Hi Dinesh

Can you please tell first step in dcf valuation…I started learning…I am novice…need to understand step by step…

First step please advise…once I am comfortable with step 1 will go to step…

Please help me

Hi Dinesh

Can you please tell first step in dcf valuation…I started learning…I am novice…need to understand step by step…

First step please advise…once I am comfortable with step 1 will go to step…

Please help me

“The Dhandho Investor” by Mohnish Pabrai contains some simplistic explanations on how a DCF is done, in case you’d like to check that out.

I would also suggest the following course: https://www.asimplemodel.com/model/3/discounted-cash-flow-model/

ASimpleModel is an amazing tool/website to learn financial modelling. It has courses and tools to learn financial modelling step-by-step. In fact, it’s being used by several famous MBA institutions around the world (Harvard, Wharton, Berkeley to name a few). Their annual subscription charges are around $2.75 i.e. ~Rs. 2400 pa or ~Rs. 200 pm, which I think is a low price to pay for such a resourceful website.

Great site just bookmarked

Thanks

Thanks Dinesh ,

I am on learning curve, I have some query what I found in number section is very fine and I am sharing with fellow VP’s to understand it better

2 Query

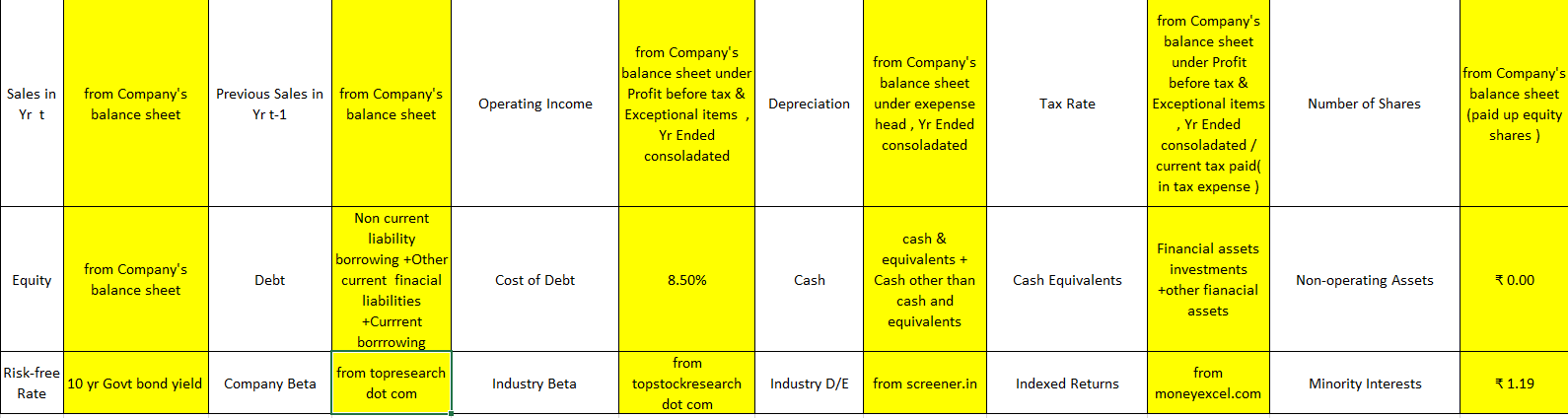

Where from one can find the data for Minority Interests however as you mentioned

“Actual Minority Interests of 4.27 multiplied by 4.5, the Basmati Rice industry’s average P/B Ratio”

3 Query

Based on what criteria debt is classified as a b c d and so on

4

Could you please suggest good book or online resource for advance excel

Thanks

Thank you. I’m sure it’ll be quite useful to boarders here.

I think you’ve missed two decimal places. ![]() KRBL’s Interest Payments (From Screener) is ₹69 Crs, not ₹6924 Crs. So the Book Cost of Debt is ~6% or so. I’ve used a 8.5% Cost of Debt to value KRBL’s Borrowings.

KRBL’s Interest Payments (From Screener) is ₹69 Crs, not ₹6924 Crs. So the Book Cost of Debt is ~6% or so. I’ve used a 8.5% Cost of Debt to value KRBL’s Borrowings.

