2 Likes

Poor Performance Continues in Nucleus Software

Hopefully recovers soon

Con-call Highlights -

Nucleus Software Q1 FY 2024-25 Earnings Call Key Takeaways

Financial Performance:

- Consolidated revenue: Rs. 195.4 crore

- Consolidated EBIDTA: Rs. 28.8 crore

- Consolidated PAT: Rs. 30.2 crore

- Consolidated EPS: Rs. 11.3

- Standalone revenue: Rs. 181.7 crore

- Standalone PAT: Rs. 31.2 crore

- Standalone EPS: Rs. 11.6

- Order book: Rs. 813.4 crore

- Cash and cash equivalent as of June 30, 2024: Rs. 920.8 crore

Operational Performance:

- Added 62 employees during the quarter

- Revenue mix: 58% domestic, 42% international

- No customer losses due to repricing initiatives

- Repricing progress slower than anticipated

- New customer acquisition yielded no revenue in the last quarter

- Long lead times for new implementations due to pricing complexity

Future Outlook:

- Management expressed confidence in bouncing back financially in coming quarters - Continued focus on product licensing and cloud-based services

- Plans to onboard sales leaders in different regions

Concerns:

- Decline in topline and bottom line performance

- Stagnant revenue growth

- Repricing initiative facing challenges

Other Important Points:

- Long-term focus over short-term fluctuations

- Committed to retaining top industry talent

- Exploring dividend payout and buyback options

- New product developments include an Islamic version of FinnOne Neo for the Middle East and Malaysia

3 Likes

Buyback meeting to be held on 22nd August, 2024 :

Link : https://www.bseindia.com/xml-data/corpfiling/AttachLive/020560ba-1ebf-457d-8011-2fde31fca0ef.pdf

1 Like

Not directly related to the fundamentals of Nucleus; wanted to work out the meaning of “Non-institutional investor” in a buyback.

Here’s the NSE demand schedule - https://www.nseindia.com/market-data/tender-issue-information?symbol=NUCLEUS&type=Active

Under “bid details”, do the NIIs categorized as “others” mean ordinary investors having shares worth > 200,000 in their demat account on the cutoff date, or they get clubbed with retail investors, and NIIs mean something else?

Now completely off-topic - this was the last buyback before Oct 1 where buyback-flippers had a chance to make real money. Post Oct 1, buyback proceeds will get treated as dividend, and get taxed according to one’s slab, while providing for acquisiton costs to be treated as a capital loss.

Positives:

- Nucleus releases a new module/update every year increasing value of product

- Being in fixed price contracts, the price escalations take time while wage inflation impacts EBITDA margins

- The contracts are usually 3-7 years long, with repricing followed at the end of the life

- Considering 2022 as the year of reprising and low EBITDA margins due to “The Great Resignation”, the same repricing can be considered to occur from 2025 to 2029

- The price charts reflect this growth over past 15 years with a flat to downward trend followed by a lumpy growth period

- ~Rs 500 crores of cash is 16.67% of the MV with no debt, allows for a downside safety in current market conditions

- The company has de-risked its business in terms of customer concentration, dependence on export sales, etc

Negatives:

- The CFO is low considering this being a tech company as the receivables is high, and the CFO could have been increased by using working capital

- The working capital to increase CFO will increase valuations and improve cost of capital, but the company is debt averse and holds cash

- The foreign subsidiaries do not make CFO as can be seen in their reported financials

- The company is dependent on BFSI doing well along with IT, both being neglected by the market

- Promoter selling stake in recent buyback, which is understandable by the fact that the promoter stake is very close to 75%. Arun Jain in non-promoter can be considered a promoter since he is with the company since 1990s. Therefore total stake is 74.3% which should come down after buyback

All-in-all, if the company is available at a good PE can purchase and hold for 4-5 years (2029) to see returns

3 Likes

Just will add another point regarding their new product in upcoming Co-Lending space.

Considering Nucleus reputation with their clients and future of Co Lending, I see this as a good growth handle along with Nucleus efforts to penetrate new global territories.

Current PE of 20 is lucrative and I am betting on a re-rating similar to Oracle Finance.

Although no direct comparison but I feel limited downside and a regular cash generating company with only organic growth is a slow and consistent compounder.

