**Disclaimer- Have a tracking position, consider me biased but most importantly- dumb.

Background-

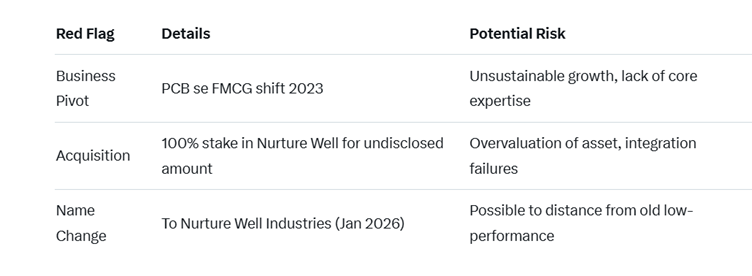

- Established in 1995, the company, as the past name suggests was in PCB busi

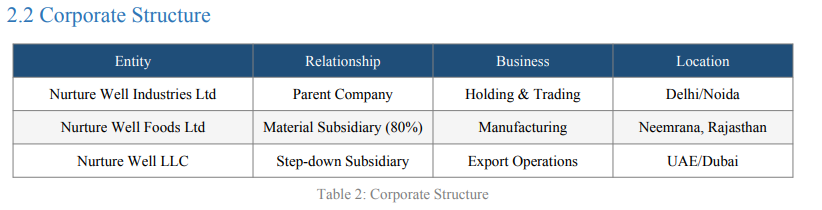

- With the acquisition of “Nurture Well” in 2023, the company started its venture into biscuits and other FMCG products.

- In July 2024, Nurture Well Foods Limited ceased to be a wholly-owned subsidiary when India Inflection Opportunity Funds acquired a 20% stake through preferential allotment

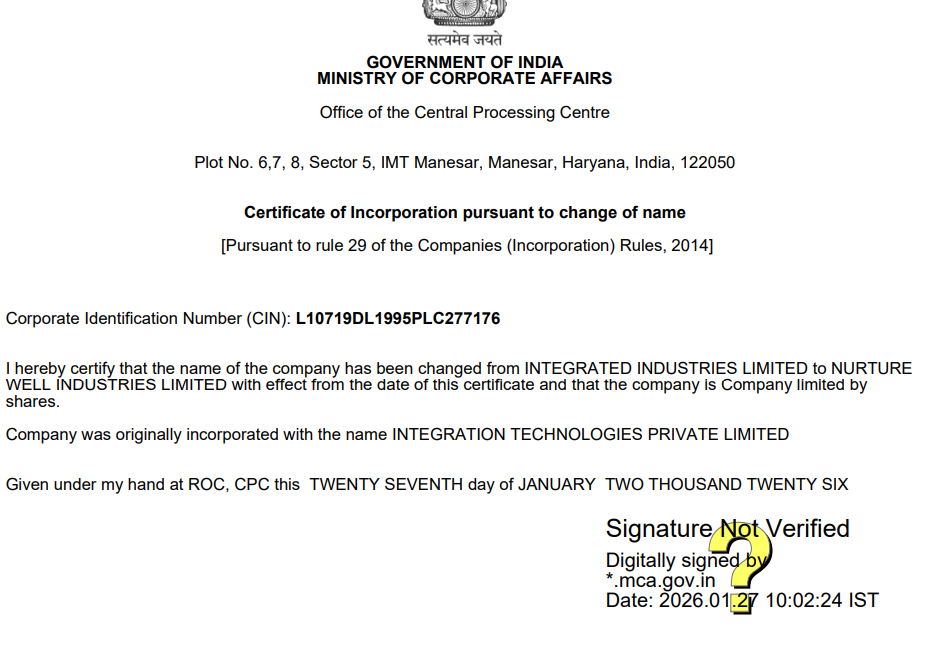

- The company has recently changed its name from Integrated Industries Ltd to Nurture Well Industries Ltd.

Industry background, TAM-

-

The global biscuits market was $134.1 billion in 2025 and is projected to grow at a CAGR of 4.0% to reach $191.4 billion by 2034.