Search for ‘Subsidiaries’. In every Annual Report, there’s a table which mentions the brief financials of Subsidiaries. I usually tend to take the Book Value of these Subsidiaries (Assets - Liabilities), multiply it with the industry P/BV and then multiply that final figure with the minority interest percentage (The percentage stake which the parent doesn’t hold). Here’s how I did it for KRBL:

As far as Advanced Excel is concerned, I would say simple YouTube courses should be very helpful. In case you’re looking for Finance oriented excel knowledge, please refer to the below:

That is really helpful thank you Dinesh so kind that you find time to answer

Regards

YourRaj

Prof. Aswath Damodaran has been putting up his Spring 2019 classes online. I think they offer immense value to those willing to look and learn. Seeing as how my model is largely based on the Professor’s own, I think it will offer a good opportunity to round things up for interested folks.

Valuation - Undergraduate

Valuation - MBA

Corporate Finance - MBA

Thanks for sharing the links!

Dinesh,

Once of the key inputs to the Damodaram model is the “Corporate Bond Spreads”. How do we get these values in the Indian context?

Thank you.

If you mean the Cost of Debt used to calculate Cost of Capital, then you can try searching ‘Corporate Bond Trading Data’ in Google. You will usually end up in these websites:

NSE: https://www.nseindia.com/products/content/debt/corp_bonds/cbm_reporting_homepage.htm

BSE: https://www.bseindia.com/markets/debt/tradereport.aspx

For instance, I would calculate the Cost of Debt for Reliance Industries as follows:

The problem in the Indian scenario is that Corporate Bond issuance isn’t as rampant as it is in the developed nations. So, you may not be able to get it for ~99% of the listed universe. In that case, I generally try to:

Thank you Dinesh. Have you tried using the ratings excel that Prof. Damodaran publishes every year? http://people.stern.nyu.edu/adamodar/New_Home_Page/datafile/ratings.htm

Do you think we can use this in the Indian context?

The Professor collects Synthetic Rating data based on companies listed in the USA. While it may be somewhat right, it may not exactly suit bonds issued in India. But yes, you can certainly use it as a tool for approximation.

This is coming late, but nevertheless thank you for this awesome post. Bookmarked it. I have a query regarding calculating Cost of Debt. Why is this taken from the credit rating and comparing it against the bond rates? I assumed that cost of debt would be the Interest costs incurred by the company for the debt that it has accumulated. Shouldn’t we be using the interest / finance cost from the P&L statement? How is it different from looking at the bond yields?

I am trying to use your model to build a baseline valuation for stocks that I would like to analyze and I am slowly learning the concepts that you have introduced in your excel sheet. Thanks again for the wonderful effort that you have put in.

Cost of Debt is the rate at which the company can raise Debt. Of course, this includes both the Debt Market and the Banks. Ideally, these should be pretty close.

As in, if Reliance’s plain vanilla Debt is trading at 7% in the Debt Market, they would also very likely get Bank Loans at 7% as well. If they don’t get it or Banks want higher rates, Reliance will just go back to the Debt Market and issue more Debt at 7% instead of quarelling with the Banks.

Thanks for the clarification. So for companies that don’t issue debentures in the market, can we take the post tax cost of debt from the income statement?

The order of importance I give is:

So if #1 and #2 are not available, then sure.

@dineshssairam I have another question related to finding the Cost of Equity from a basic CAPM based model.

I was looking at several definitions (Investopedia for example) and found that CAPM is derived from the Price of the underyling stock price and the overall market returns. Can I plug this Cost of Equity in a WACC calculation model? I am confused here because in WACC - the cost of debt is the Yield on the debt as you have explained above. For the cost of equity, can I use the stock price based CAPM or should I consider Dividend yield?

P.S - Sorry for bombarding so many questions in a single day! I am a newbie and I don’t have a finance background ![]()

There is a difference between the companies rate of return and your rate of return

A company uses its own rate of return to evaluate project IRR on a new expansion

For arriving at a valuation you would first see if what you can reasonably get from the bank. This is your risk free rate. To that you would add the risk and inflation as even bank rate you get can be beaten for instance by investing in a non inflationary unit of money

You are then discounting the future cash flows with that rate.

Using a company rate sometimes short cuts the process as you assume that banks are generally more efficient and if they are giving one company 9pc and another company 13pc, they feel the second company is more risky so you are using their analysis to cover your risk

Ideally you should have an idea of how banks price it. The higher the debt of a company the riskier it gets. So one company with a higher cash balance and lower debt might have a lesser risk and hence higher valuation than the one with higher debt

This is also the reason a well run company with good cash reserves command a higher valuation as the risk is lower and hence you are discounting future profits with a lower denominator

Do you know if he made and money on stocks or it’s purely theory

I tried searching what his net worth is and didn’t get very far

He should have been very successful by now and probably be running a large fund for the knowledge he shares

Some time back, I calculated the Cost of Capital of Reliance Industries from scratch and posted it in a different thread. Hope this helps you.