And that’s why I told… It’s conservative ![]()

Only 2-3 percentage of their total non current investments

Some more digging ![]()

Temenos is the market leader and it has grabbed some key executives from Nucleus before.

Examples

- https://www.linkedin.com/in/jiteshmalik/

- https://www.linkedin.com/in/vibhooti-chaturvedi-a73b2315/

- https://ibsintelligence.com/ibs-journal/ibs-news/c381-ibsj-archive/c347-ibs-journal-archive-2011/temenos-spearheads-consumer-banking-push-with-ex-nucleus-software-senior-exec/

Below is the list of software and associated sales in the industry (global)

https://www.temenos.com/contentassets/894a4f9744ab45a8aef8edb48f5cc1e5/ibs-journal-april-2018-feature-focus.pdf

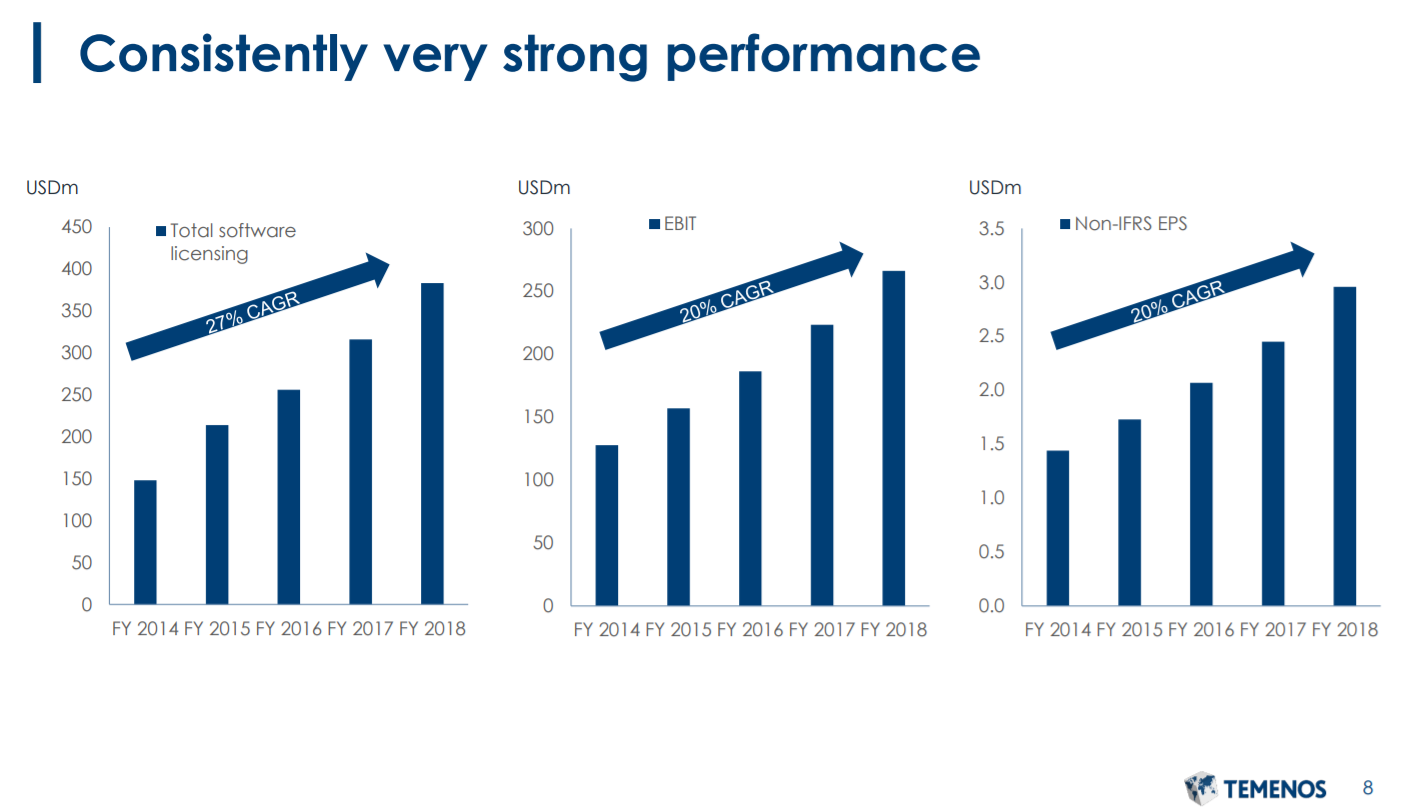

And, coming back to Temenos, it currently is at PE of 60 because it is very aggressively trying to capture the market (leveraged at 1.6x). A screenshot from their investor presentation below:

Another aspect is the split of product revenues. Form another competitor Silverlake Axis, you can find that the maintenance and support constitutes about 70% of the total revenue. SLAxis has a bit longer history and hence this can be expected. Wondering the case with Nucleus.