-

India is world’s largest exporter of biscuits. Indian biscuits market was valued at $5.05 billion in 2024 and is expected to reach USD 8.72 billion by 2030, growing at a CAGR of 9.61%.

-

Obviously, India’s growth is more than global average because of This growth is significantly higher than the global average, reflecting the country’s demographic dividend, increasing urbanization, and rising per capita consumption.

-

India’s per capita biscuit consumption stands at approximately 2.5-2.6 kg per year much below global average of 4.5-5 kg.

How it came to the tracking list?

-

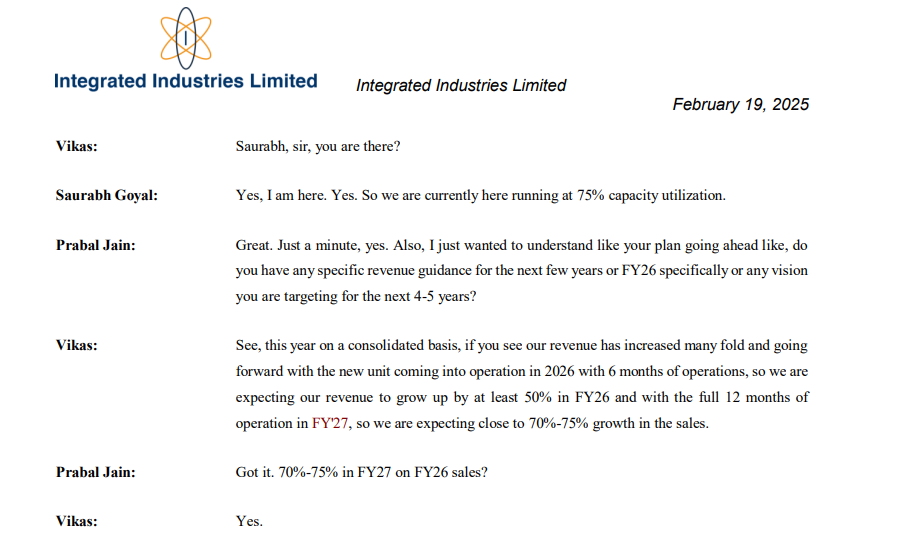

The co. did its 1st con-call in 22 Feb 2025 where it guided 50% growth for FY26 and 70-75% for FY27.

