Why has the promoter pledged around 90% of their shares? On the flip side, looks like their repayment of borrowings has picked up.

1 Like

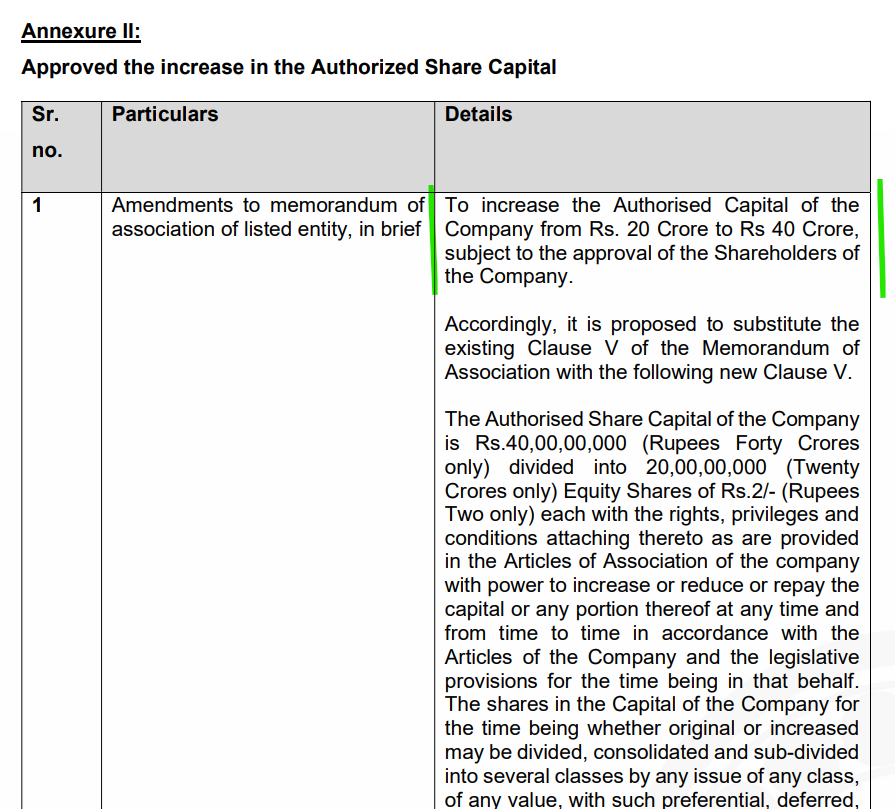

Authorized Equity share capital increased from 20Cr to 40 cr. As there was settlement among family members recently, now with single owner (Mrs Harshabeena Zaveri) have more control on deciding on capital allocation / future expansions. The increased authorised capital to 40cr is giving a signal of a fund raise ?

https://www.bseindia.com/xml-data/corpfiling/AttachLive/05ed8b78-22fe-4527-ac4f-2b18403d6065.pdf

Disc: Invested and no transactions from last 3 years.

6 Likes

does it means promotor holding will come down to 25% ? or promotor will pump large chunk ! but they have pledged 90% in past means they have no money on hand !?

so how to interpret above one…

second on the positive side ,they have huge oppurtunity to invest almost same amount as Current m-cap, right ??

disc. invested

1 Like

Increased authorized doesn’t mean promoter holding will go down. But it depends on the avenue they chose to raise the capital - QIP, rights issue or preferrential allotment. Also, there is no official communication about fund raising. Authorized share capital needs to accommodate if there is any new shares in future that is going to come. Only management can clarify on the reason for increased authorized capital. I am just taking some guess as to why management increases authorized share capital simply (May be some senior members can enlighten more on this topic)

Regarding the pledged shares, there was a recent settlement among family members and the IP usage “NRB bearings”. I feel the money from pledged shares might have been used for settlement among family members. Also you can check recent filings reg the same. Promoters are releasing pledged shares slowly.

