NRB bearings is a company working on those invisible tiny bearings which make things move. If someone wants to understand about bearings then below video series is the best I found: https://www.youtube.com/watch?v=91_VaGiU1Is

Interestingly, the world is going crazy with precision engineering due to demand from sectors like aerospace and defence. NRB is essentially into precision engineering and market leader in needle bearings. NRB had a great promoter few decades back (Trilochan Sahney). He had two children Harshbeena and Devesh. Not much is known about Devesh (and irrelevant for this discussion) but Harshbeena on the other hand used to be in limelight. She may not have technical qualification for a company like NRB but started from the floor shop and worked her way to the top management (not necessary due to merit). She is widely credited with opening the first R&D center of NRB in the year 2000. Even today R&D is a rare occurrence in Indian corporates and many are being punished severely for it. At the time, NRB had marquee clients like Maruti, Bajaj Auto, Yamaha, Hero Honda, M&M, Renault, Volvo, General Motors, Electrolux, GKN. In 2007, they were clocking 300 cr in revenue with great growth. In fact, Harshbeena gave a revenue target of 1 billion dollars (4500 cr inr at the time) to be achieved in 2020. Fast forward to 2026, they are nowhere near this target with current revenue of 1335 cr. So what happened? NRB was hit by global recession, sibling rivalry, death of promoter, covid and factory fire. Their major revenue comes from auto which is a cyclical industry. Suffice to say, targets of more than 2 years are hawa-hawai baate in my opinion.

After being hit with all these problems and losing 16 years in the process, the dark clouds finally lifted when siblings came to an agreement in 2024. Harshbeena would control the crown jewel ‘NRB Bearings Ltd’ while her brother will get the industrial business and a large sum of money as one time compensation. She took huge loans by pledging all her equity and paid the compensation. What she got in return was complete autonomy over the business. Nothing stands in her way now and on top this she will be motivated by the huge pledge to work harder than ever. At least thats the narrative!

Below is the brief of commentary in q4 fy26 concall:

Harshbeena handles nearly all questions and her technical knowledge is quite good. numbers are at ATH, revenue is 372 cr with ebitda at 74 cr (~19% margin) and pat of 146 cr. They have been impacted by gas shortage meaning q1fy27 numbers may not be that good. blended utlilization is around 85% while brownfield capex is underway and will finish by q1fy28 in piecemeal. They are entering into industrial friction solutions in segments such as construction equipment, off highway, industrial gearboxes, switchgears, and power generation. They have also also entered into aerospace.