Business Model and how the company operates-

-

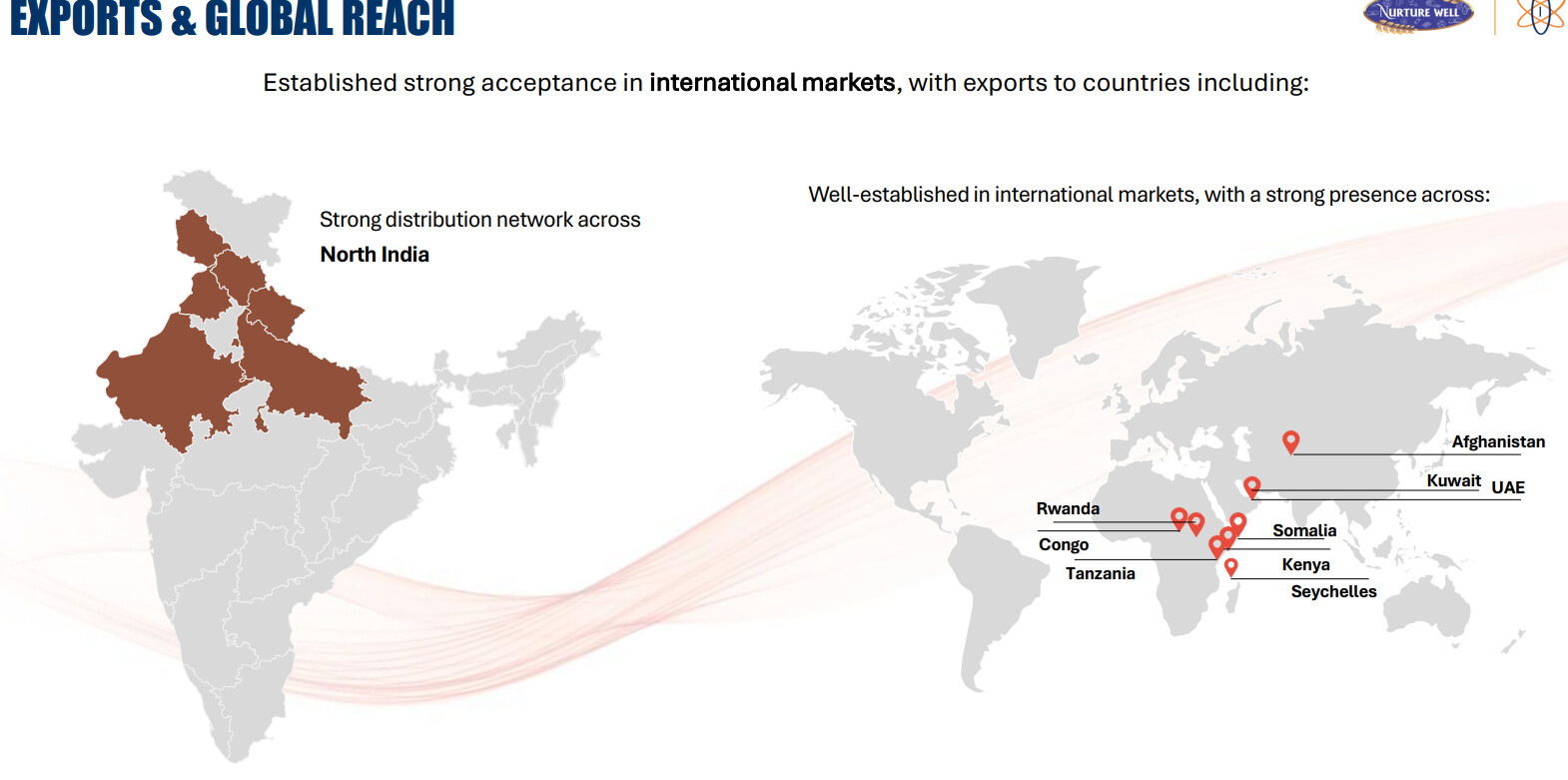

The company started with selling biscuits in Africa and Middle-east by getting them contact manufactured and putting their brand to it.

-

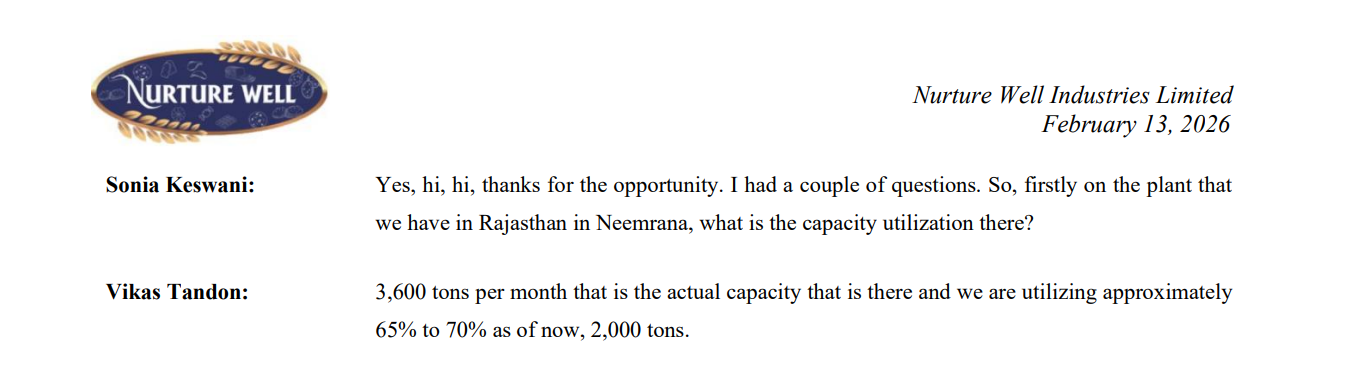

By acquiring Nurture well, the got their plant of 3400 MT per month capacity in Neemrana, Rajasthan.