3 Likes

Wanted to understand revenue contribution and customer churn rate for each product. Could not find it in the annual report.

Is there someplace where I can find it ?

This IT company is presently trading @15 pe with market cap of just 2200cr. There is a cash of Rs 900 cr in fd/mutual fund etc as per last concall in the balance sheet.

2 Likes

Been researching this company and find it attractively priced, despite conservative management and huge cash on books which company is not using very productively over the last few years.

My question is now that buyback has become unattractive with change in the IT rules post Oct 2024 how will company use this cash going forward? They have consistently used buybacks over the years but now that’s off the table. Will they increase dividend payout?

What is tempting is the ex-cash company is available at PE of under 9 (Enterprise value of around 1300 crore)

Overall, classic case of heads i win, tails i don’t lose much as already stated in the beginning of this thread but good odds it will remain the same(value trap) for foreseeable future unless they make some uncharacteristically bold move(like an acquisition ) or even more ‘outrageous’ majority sale by promoters ![]()

Disc: No position but tracking

4 Likes

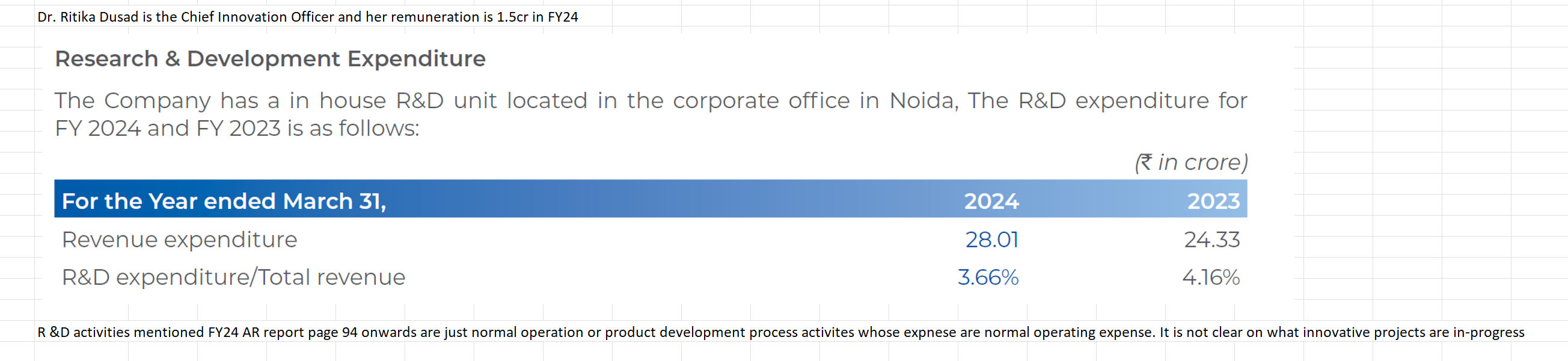

This info in FY24 Annual Report. Does company earn any rent for this 250 seater facility?

Nucleus Software Ltd.

Nucleus Software Ltd. (NSL) has operations in Jaipur with registered office in New Delhi.

It was incorporated in 2008 for facilitating delivery to larger clients through operations in a Special Economic Zone.

NSL acquired 17.41 acre of land in the Mahindra World Special Economic Zone, Jaipur and has co-developed a 250-seater facility.

The R&D activities mentioned in the FY24 Annual report are standard software product development activities, whose expenses should be part of operating expenses.