2 Likes

In its AR, Nucleus has clubbed together licence fee, maintenance and support as ‘product revenue’. So you won’t get the exact split between license/product sales and maintenance/support. However most product companies operate similarly and I would imagine the ratios for Nucleus would be similar to that of its competitors.

In my understanding Temenos competes with the likes of Finnacle (Infosys) and BANCS (TCS) in the core banking software category. Nucleus specializes in loan management systems (LMS). Both are complimentary. For example a bank would need both, whereas an NBFC would just need LMS.

1 Like

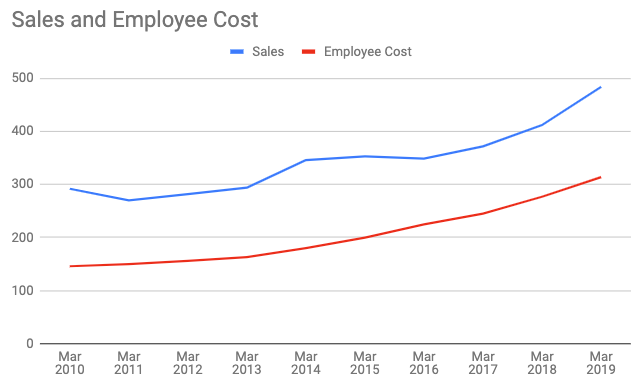

I was looking into Nucleus and noticed its slow growth in top line and its low operating profit %. Its operating profit % is stuck in the 14% to 16% for some years. It seems like it is a services company in the disguise of a product company.

It doesn’t seem to be operating in a niche nor does it seem to have a scalable product (i.e. a product which scales without needing to add employees)

Its employee cost has grown in line with its top line.

Data source: Tijori

How is this even possible for a product company? Can other members, with a background in IT products and services, provide an explanation?

6 Likes

Incompetent management which completely lacks growth mindset.

One example is:

They created a fintech solution PaySe in 2015 but did nothing about it except showcasing it to sale core product.

https://payse.cash/

A smart management would en cashed that for few hundred million dollars in fintech boom. We are past that hype already so not much can be expected in future.

2 Likes

Only if they had named it paytm

Name was not that bad ![]()

But they did not do anything with it and slept over it.

In fact their product and services also has had such a tepid growth for last decade putting a question mark on their appetite to grow.

1 Like

i really dont think one is paying here for growth at all.

With a current market cap of INR 702 Crores, and cash in books worth INR 532 Crores, this business, which brought in operating profits of INR 71 Crores in 2020, is valued at mere INR 169 crores.

Which is perhaps scary, since I am unable to understand the discount which is given by the broader set of market participants to the current cash in its books. Nucleus management has been very conservative with its cash and has been hoarding the same in its books since years, mostly citing acquisition opportunities In fact, it even cancelled the INR 9 per share of dividend it had announced right before the coronavirus pandemic hit citing conservation of resources (cash in books is INR 189 per share).

Although I think the decision of conserving cash made sense, they seem to be almost drowning in it. Further, always being 10 feet away from the truth, I cant discard the possibility of some of the cash simply not being there (considering the valuations the company has commanded in most of its history). However, listening to calls that go back years, I am willing to put my neck and money out to claim that I do not sense any shenanigans here. I could be totally wrong about this, but based on the consistency of the management commentary, I am willing to take that risk and am thus invested.

I have written a detailed thesis on the company here -

feel free to get back with your views.

happy investing!