-

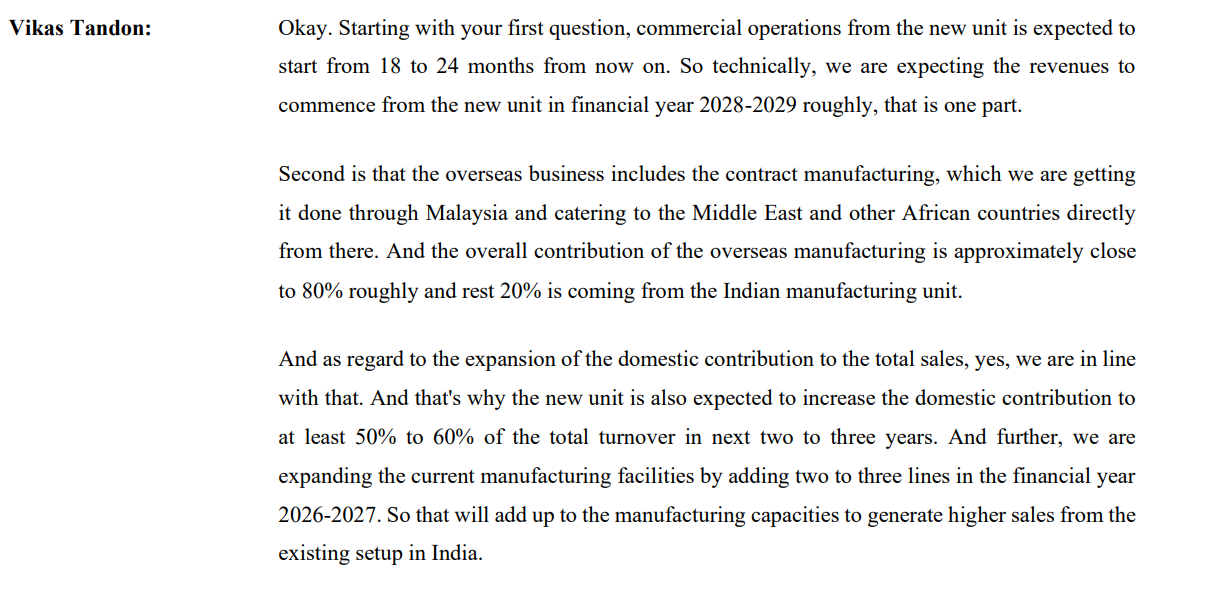

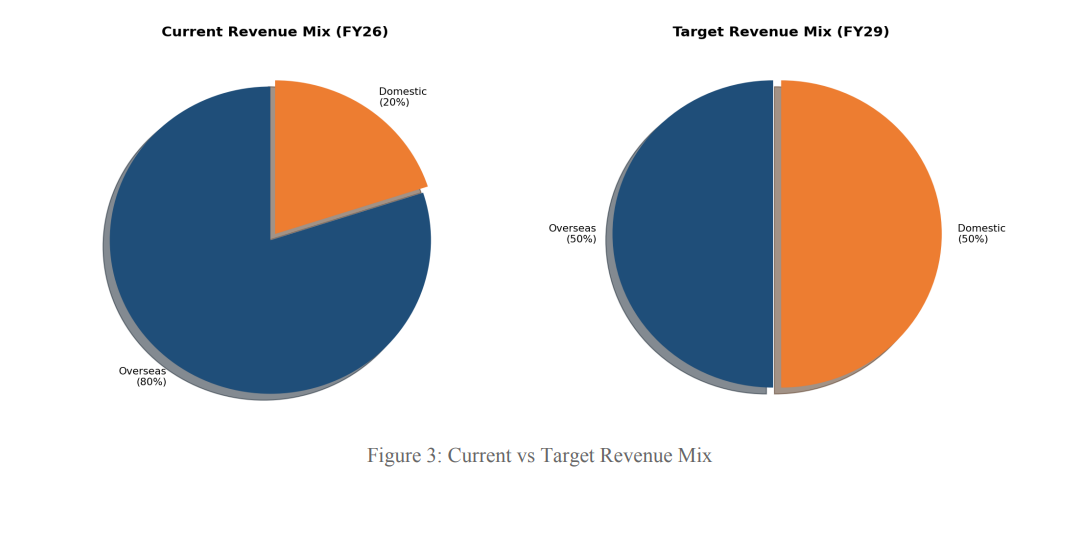

So broadly speaking, the business can be divided into 2 parts- the Indian manufacturing which gives 20% to the revenue and the overseas export contributing 80% to the revenue.