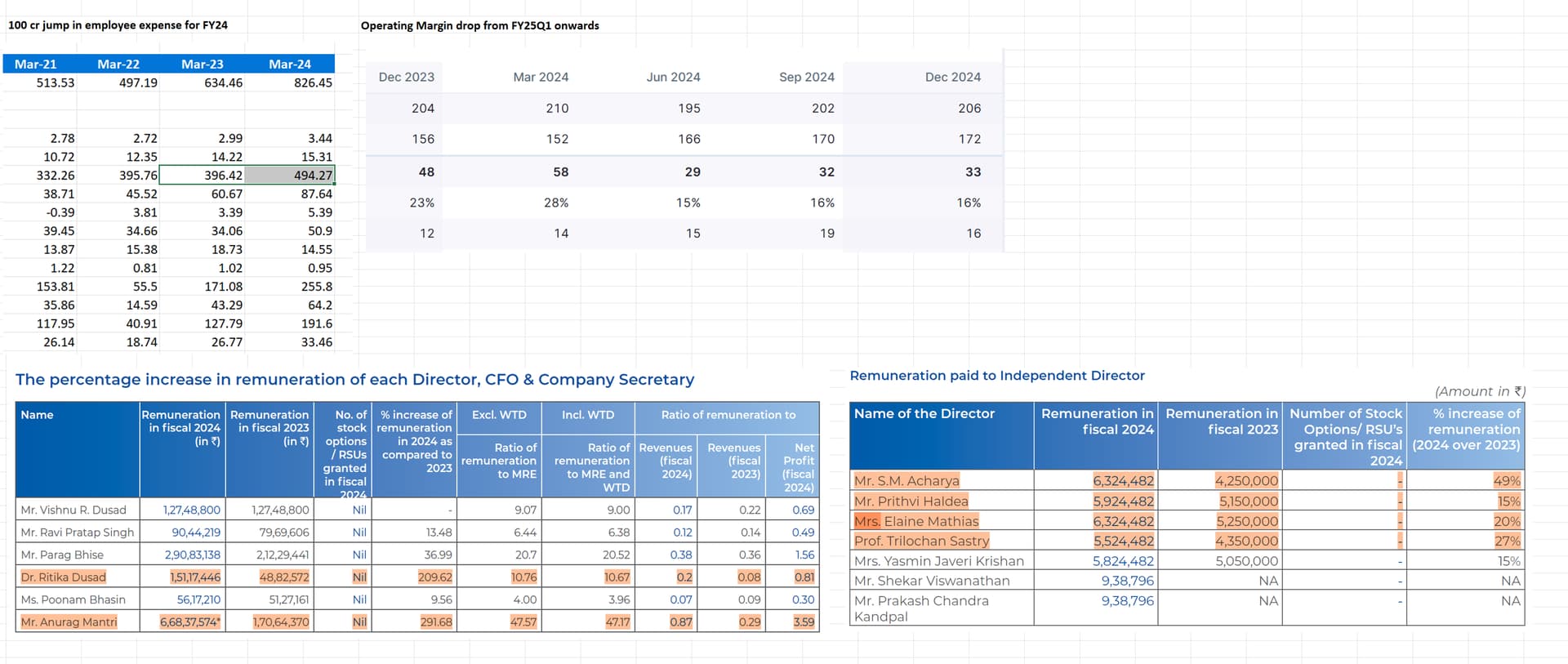

FY23 to FY24 the employee expense has jumped by 100cr and its impact on operating margins in FY25 quarters are high.

Please suggest whether my understanding is correct or not.

Good spot @umesh_venkatesh

Just wanted to clarify that are you saying this should be removed from R&D and just classified as normal revenue expenditure which I’m presuming will lead to 0% expenditure in R&D or they are claiming this as capital expenditure which will be more of a serious issue as it will be capitalisation of revenue expense?

Is this from notes from auditor section? I couldn’t find the relevant section in AR ( page 94 only shows director’s report without any clarifications/comments at the end)

I feel the most interesting investment ideas are also the ones which are the most simple. And this is an extremely simple investment idea

The company has two software’s which are its bread and butter.

- FinnAxia typically deals with big banks and institutions. It’s handling more than $15 trillion worth of transactions a year in 20 countries as of now.

- FinnNeo is a product which offers an end-to-end solution for lending businesses

Well-run SaaS businesses when they achieve scale, they become a sustainable cash guzzling machine. I believe that is the case for Nucleus as well:

- High exit barriers for the customer

From my scuttlebutt in talking to different banks and financial institutions, this software has a huge moat in terms of exit barriers as it’s not easy for most financial institutions to opt out of a software that has been deeply integrated in their internal processes. The extent to which this is present is such that some customers feel they would benefit from newer upgrades but are not ready for migration, causing delays and rather stick with the older versions.

The management in concalls claim that customers are very cautious about the solutions that they are choosing and their selection cycles have moved from typical 6 months to a year, sometimes 2 years and so on. Sometimes, even Boards get involved, which is something management did not experience in the past which shows that customers know the exit barriers to a banking solution quite well. Data about customer churn, attrition and new product/feature development-related information is not shared by management. Voluntary churn by customers is less than 5%.

