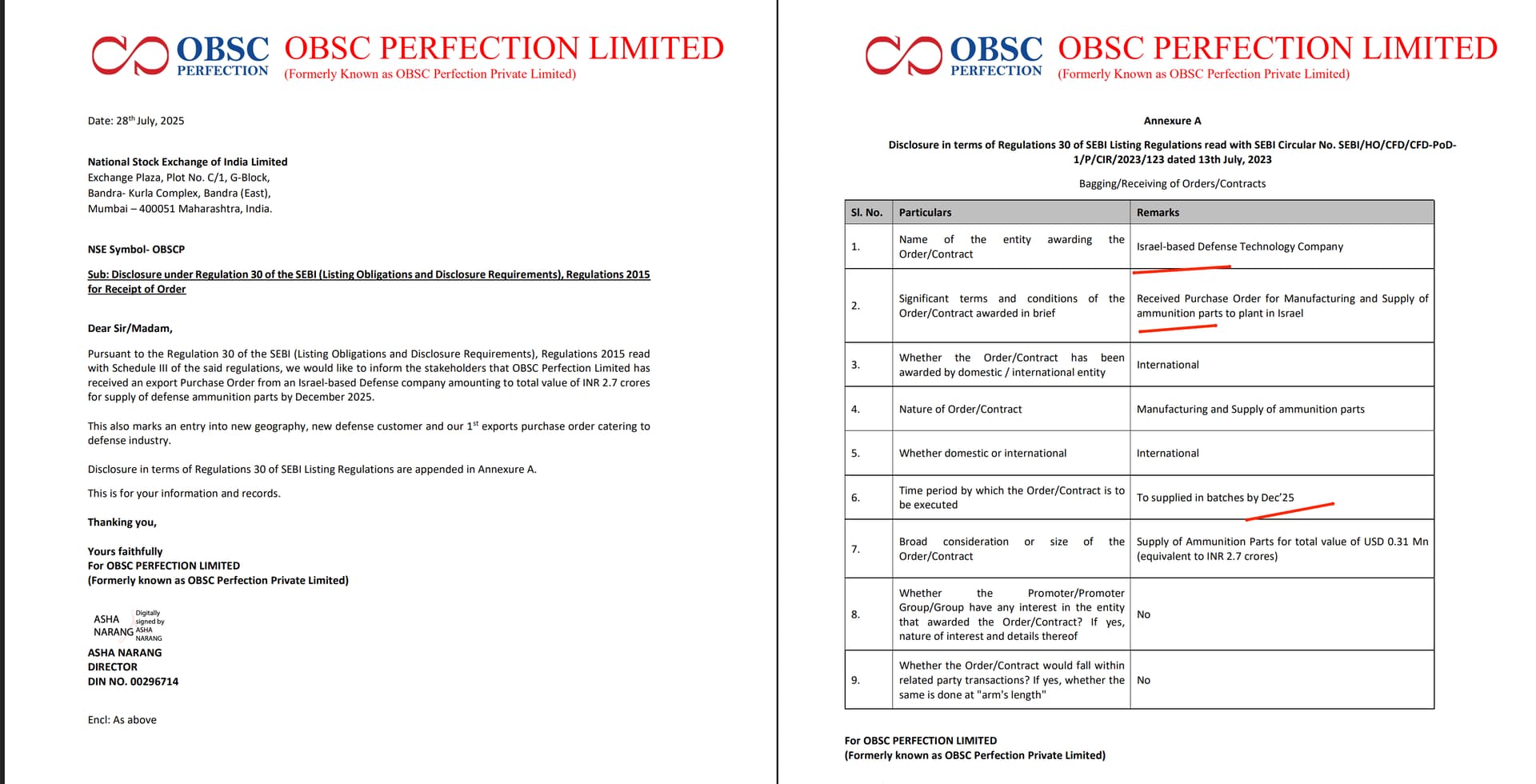

Defense

• Order book: 133 cr

• They are manufacturing some Defence products for PSUs in India and some are of Israeli origins

• Revenue from defense segment up from ₹0.28 crore in FY24 to ₹5.55 crore in FY25

• Defense order book: ₹130 crores (10-year horizon). Implies ~₹13 crores/year revenue visibility from defense

• The Defence segment is expected to grow significantly, potentially at a CAGR of at least 45%-50%