13 Likes

Attended Q4 FY21 Call and below is attempt to summarize

• Co. reported 124 Cr in Rev ,NPAT at 27crs for Q4 FY2021, YOY(Q4 2020) Rev and NPAT was at 138 crs and 28crs repectively. Co. declared Rs 6/Share Dividend

Cons

• Malware Attack recently on Nucleus Website, though there is no Data Leakage as Nucleus does not store data with it but it does affect Discussion with Prospective Clients

• Higher Attrition in IT industry overall and Nucleus will lead to higher cost which affects Margins

• Flattish Sales , sales growth is 6 % CAGR for last 10 years

• Though Op and Net Profit Margins were better at over 20 % in FY 21 cos of Reduced Travelling Cost and Office Related Costs, however over the period they shall revert back to earlier levels of 18-20%

Pro

• Mgmt claims 70percent Loans originated, serviced or collected in India are via Platforms of the Company

• Bank of Sydney has signed up with Nucleus Software effective Q1 FY 22 , though Contract Amt is undisclosed

• Mgmt is in talks with Fintech Companies in India to adopt their Software (Bajaj Finance , HDFC Bank , HDB Financials etc are already their clients )

• Company is sitting on cash and inv of Approx 680crs as on March 2021 , at price of 580 Mcap is at 1685crs

• The Lending software cant be easily replaced , so it gives kind of a moat to them but then it is prone to events like recent Malware Attack

Inference

• Order book appears Flat Mgmt , however since they have managed to rope in Bank of Sydney as their client they expect their next Aussie client soon. In Australia the loan processing is quite Manual and is potentially a nice Market for the Company however the Company hasnt able to capitalize on it as can be seen that they entered the Continent in Yr 2016 and still havent made Notable progress.

• Growth in Rev is a concern even though their Lending Software is rated among top 3 in the World , though the Company has claimed that they have Moved people who have operational Knowledge of their Softwares to Sales so that they can convince Prospective Clients regarding uses of their Software.

• Rev can be via 2 Model ,Transaction Based and the Traditional Licence Fee based , Most of their clients are on Licence Fee based and hence stable Rev.

• The Product is Great , Financials are good , but Lack Lusture Sales raises Growth concerns from Investor pt of view.

Disc: Divested

5 Likes

I was researching this company over the last few days.

This seems to be one of the perfect examples of a company that has created a niche in a market. And it is very hard for competitors to grab them but hard for them to grow too which put themselves in a sticky situation . The customers sticking to them after a malware attack seems to imply some moat around the product.

They claim to have around 70% market share in India (might be less in reality as the metric they use to measure it is somewhat tricky). But nonetheless, they have a dominant position in India that is not easy to take down for any competitor.

The good thing about the company is that it has a really strong balance sheet( as do most IT companies). Around 700 Cr cash out of which 450cr is parked in mutual funds. This serves as a huge margin of safety. But the issue is that it is hard for them to grow from here.

For them to grow, there are three options:

• Use the cash to acquire a competitor or acquire another company to enter a new product market.

• Use the cash to grow in new territories and countries. They are trying to grow in Australia and acquired 3 customers there. But it is a long road to put your mark in another country and their sales team have to do exceptionally well. Also, only around 180 cr of their 520 Cr sales are from India. Rest are all diversified markets except North America. So, growth prospects are also limited (Unless they get into US which is a huge market).

• Or sit on cash and consolidate their position as a leader in India. If their customers grow, they will have higher revenues. (They currently work under two models – license based and transaction based. Transaction based can grow if their customers do well)

The management came across well in concall transcript. Also, there doesn’t seem to be any integrity issues too (i might be wrong here as companies that keep so much cash are usually tricky in such scenarios).

But I find it hard to believe that being ultra conservative and cautious as they are, they will do buybacks or give huge dividends. So, they might go for Option 1 or 2. Option 3 gives them low sales growth.

But as of now, it all depends upon the management and their capital acquisition skills to grow this company.

This might serve as a good investment if bought at cheap valuations. But not so sure at current valuations because of hinderance to future growth. Valuations are certainly not expensive but they are neither mouth-watering as they were a year back. At this stage, be on this company is a bet on future management capital allocation decisions which are a little tough to predict as they were not much clear about it in their concalls as well. It for now seems to be a good value bet if available at cheap valuations and not a consistent compounder as some in Tech/IT industry seem and its certainly not worth paying up for.

Disclosure- Tracking

5 Likes

Nucleus Results for Q1’22 are terrible, Revenues declined, and profits nose dived.

In the press release, management attributes it to Wage hikes handed out to combat attrition, but we have not seen a similar impact on IDA, OFSS financials, could be relate due to the ransomare attack.Till last quarter they had not hinted at any abnormal margin pressure. The press release talks of “Bold steps” lets hope this jolt does make them wake up and try something innovative, they have been coasting along for quite a while. And hopefully new CEO in charge can use the opportunity to do some org revamp. The conf call will be interesting to see if they do talk of any tangible plans.