- Pricing Power

Due to the high exit barrier and stickiness of the existing customer base, there is some limited pricing power they can exercise. Nucleus releases a new module/update every year increasing value of product. Being in fixed price contracts, the price escalations take time while wage inflation impacts EBITDA margins. They have some pricing power that they can pass on to the customers in terms of advancements and newer solutions they provide. The contracts are usually 3-7 years long, with repricing followed at the end of the life. The contracts are long term in nature and have a high repeatability rate at the end of tenure. With newer models and upgrades, repricing is available.

I feel the stock is depressed due to a few reasons.

- There is a lack of clarity of growth

The company’s revenues haven’t grown linearly and neither can the market see any fundamental growth from here on with great clarity. The management is very secretive on concalls about potential clients they are trying to acquire. But that is the nature of sales in this business where secrecy is paramount.

- Margins do fluctuate once a while as it did in FY22 primarily due to higher employee costs(usually)

Due to the nature of the business, the revenue growth is bumpy. Management has been spending more on marketing and will continue with marketing spend and hiring. However, since revenue is bumpy, the margin is also going to be bumpy. Margins in FY22 got depressed due to wage hikes, marketing spend and investment on technological functions while it was not compensated with growth in revenue.

- Lack of clarity of cash utilization

There is around 895 Cr of cash equivalents sitting on the Balance sheet has made investors anxious over its optimal utilization

- General market downtrend

The recent correction in markets particularly the smaller capitalization companies has depressed its valuation

Growth in such a company is usually uncertain and lumpy. It is directly proportional to the excellence of their sales and marketing teams. It takes time to get a client onboard and it’s a long, painstaking process. But once customer is acquired, there is a huge exit barrier for the client. This makes their present business extremely consistent and on the flip side, getting new clients to switch over to be extremely hard.

Management claims that they are getting a lot of queries from different players in different geographies including a big player who wants to transform their legacy system. It does not have any presence in the US but it does in a lot other emerging markets which gives them a huge opportunity of growth in coming years. Revenue mix is about 58% domestic and 42% international. They have a 700 Cr Order book executable over next 5 years. My bet here would be that management is able to crack the emerging markets and Indian market better over the next few years. Historically, their revenue growth has always been bumpy and I expect it to be the same in future as well.

The TAM as per management is $20 to $30 Bn since software cost for the lending business is between 0.5% to 1% of AUM but since they aren’t present in the US and some other developed markets, the real TAM for the company will be a lot less.

Conclusion

I feel the business is an interesting one due to customer stickiness, high exit barriers, some pricing power coupled with optimal potential for highly sustainable growth over the longer term.

On top of that they have a clean balance sheet with zero debt and 895 Cr of cash and cash equivalents. Promoter stake is high around 74%. They did a buyback of 150 Cr in 2021 at 700 per share and of 72 Cr in 2024 at a price of 1615 per share. The CMP is at a huge discount to the last buyback.

The market capitalization as of current date is around 2,000 Cr. If we take out cash balance of 900 Cr, the business is available for around 1100 Cr. And it earned 150 Cr last year. Even if we don’t account for any increase in OPM or revenue, the business is available at 7.5x PE and 1.3x PS

I find this company extremely peculiar. I understand why it’s cheap and there is a reality in which it might stay cheap or deliver sub-optimal returns for a long time. But it fits right into the kind of investment I usually look for. Something that has a great margin of safety and some potential of asymmetricity with a low current market sentiment(temporarily of course).

Please share any counter viewpoints please

9 Likes

Thanks for sharing. Have you adjusted 60cr other income from PAT in your calculation for 7.5x PE because other income is significant (>20%) portion of PAT?

5 Likes

Hi. Thanks for pointing it out. Apologies if I miswrote it. I meant it as 7.5x as a figure of Operating Profit. But the real calculations won’t be very far off as well.

Breaking down the “other income” on this front:

150 Cr OPM estimated

15-16 Cr depreciation

Considering 25% tax rate, it’s earning about 112.5 Cr and 15 Cr depreciation, turns out to be approximately 128 Cr.

They gained 33 Cr in investment profits, which I consider as one time non repeatable profit and hence not in my calculation for earnings growth. And an interest income of 17 Cr which is around 12 Cr after tax. And this income is repeatable and probably going to increase with increasing liquidity, but i’ll keep it as stable in my conservative approach.