• Defense segment to drive margin expansion and profitability

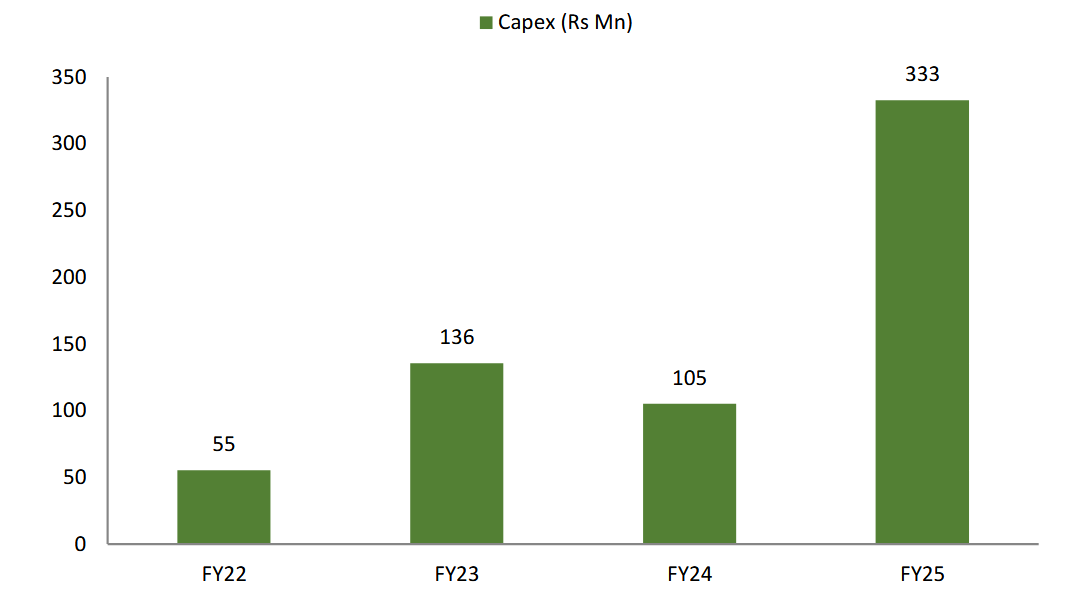

Capacity / Capex:

• It has five plants, four in Pune and one in Chennai. A plant is coming up in Gujarat.

• In-house manufacturing capabilities across machining, turning, investment casting, fabrication

• OBSC identifies itself as a precision engineering company. Now within that broad spectrum of precision engineering, they have different processes like CNC machining (which includes Swiss machining, grinding), Investment casting, Cold & Hot Forging

• ₹20 crores of unutilized IPO funds remain: ₹15 crores earmarked for CAPEX in third facility (Chennai) & ₹5 crores for Unit -4 in Pune. Utilization timeline: Majority in H1 FY26, balance in H2 FY26.

• 3 out of 5 plants operating at 80-90% machine utilization

• The Chennai plant (third facility) and the Pune plant (fourth facility) are yet to come to full capacity.

• There is space to add new machines, and teams are ready for expansion. Future growth will see massive revenue coming from these plants.

• Value Chain Up-move with Forging Capability:

o Addition of Hot and Cold Forging capability to move up the value chain; enabling them to

make complex and larger parts

o 5th Facility being commenced in Pune – this plant will bring our in-house forging capability

o Status:

![]() Facility inaugurated in Apr’25

Facility inaugurated in Apr’25

![]() Hot and Cold Forging press machines have been ordered

Hot and Cold Forging press machines have been ordered

![]() Expect to be operational in 3 months – Mid August 2025

Expect to be operational in 3 months – Mid August 2025

![]() Eventually, this facility will have both Machining & Forging under a single roof

Eventually, this facility will have both Machining & Forging under a single roof

![]() Expected to convert into revenue from the end of the second half of FY26

Expected to convert into revenue from the end of the second half of FY26

• A dedicated facility in Sanand, Gujarat is being planned for a long-standing customer to produce shock absorber rods for commercial vehicles and electric vehicles. A confirmed letter of intent has been received, and the project will be worked on over the next six months. This planned Gujarat facility is not included in the current Rs. 700+ crores order book.

• The company plans to get into stamping and sub-assemblies very soon. The goal is to become a company that owns multiple processes and can make any metal part in the long-term

Outlook

• The management expects margin tailwinds from growth in the ASP and change in the export mix. It is targeting a margin expansion of more than 400bp in the medium term

• Focus is on higher profitable sectors of defence & increase in export mix (defence/exports:

~INR133cr/~INR181cr)

• In terms of capacity, with the current installed capacity, the company expects revenue to grow to around Rs. 200+ crores in FY26

• Company expects >40% revenue growth in FY26

• The company expects margin expansion. Immediate target is to improve EBITDA margins by at least 200 basis points for FY26