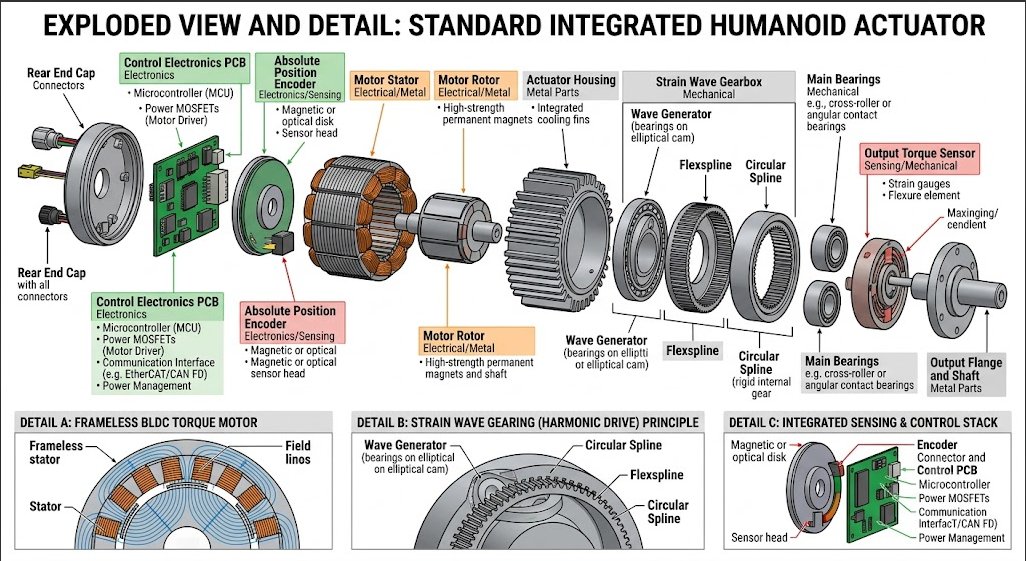

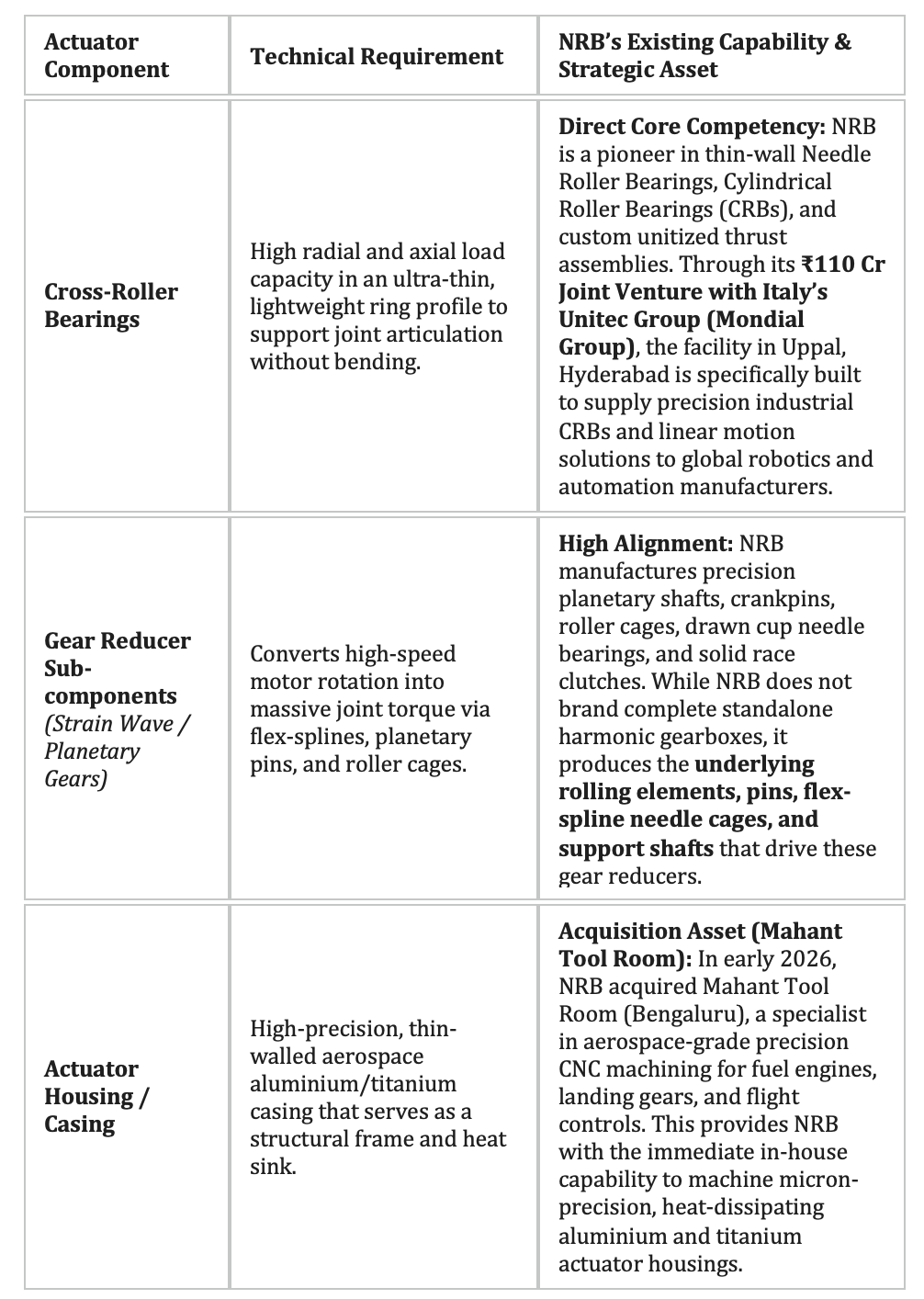

Aerospace is a very difficult sector to enter into as it demands nothing but perfection. A small failure in some component of an airplane is enough to take down everyone on board. And humans always had extreme reactions to flight crashes. Tens of thousands may perish on roads but a single plane crash sends massive shockwaves all around the world instantly. NRB always had the capability to cater this industry and they claim 100s of RFQ from aerospace division. After all their clients are the likes of bmw, mercedes, audi, volvo. What they did not have was AS 9100 certification which is a must to enter this sector. So they acquired a small company called ‘mahant toolroom’ which is already a supplier to HAL with an order book of 50 cr. This essentially saves the company few years to acquire the certification organically. I believe this is the reason why market has pushed the stock to ATH valuation.

NRB is a market leader in needle bearings for auto industry with over 60% market share. They also claim to be EV transition proof meaning ICE-age ending will have no impact on their business. It is important to note that they are not making any engine components but more into transmission.

Risks: I believe there are several key risks to this business. First is promoter pledge which they are reducing fast by selling stake and restructuring loan. Pledge stands at roughly 77% right now. Another risk is cyclicality of auto industry. Currently we are in auto boom cycle which is not a good starting place to bet on auto related stocks.

One subjective opinion on promoter is she comes off a bit too much sometimes to me. But so far in my research she came as a competent leader. One can also consider her age (66) as a risk. Succession triggered nasty rivalry and company suffered in the past.

If auto cycle risk plays out the market cap can easily slash by 50% from current levels. They must scale fast into other divisions as sooner or later this risk will play out.

Disc: invested at recent levels with small position and looking to build more. I was going through Bharani’s threads and something he said on capabilities hit me hard. Market is not rewarding companies on basis of what they are doing but rather what they can do (future earnings and growth visibility). Those companies which can handle mission critical components are far likely to do better than others. I think NRB fits the case of a company with hidden capabilities in its balance sheet. Even with all the issues of past they are a market leader in the part of precision engineering they do. Its not easy to acquire such competence.

I must share another bias I have. I believe we are in a bull market since April 2026. I look at charts and most stocks had run up in April (gadhe-ghode sab bhag gaye). Then we had some issues in May and many either fell or remained flat. But some refused to fall and rather continue to climb up in May as well. NRB is one such stock. Though it maybe a bull trap but I decided to pull the trigger with a small position. Rest markets will decide in the end, bhav bhagwan che