With that you can take an approx figure of 130 cr as business profit and it comes out to be 8.4X PE and if we consider interest income and take 140 Cr as total profit (without investment gains), it turns out to be 7.8X PE (after taking out cash from market cap). The point is that in my opinion, considering whatever model that suits your investment framework, I find it valued cheaply and the estimates i have taken here are more on the conservative side (but what are conservative estimates can be up for a debate here).

5 Likes

Thanks for the note!

How much competition is there for the 2 Nucleus software solutions? And what is the TAM that the management is targeting out of $20-$30Bn? How is this TAM derived?

The fact that they did a buyback at ATH price of 1645/- suggests poor capital allocation on mgmt’s part.

1 Like

Some more notes based on my assessment of the company and management :

- Looks like repricing over the last couple of years has driven revenue growth as well as margin improvement but the margins are coming off because of the investments they are making in new product developments, existing product upgrades, investments in AI etc. (as per Q3FY25 mgmt. concall); as a result, OPM% is now 16% (Dec’24) vs 40% as of Mar’23).

-

Nucleus looks like a small company behaving maturely in a large market. Growth is a concern in the short term but in the long arc of time, consistent high single digit revenue growth and mid-teens Profit growth can be expected. It looks like a consistent slow compounder what with it’s contract repricing, customer value addition through tech implementation, and conservative mgmt. It’s important to buy such companies with a good margin of safety!

-

This company’s performance will be synced up with the Lending cycle. As the rate cut cycle brings in conditions for credit growth, there should be some traction for the business too.

-

Mgmt is super conservative (maybe less ambitious too?) and overly secretive. There is no clear succession for promoter (Mr Vishnu Dusad is likely to be in his late 60s). Dr Ritika Dusad looks highly qualified (PhD in Physics and all) but took a career break after a stint of around 3 years with the company in key positions (this is as per her Linkedin profile). Couldn’t find anything on Madhu Dusad/Kritika Dusad or the other co-founder Mr Yogesh Andlay.

-

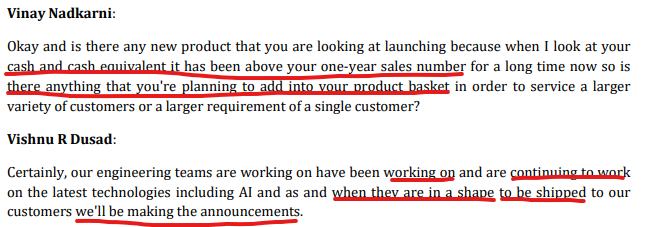

Use of cash is uncertain; product development & customer acquisition journeys are uncertain. Answers from mgmt. on these aspects are vague at best. For e.g. below extract is from Nov’24 transcript. (Another view : Mr. Buffett hoards a lot of cash at all times but he is upfront that he is looking for smart acquisitions - something similar from the mgmt. would be great! Nobody is looking for dividends

!)

!)

-

KMP/Employee cost (FY24) : CEO 2.9 crs, COO 6.7 crs, Mr. Vishnu Dusad 1.3 crs, Dr Ritika Dusad 1.5 crs. Total KMP compensation is ~13 crs which is 2% of revenues from product & services. This is in line vs Newgen but higher than Intellect Design Arena (0.3%).

(It is possible that I could be missing something in Intellect design’s KMP % calculation!)

-

Raw engineering & product management talent is needed to run and grow this business over time. I saw a few employee profiles on Linkedin and it looks like this company does a good job of employee hiring and retention - Few senior Product Mgrs and Senior Engineers have been with the company for 10+ years & have very decent profiles. For e.g. Amit Jain (Head Engineering - FinnAxia; 13 years), Lokesh Pathak (Head Engineering - Finnone Neo; 10 years), Ashish Khanna (Chief Marketing Officer, 17 years), Rohit Mathur (AVP Digital Transformation; 22 years); Shashank Bhaskar (VP; 25 years).