1 Like

I sent an email to investorcare@nrb.co.in asking for any public disclosures regarding the pledging of shares. That was six days ago but still awaiting a reply. I would like to know if companies in India are required to disclose promoter pledging of shares and reasons for doing so. Is it required?

Also, see that the unpledged promoter holding has ticked up to 17.5% (source: screener.in) as of today.

Anyway, my reasons for investing in NRB bearings is because of its market share, leadership under Harshbeena Zaveri. She seems like a trustworthy person from her educational background to her personality in her interviews. I came to know about the company from reading Pulak Prasad’s What I Learned About Investing from Darwin. So, the company has passed the filter of his investment company, Nalanda Capital, as well.

Low debt to equity, reasonable ROCE, significant promoter holding (though pledged). Let’s hope they continue to do well in the future for the sake of all stakeholders of the company.

3 Likes

AGM Transcript - Management tone seems to be very confident on the future growth.

Disc: Invested.

https://www.nrbbearings.com/AGM%20Speech%20-%20NRB%20Bearings%20-%20Final%20V5.docx

VC & MD Transcript

Good evening Shareholders,

It is my immense honour to address you at this Annual General Meeting of NRB Bearings. Let me say, first, that there is an irreplaceable connect that comes from being able to convene in person. I hope that next year we will by meeting in person. The only advantage with a virtual AGM is that more of you are able to participate. The experience is more elevated when there is good news to share with you, our stakeholders and I am privileged to be able to do that today.

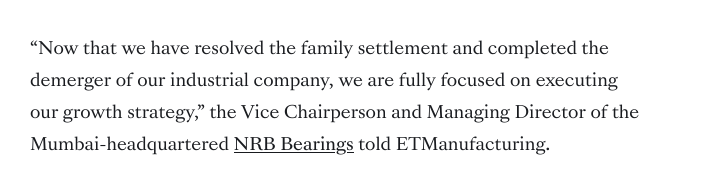

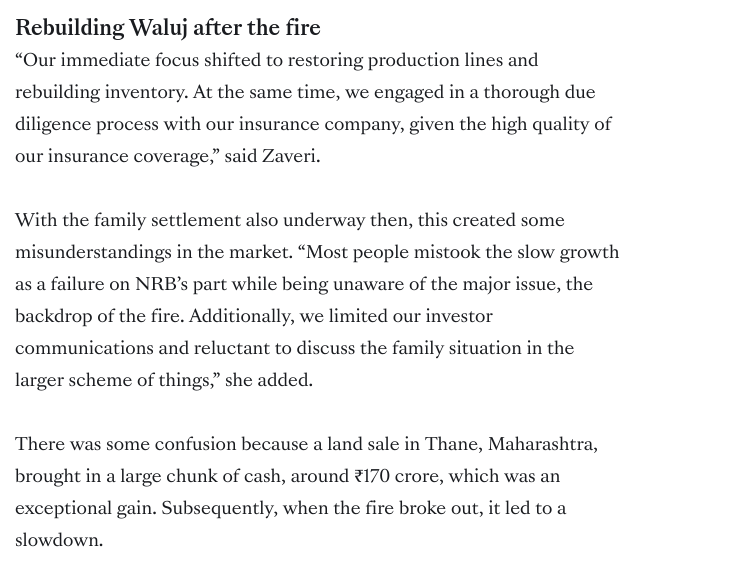

The events of the past year have demonstrated that the true strength of NRB is beyond financial metrics - it is the ability of your company, our colleagues, our teams, to withstand disruption, adapt with agility, and emerge stronger with each challenge faced. After the pandemic, which we handled exceedingly well and bounced back, we faced an operational setback – a fire at our Waluj facility that disrupted one of our most critical lines. The impact on revenue growth and profitability was felt for our two financial years. Our teams worked tirelessly to restore production, rebuild stock, and ensure that every customer relationship remained intact. I am proud to say that since January this year, when full capacity was restored at Waluj, we moved back to achieving our growth forecast, with profitability exceeding 19% at the EBITDA level (as a percentage of sales).