Export business- contract manufacturing of biscuits and bakery products through third-party manufacturers in Malaysia, which are then exported to African and Middle Eastern countries under the company’s own brands. The export business benefits from a tax-efficient structure through the UAE subsidiary, resulting in lower effective tax rates.

Indian manufacturing business- manufacturing a range of biscuits, cookies, and bakery products targeting Tier-2 and Tier-3 cities in North India.

Q3 FY26 results and con-call snippets-

-

The co. came out with a good set in Q3 with 46% top-line & 85% bottom-line growth and EBIDTA margin of 11.45%.

-

They also have introduced donuts, rusk, khari biscuits and also entered into fresh bakery segment.

-

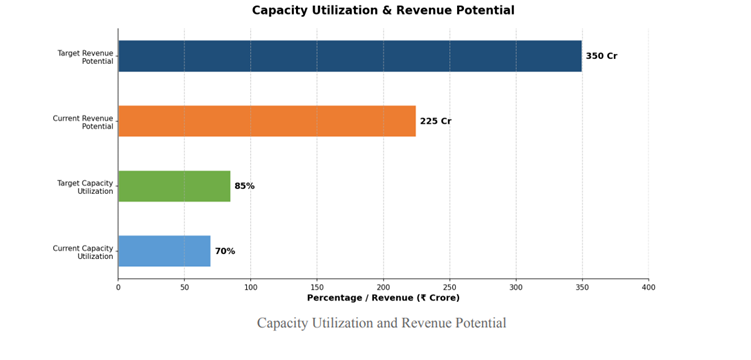

Capacity utilization stands at 65-70% as of Q3.

