Some more notes based on my assessment of the company and management :

- Looks like repricing over the last couple of years has driven revenue growth as well as margin improvement but the margins are coming off because of the investments they are making in new product developments, existing product upgrades, investments in AI etc. (as per Q3FY25 mgmt. concall); as a result, OPM% is now 16% (Dec’24) vs 40% as of Mar’23).

-

Nucleus looks like a small company behaving maturely in a large market. Growth is a concern in the short term but in the long arc of time, consistent high single digit revenue growth and mid-teens Profit growth can be expected. It looks like a consistent slow compounder what with it’s contract repricing, customer value addition through tech implementation, and conservative mgmt. It’s important to buy such companies with a good margin of safety!

-

This company’s performance will be synced up with the Lending cycle. As the rate cut cycle brings in conditions for credit growth, there should be some traction for the business too.

-

Mgmt is super conservative (maybe less ambitious too?) and overly secretive. There is no clear succession for promoter (Mr Vishnu Dusad is likely to be in his late 60s). Dr Ritika Dusad looks highly qualified (PhD in Physics and all) but took a career break after a stint of around 3 years with the company in key positions (this is as per her Linkedin profile). Couldn’t find anything on Madhu Dusad/Kritika Dusad or the other co-founder Mr Yogesh Andlay.

-

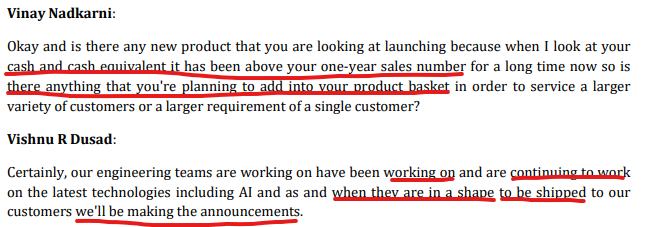

Use of cash is uncertain; product development & customer acquisition journeys are uncertain. Answers from mgmt. on these aspects are vague at best. For e.g. below extract is from Nov’24 transcript. (Another view : Mr. Buffett hoards a lot of cash at all times but he is upfront that he is looking for smart acquisitions - something similar from the mgmt. would be great! Nobody is looking for dividends

!)

!)

-

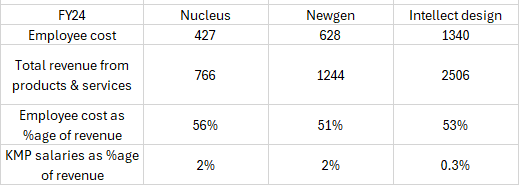

KMP/Employee cost (FY24) : CEO 2.9 crs, COO 6.7 crs, Mr. Vishnu Dusad 1.3 crs, Dr Ritika Dusad 1.5 crs. Total KMP compensation is ~13 crs which is 2% of revenues from product & services. This is in line vs Newgen but higher than Intellect Design Arena (0.3%).

(It is possible that I could be missing something in Intellect design’s KMP % calculation!)

-

Raw engineering & product management talent is needed to run and grow this business over time. I saw a few employee profiles on Linkedin and it looks like this company does a good job of employee hiring and retention - Few senior Product Mgrs and Senior Engineers have been with the company for 10+ years & have very decent profiles. For e.g. Amit Jain (Head Engineering - FinnAxia; 13 years), Lokesh Pathak (Head Engineering - Finnone Neo; 10 years), Ashish Khanna (Chief Marketing Officer, 17 years), Rohit Mathur (AVP Digital Transformation; 22 years); Shashank Bhaskar (VP; 25 years).