At the same time, we were conscious that the settlement had created confusion in the market. Exceptional items such as the sale of land in Thane (which took place in the same quarter of the previous year), insurance settlements related to the fire, and one time pay-out on the inter-company arrangement, confused shareholders. Many were not able to comprehend our excellent operational performance (without exceptional items), Along with the period of lower than planned growth due to disruption related to the fire this gave rise to misperceptions about our growth capability among analysts and investors who were not aware of the fire incident, and misconceptions about our profitability.

As was evident in the results this past quarter- our financial performance puts NRB Bearings amongst the strongest performers within the auto component and bearing industry now that their events are behind us.

When the Q1 results of FY26 were announced and the exceptional items were no longer clouding the results, our strong performance became more evident. In the first quarter, standalone revenue rose 10% to ₹279 crore, the net profit rose by an impressive 50.1 percent to Rs. 26 crores, and EBITDA grew over 40%. On a consolidated level, we achieved an EBITDA of Rs. 61.4 crore on revenues of Rs. 310 crore, driven by strong domestic demand and expanding global markets. These numbers tell our story.

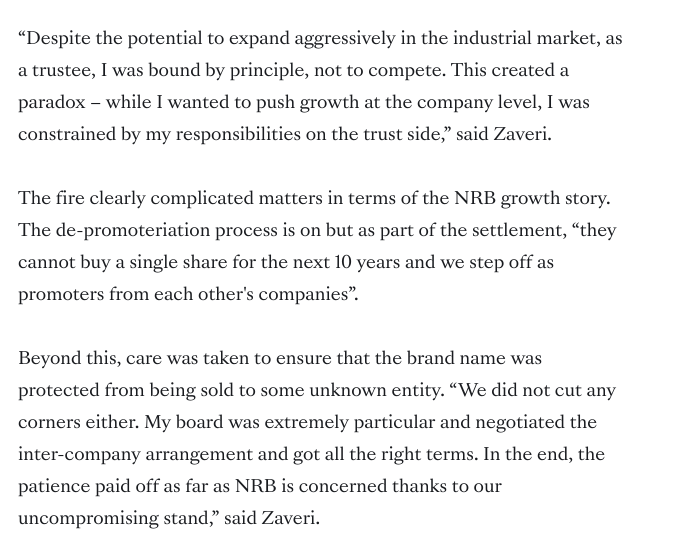

For decades, NRB has been the leader in the manufacture of needle roller bearings and cylindrical bearings in India. We were once the widest range manufacturer of bearings in the country and post the settlement and the inter-company arrangement, we are step by step moving closer to regaining that space, building capacities moving to a growth trajectory beyond the 10-12 % we have today.