-

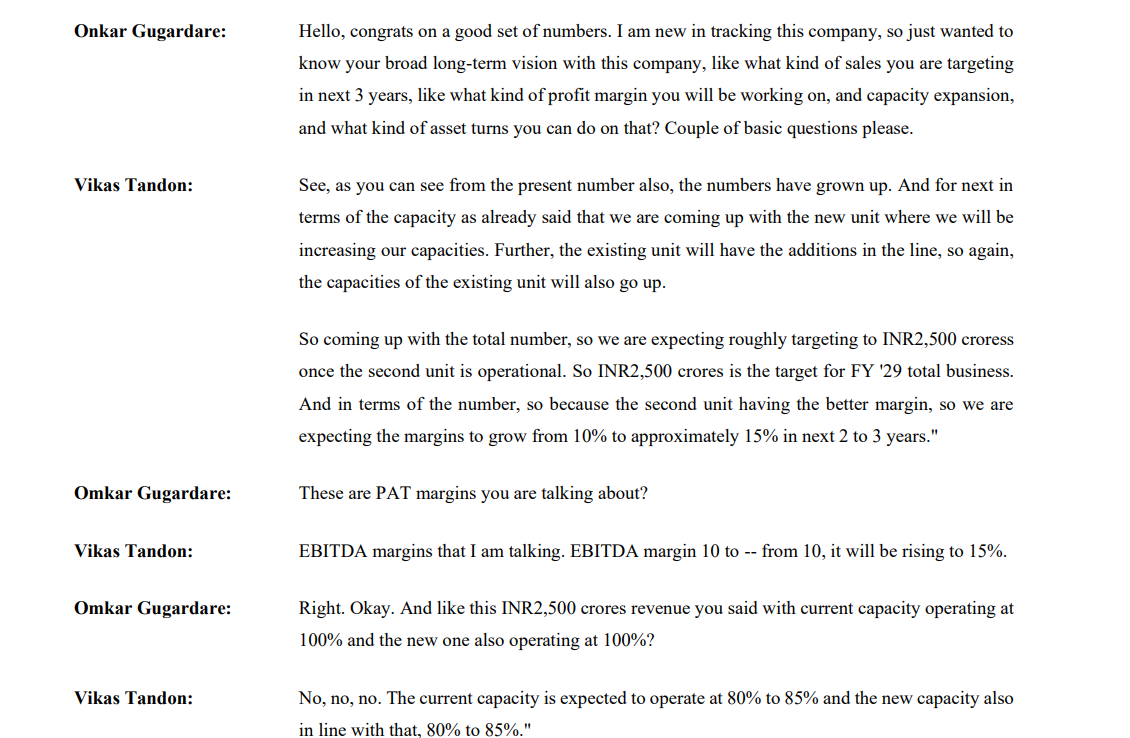

The company is planning to start a new manufacturing plant in UP which would be operational by FY29.

-

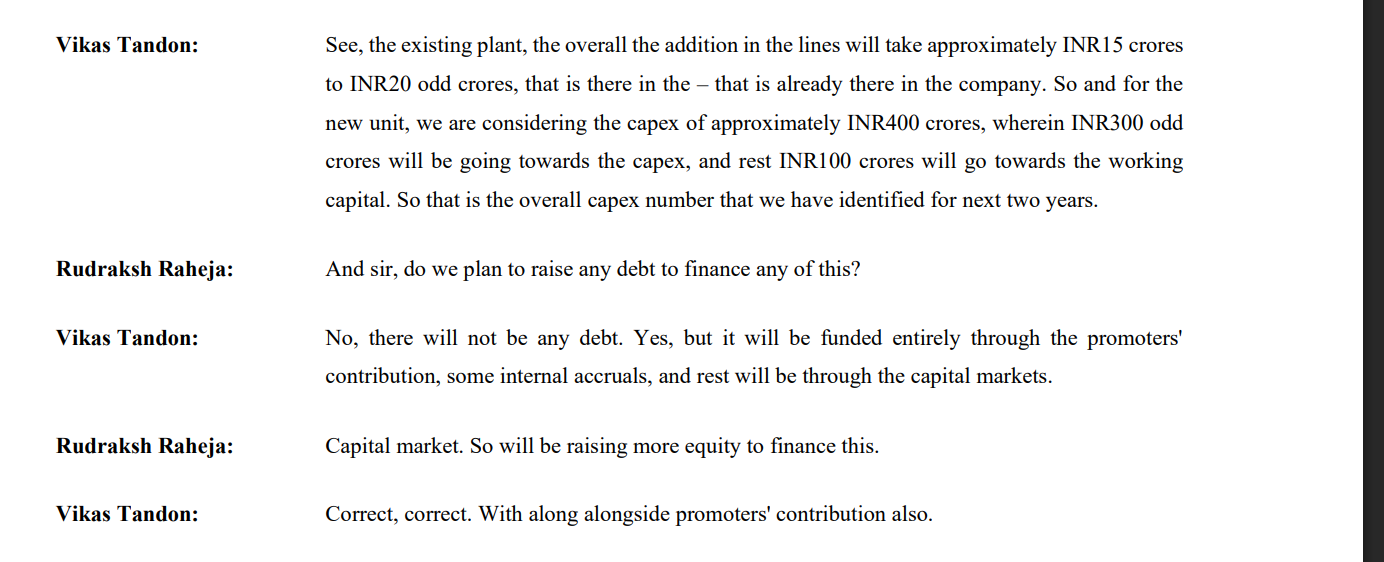

Also, the co. is planning to add new lines in the current Rajasthan facility which would take the capacity from 200-225 cr revenue potential to 300-350 cr revenue potential.

-

The capex will be done by internal accrual as well as a preferential allotment.

Mission 2029-

-

With the new capacity coming live in a few months, the management is guiding for 2500 cr revenue & 15% EBIDTA margin as 50% of the revenue will come from India manufacturing.

-

Own manufacturing will lead to higher EBIDTA margin and also 30% from the new plant is to be exported which will be margin lucrative.