-

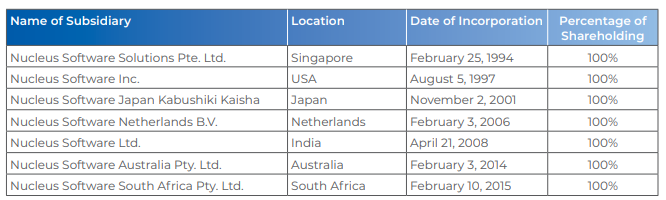

RPTs & relations with subsidiaries : Nucleus has 7 Wholly owned subsidiaries (More on this in another post along with audit opinions)

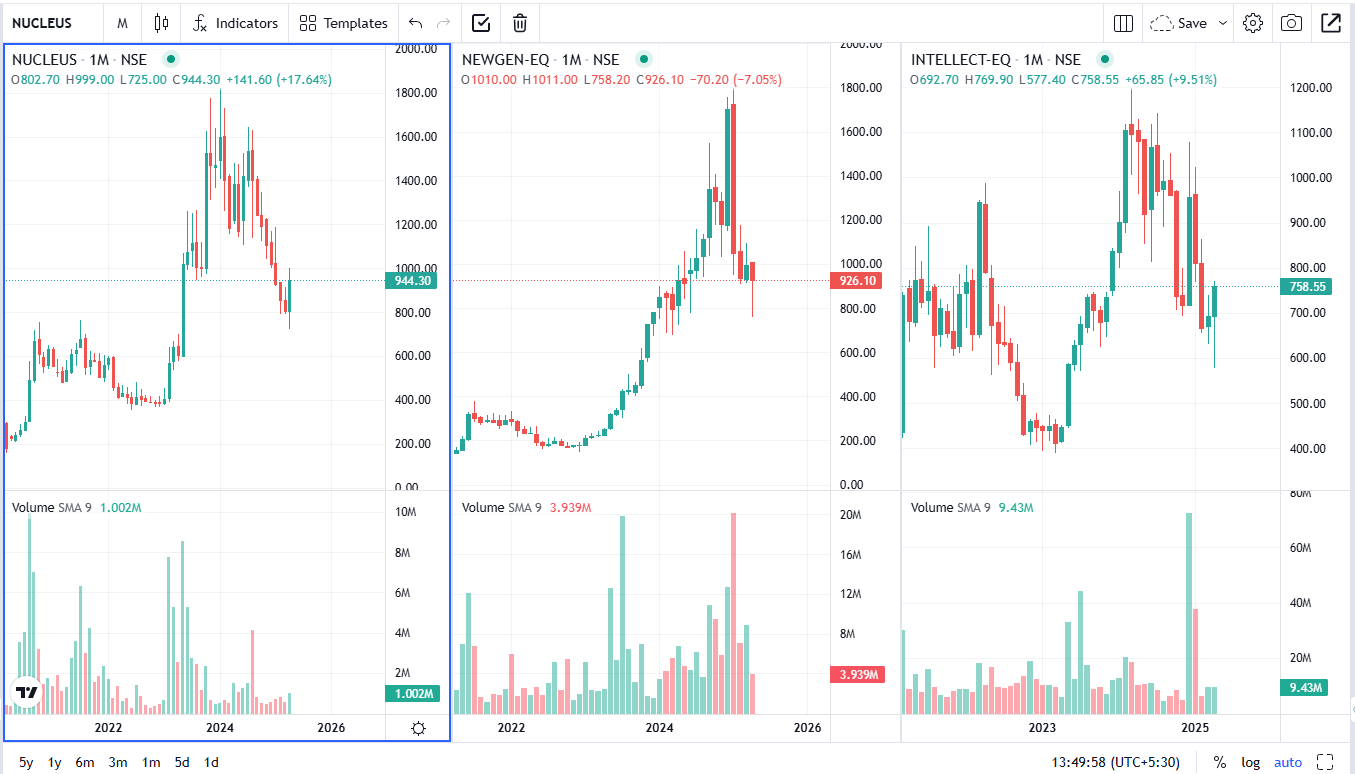

- Technically, the stock is attempting a bounce back from its key support levels of 750~ on the monthly chart. Any further buying pressure should help break this stock from LHLL pattern seen since ~Aug’24. Any break from this support level will cause more pain for holders from higher levels. Price action is more aligned with Intellect Design Arena.

Disclosure : Invested with a small tracking position and trying to answer some more questions before deciding to add/exit.