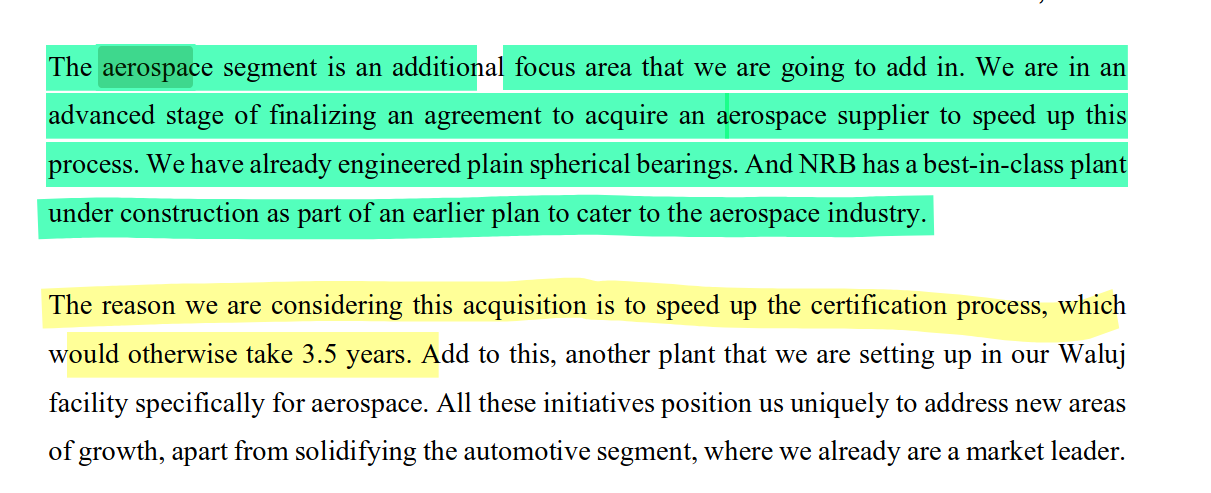

To support this the Board has approved a Rs. 200 crore capacity expansion. This will not only scale up our cylindrical, needle, taper roller bearing and ball bearing capacities, even more importantly, it will expand the size range we manufacture, enabling us to enter new hitherto un-addressed applications and add more business at existing customers in unpenetrated segments- construction and off-highway, electric grid, HVAC, defence and aerospace ; all this whilst growing aggressively in the mobility space in India and overseas. This diversification of sector and geography, customers, and technologies is the ultimate risk mitigator and growth engine.

In the mobility segments, we continue to be a technology leader. The proof lies in our order book. We have secured orders for the production life cycle of a vehicle, what is known as ‘lifetime nominated business’, worth over ₹600 crore from global Tier-1 and OEMs. This includes new launches for advanced hybrid and EV platforms from BMW, Renault, Stellantis, and Mercedes-Benz as well as the prestigious electric three-wheeler program for Stellantis. These nominations are the result of our black box design capabilities and R&D, prowess and competitive manufacturing capabilities. Our products already power the next-generation E Drive of Mercedes-Benz for the EQC & EQA platform for all Electric & Premium cars, along with a wide range of BMW models- the 1,2, 3 Series and X1, X2, the Ford F Line pickup truck, and latest models of Hyundai, Kia Motors, Jeep, Foton, Daimler and Paccar trucks…

Our products power more than 90% of vehicles on Indian roads, but our horizons extend far beyond. I am proud to say, in the domestic market, customers we have been supported by include Maruti Suzuki and Hyundai Group, both, by Tata motors, Mahindra, VECV and Ashok Leyland . In the two-wheeler industry we hold the premier position thanks to Hero, Honda, Bajaj, Suzuki and TVS. Our global customer partnerships include, Mercedes, Volvo, Magna, ZF, Daimler, BorgWarner, Dana, Hyundai Group, Mazda and Stellantis to name a few

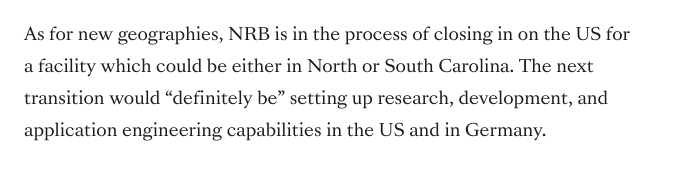

Our current overseas footprint contributes 25% of our total revenue. A proof of how sticky our customers are, and our unique competitive advantage is that our customers cannot easily replace us, no matter how complex the world and tariff situation; in any case, US market for us is only 4.5% of our total sales and today and have very limited exposure there.

We are now in the process of formulating a high growth strategy to follow our international customers with a strong global manufacturing footprint. This is part our aggressive growth plan to diversify geographically, add new products and serve new segments riding on our R&D and our application engineering presence in Europe and the US, close to the heart of global innovation. Our Thailand facility has already demonstrated how NRB can succeed in diverse geographies. It is one of our most efficient plants, and its strategic location has helped us win marquee Japanese and Korean customers. Thailand is not an assembly operation – unlike many auto component and bearing companies, NRB decided to manufacture components based on a local manufacturing program.