Revenues Rs. 108 Crore vs 124 (Q4) and 128 Cr (Q1’21)

PAT 6 cr vs 27Cr (q4) and 36 cr (Q1’21)

EPS at Rs. 2.07 vs 9.04(Q4) and 12.5 (Q1’21)

Disc: Invested and holding.

2 Likes

I attended the earnings call. Voice quality was patchy, so lost some of the conversation, but sharing the notes from what I heard:

1 They hope to be back to normal profitability in a few quarters, but no specific projections.

2 There were no announcements of plans to go after more marketshare in advanced markets (unlike IDA), just a general statement that we want to get more business in those geographies, which was something they have stated earlier too.

Revenues were partly impacted due to the Covid 2nd wave disruption, and then the ransomware attack.

3 Customers were back in operation in few days to a maximum of 2 weeks. Customers have stuck to them, there have been no cases of customer levied penalty.

4 Salary hike was effective from 1 April, but communicated in July, and arrears were paid out.

5 Managing retention and ESOPS: Was disappointed by the way the question was handled both by Parag Bhise the CEO , and Vishnu Dusad the CMD. Parag said they are looking at hiring 500 freshers, but a good product company cant work like a services company with a pyramid structure, domain expertise is very critical to create and retain, by keeping your experienced engineers. Vishnu categorically stated they are not in favor of ESOP as a compensation and long term retention tool as it creates risk. On Probing if it was dilution risk that was worrying them, he said no, it is more system balance which was very baffling, given the huge stake he owns. He said they will look at other stock based compensation, I guess they might be exploring SAR’s.

Disc: Invested and holding. Valuations and the space are very attractive, but the management mindset is too conservative. Will watch for a couple of quarters before adding further, or divesting.

3 Likes

Nucleus has announced buy-back upto 22,67,400 (Twenty Two Lakh Shares ), comprising of 7.81% of the total paid-up equity capital of the Company,

at a price of Rs.700/- (Rupees Seven Hundred Only) per Equity Share.

One strange sentence in the notice:

“The Board noted the intention of the Promoters and Promoters Group of the Company, to participate/ not to participate in the proposed Buyback.”

I am not sure if this means Promoters and promoter group will NOT participate in the Buyback, so the acceptance % will be much higher than the 7.8 % ?

Does anyone have clarity on this ?

Disc: Invested and holding. Attractive space and valuations, but very conservative management, an activist shareholder can do wonders for this company.

Opel Vauxhall Finance announcing the going live in Spain with Nucleus Software’s flagship lending product, FinnOne.

Buyback announcement by Nucleus Software of Rs 158 crore for 22.67 lakh shares at Rs 700. 30% premium to closing price today.

Interestingly, promoter to tender only 1 lakh shares, which means 95% of buyback will be for public.

As per my estimates it is a safe opportunity, the ratio should be almost 1 in 3.5 shares. Assuming 1 in 4 and a constant share price, the opportunity would be to make about 5.5% return.

Example :

100 stocks x 575 = 57500

25 stocks buyback x (700-575) = 3125

3125/57500 = ~5.5%

Disc : Not Invested.

2 Likes

Did u factored the 15% reservation for small shareholders? I blv if u consider that the acceptance ratio will be much higher for smaller investors i.e in the range of 40-50%.

Of course the issue is that the price run-up of almost 25 rupees has reduced the differential amount.

Buyback of Nucleus software.

Can someone check my analysis and validate. It looks like a super arbitrage opportunity.

| Total shares | 29040724 |

|---|---|

| Promoters | 19627866 |

| Non promoters | 9412683 |

| Promoters willing to tender | 107926 |

| Total possible Tender shares | 9520609 (Non promoters+promoters willing to tender) |

For retail

| Total buyback shares | Retail quota | Retail quota %age | Total potential retail shareholders | Acceptance Possibility (Retail quota/total potential retail shareholders) |

|---|---|---|---|---|

| 22,67,000 | 3,40,050 | 15% | 53,27,000 | 6% |

For non Retail

| Non Retail buyback shares (22,67,000-3,40,050) | Total potential non retail shareholders willing to tender | Acceptance Possibility | |

|---|---|---|---|

| 19,26,950 | 41,93,609 | 46% |

46% AR is if all the non-retail is participating. In reality it should be much much higher.

Current arbitrage is 18% ( buyback price= 700 CMP= 590)

3 Likes