-

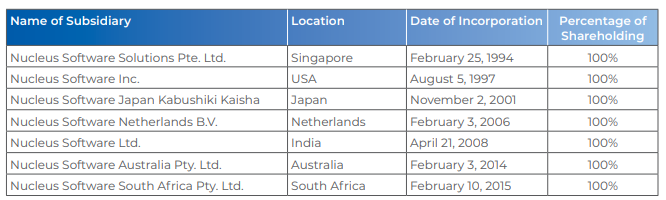

RPTs & relations with subsidiaries : Nucleus has 7 Wholly owned subsidiaries (More on this in another post along with audit opinions)

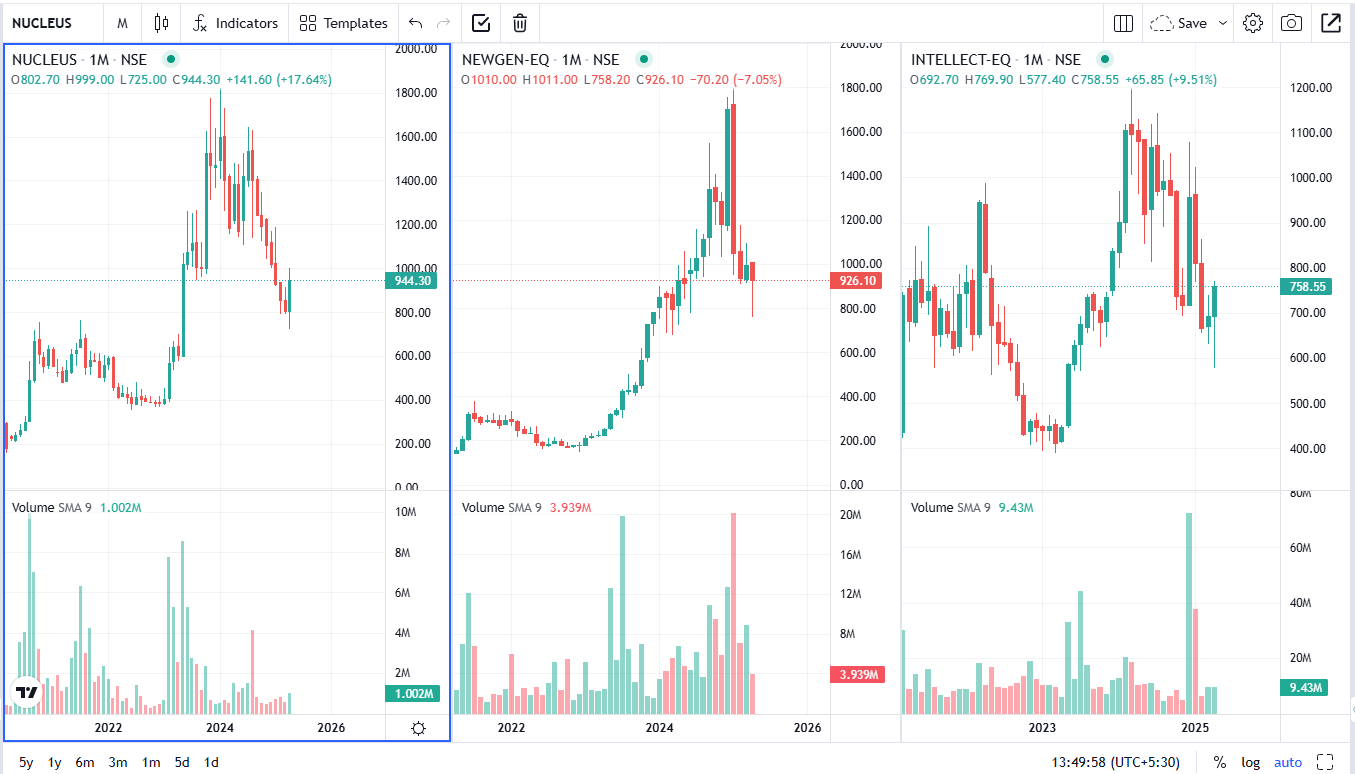

- Technically, the stock is attempting a bounce back from its key support levels of 750~ on the monthly chart. Any further buying pressure should help break this stock from LHLL pattern seen since ~Aug’24. Any break from this support level will cause more pain for holders from higher levels. Price action is more aligned with Intellect Design Arena.

Disclosure : Invested with a small tracking position and trying to answer some more questions before deciding to add/exit.

2 Likes

@Adhiraj - As you said, it does seem to fit the idea of an investment which offers decent margin of safety along with real potential for asymmetricity.

1 Like