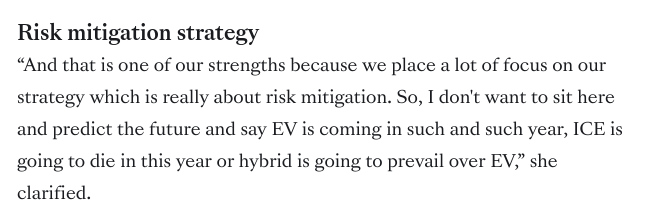

The world of mobility is in the midst of unprecedented transformation. ICE, hybrids, and EVs are all coexisting in a complex ecosystem. There is still widespread speculation on which technology will dominate. But NRB’s strategy is clear: to remain technology-agnostic. And deeply entrenched. Whether in electronic steering systems, e-axles, or next-generation transmissions, our aim is to ensure our products remain indispensable across platforms, irrespective of whether ICE, hybrid or EV will prevail our products co-exist in all and further we dominate in applications that are identical across all three for cars and truck applications. Additionally, no single customer is more than 10% of our sales, and the top 10 customers comprise 50 %- Overall, we have an exceedingly risk–mitigated approach.

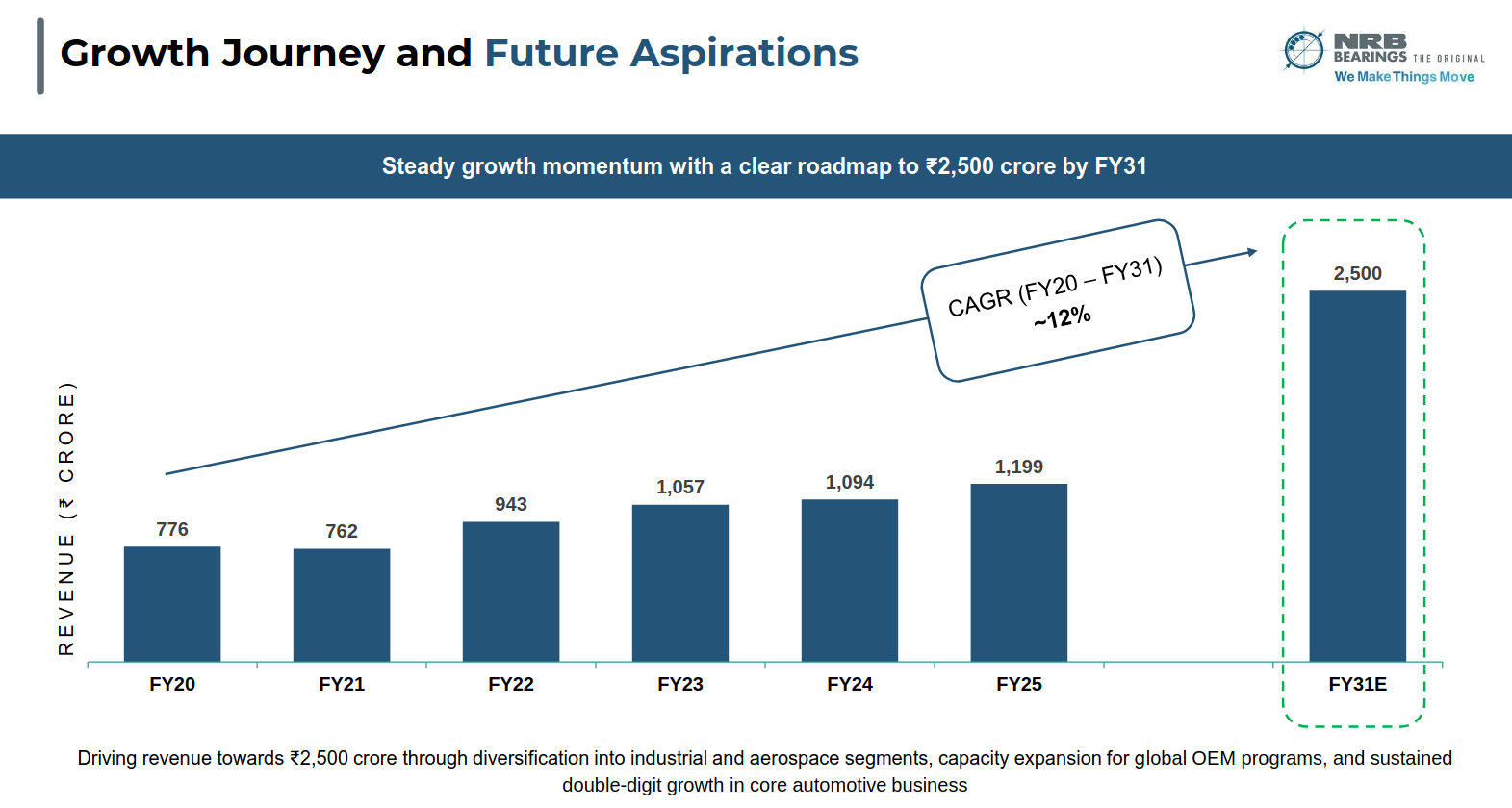

Shareholders, the challenges of the past two years are behind us, and we face the future with confidence. It is a future being reshaped by new supply chains, new technologies, and India’s rise as a global manufacturing hub. Singly and in aggregate, they all favour NRB- no technology transition can displace NRB. In fact as our lifetime nomination and its growth shows we are benefitting from this trend. Along with our plans for sustained growth as we have showcased the past two quarters, we are well on track towards our aspirational vision of 2500 crores in 2030, with enviable EBITDA margins that make us stand out within the auto component sector. Add to that our prudent financial management. Our AA-Stable Crisil Rating and financial ratios reaffirm this. And even after this capex, our debt-equity ratio will remain at our historically conservative levels, giving us the opportunity to keep investing as opportunities arise.