Management-

- The co. is headed by Mr. Saurabh Goyal & Mr. Sanidhya Garg, who are fairly young to the business.

https://www.linkedin.com/in/saurabh-goyal-31639a71/

https://www.linkedin.com/in/sanidhya-garg-382aa9217/

-

They were also asked about the management during the con-call.

-

Someone on X also have shared their founding, which can be of concern if true.

https://x.com/ZenvestorFiles/status/1901324043607036324

Growth drivers-

The co. has themselves mentioned the drivers in Q3 results ppt and one need not dig any deeper.

Some concerns/ Probable red flags/ Trackables-

-

Grok helped with this one.

-

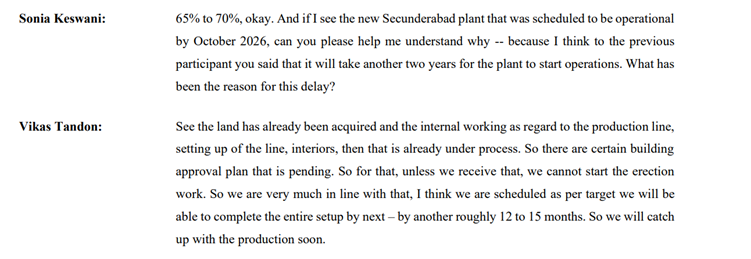

The UP plant was to go live originally in Sept 2026. The management was asked about the same & this was their answer.

-

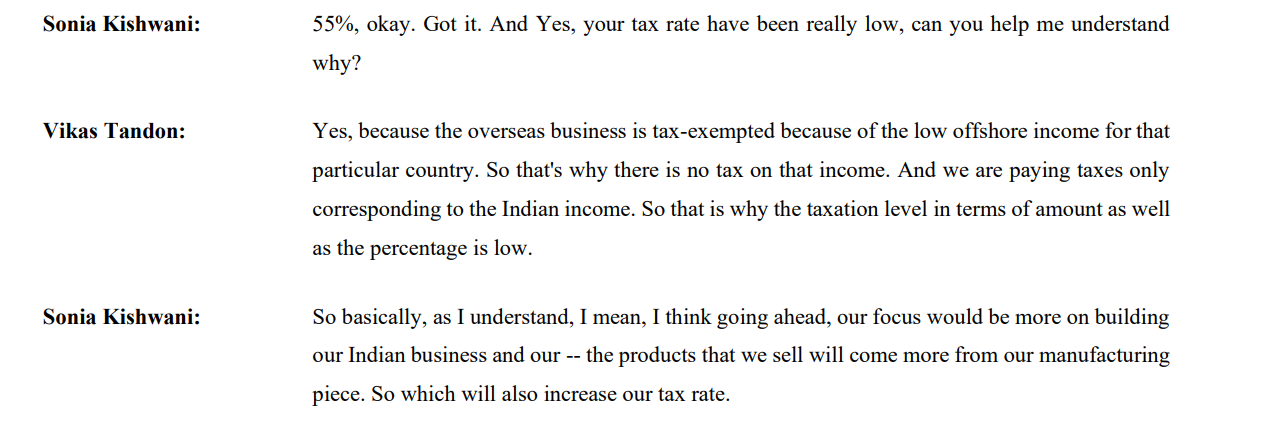

The tax rate seems to be really low which is because 80% revenue comes from overseas business where tax rate is lower.