I believe the 2025 GST reforms mark a transformative moment for India’s manufacturing landscape, and NRB Bearings is perfectly positioned to capitalise on this. The move to keep just two tax slabs 5 percent and 18 percent combined with streamlined compliance, is a game changer. Within our industry, NRB should be one of the major beneficiaries of the GST rate cuts. 40% of NRB’s total revenue came from the tractor and 2-wheeler industry put together. We are already noticing a demand surge in our order book for the next quarter. The kick-off of our capex expansion this quarter seems well timed and we are working on speeding up augmentation of capacities in those products for which we are seeing a demand uptick.

With that, I would like to thank you all, dear shareholders for the for your unstinting support and the confidence reposed in NRB for which we remain grateful and assure that the leadership and employees of NRB are on the right trajectory for profitable growth.

Thank you

8 Likes

Concall Transcript:

1 Like

ICICI results update.

It looks NRB is entering into aerospace space (bearings used in aerospace) and is looking to accquire a company in the same field.

From concall.

concall was very insightful and was conducted for the very first time.

- 200 Cr capex planned till FY28 and 350Cr from there on

- Enough reserves for capex (and is required enough land bank available at book value)

- Expecting 2500Cr sales by FY31 with margin of 20%

- Going farward inventory will be reduced (the sudden increase in inventory was due to the fire in Waluj which caused to procure more inventory to keep the supply chain smooth).

- Looks like mindset of promoters changing from conservative to growth.* Talked about the family settlement among the promoters.

- Looks the promoters are talking now about growth

From inv ppt:

Disc: Invested.

4 Likes

Would it be wrong to say that a near term trigger for NRB could be a reduction in promoter shares pledging? Here is a link regards to a restructuring of the pledge. So, percentage of pledged shares stays the same?

I feel the promoter pledge is due to the recent settlement among family members. I believe pledge is not really a concern for the rerating. New initiatives, entry into industrial bearings, aerospace, capex could be trigger for rerating.

Came across this good blog.

4 Likes

1 Like