-

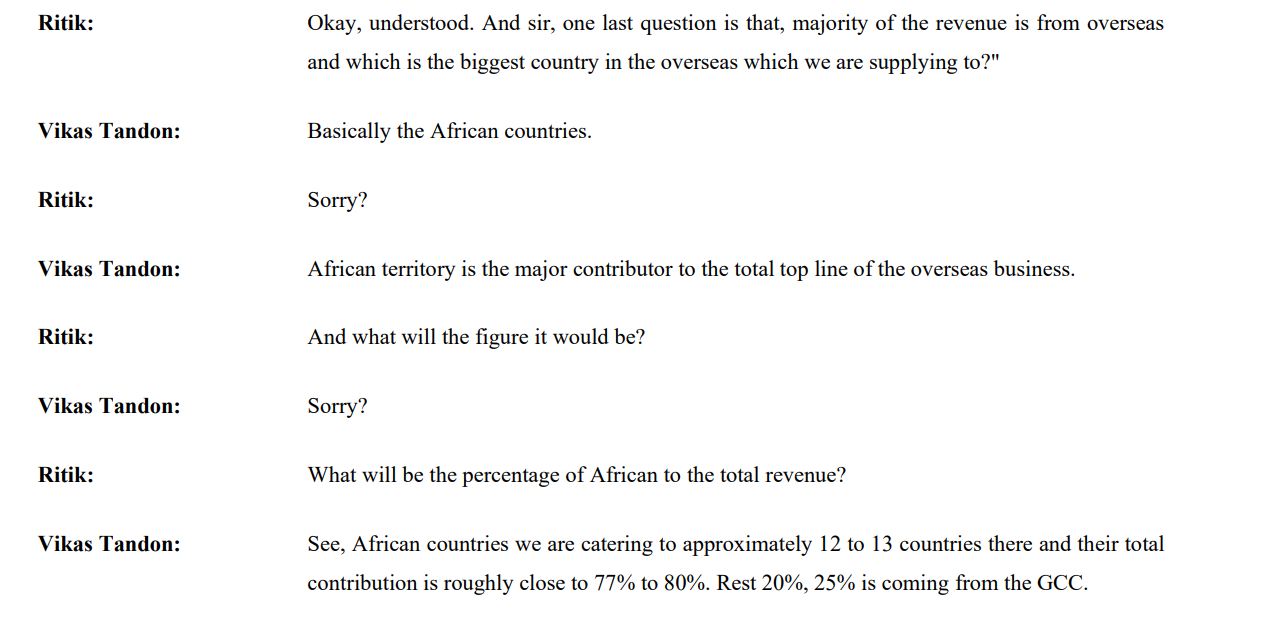

75-80% of the overseas revenue comes from Africa, which is not a big turn on for me. (Consider me biased here)

-

There is a customer concentration risk as 75% of the revenue of FY25 comes from a single customer. The justification seems somewhat reasonable though.

-

After the H1, the receivables were quite high at 216 cr for a 537 cr sales. The management claims to have received 57cr as of the Q3 con-call.

-

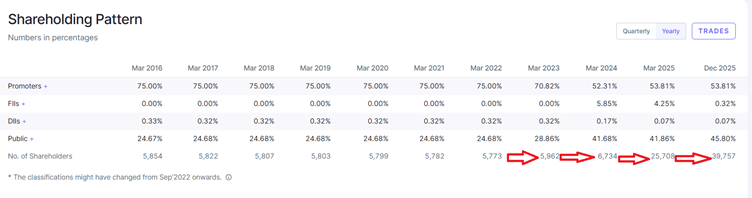

Have to track the retail investors and the rise is certainly not good.

Valuations- The co. is available at a single digit PE considering their guidance which seems achievable so far and the management has walked the talk in this regard.

However, allocation in the portfolio is the key considering some concerns and if you find the justification/answers satisfying and just a reminder- “we are in the game of stocks rejection not selection”.

Summary:

-

The co. is headed by 2 young leaders which started its FMCG business from 2023 and also changed name in Jan 2026.

-

The co. gave a very optimistic guidance for 2026 and is on the path to over shoot it.

-

The co. is constantly coming out with new products and intending to increase its sales & Tam with the upcoming capex.

-

The key trackables would include

- Delivery vis-à-vis the guidance

- How the co. handles the commodity price volatility (flour, palm oil, sugar) and weather it can pass higher raw material price as and when it happens

- New capex coming live

- Change in revenue mix and EBIDTA margin

- Tax rate as India sales starts contributing more

- The receivables after H1 and weather it comes to cashflow.

- The FY2029 guidance of 2500 cr revenue with 15% EBIDTA margin

- Increase in retail holding

- Although there are some red flags, the valuations seem very cheap to ignore it.

** DYOR, too dumb to give any investment advice

** Took quite a while to do the research, so feedbacks and pointers to improve is always welcome.

Feel free to add anything extra you know and correct me.