Hello,

I have been reading VP a lot lately. Amazing forum. Thanks @Ansh_Gupta for introducing me to this wonderful platform.

I am very new to value investing and this is my first analysis of a company. Please help me out if I go wrong/vague somewhere.

This is my take on the company:-

Company Background-

- · 27 years old company, family run paper manufacturing business. 5 units across Gujarat. Promoter- Mr R. N. Agarwal.

- · Business Type- Mainly B2B, Recently entered B2C with copier paper

- · Product portfolio-

-

- Writing and Printing Paper- 46%

-

- Duplex Board- 45%

-

- Newsprint- 9%

- · 5 units:

-

- Unit 1- 8000 TPM (Duplex Board)

-

- Unit 2- 5500 TPM (W&P Paper)

-

- Unit 3- 3500 TPM (Duplex Board)

-

- Unit 4- 3500 TPM (Duplex Board)

-

- Unit 5- 9000 TPM (W&P Paper)

- Sales: 85% Domestic, 15% export

- Overall capacity- 3,54,000 TPA

Elevator Pitch-

· 27 yr old paper company, mainly B2B, cyclical, good numbers for the past 3 years.

· Pricing wise seems undervalued w.r.t. industry and market

· Growth potential and capex plans to increase capacity, plans for becoming debt free

· Company moving towards more profitable product segments and exiting declining newspaper industry

-

Positives-

o Long term growth potential due to undervaluation and increasing demand of paper as a packaging substitute.

o Recent increase in promoter shareholding -

Immediate negative triggers include

o Increase in other current liabilities (Don’t know what the liabilities are and what will be the impact on the company)

o Covid-19 demand slowdown

o Raw Materials cycle turning around

Industry Trends-

- Growing demand of paper. Domestic paper demand grew at a CAGR of 6.3% from 2008 to 2018 owing to rising literacy rates, ecommerce book, reduced demand of single use plastic for packaging.

- Under penetrated market as compared to developed countries. FY 18-19 AR mentions per-capita consumption around 13 kgs in India as compared to a global average of 57 kgs.

- Capital intensive industry, making it difficult for new players to enter in this sector.

- Cyclical industry, raw material price fluctuations are difficult to pass on to the customers hence company bears the load.

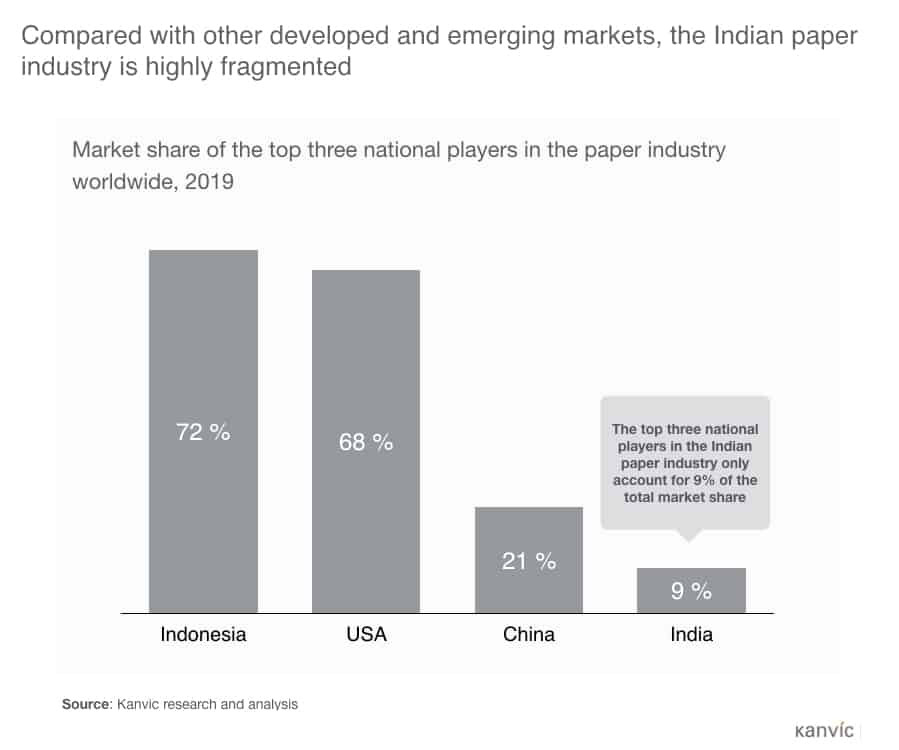

- Paper industry is expected to enter a consolidation phase. Don’t know how this will turn out but found this fact very interesting. Larger moat, cyclical nature can lead to consolidation and emergence of few top players instead of a segmented industry. (Source- Kanvic)

Business Attractiveness (Qualitative)-

-

- Recent switch from Newsprint to Writing and Printing paper. Moving away from fading newspaper segment towards a growing product segment.

-

- Company according to FY 18-19 Annual report expects to be debt-free by 2023-24. (Might get changed/extended due to Covid-19 impact). Long term borrowing reducing every year.

-

- Company focused on increasing operational efficiency (see numbers below) to gain competitive moat.

-

- Company planning to expand the Duplex Board segment from 1,80,000 TPA to 3,30,000 TPA (+ 83%) by 2022-23. (Rationale Given- “ High demand in western region, plastic ban, growing export demand)

Business Attractiveness (Quantitative)-

Trends-

| 5 yrs | 3 yrs | 1 yr | |

|---|---|---|---|

| Sales Growth | 14% | 10% | 6.60% |

| PAT Growth | 33% | 23% | |

| OPM | 13% | 14.30% | 15.40% |

| P/E Ratio | 4.91 | 4.64 | 3.30 |

Sales growth has been stagnant, however Operating margins have improved over the years. Still okayish. Company is planning to increase capacity over the next few years.

Operational Performance-

| 2018 | 2019 | 2020 | |

|---|---|---|---|

| EPS | 53 | 56 | 69 |

| RoCE | 27% | 27% | 33% |

| RoE | 41.13% | 30.30% | 27.88% |

| RoA | 13% | 12% | 13% |

| Current Ratio | 1.12 | 1.31 | 1 |

| D/E Ratio | 1.32 | 0.95 | 0.41 |

| Operating Cash Flow | 104.12 | 112.18 | 191.45 |

| Free Cash Flow | 54.48 | 22.53 | 114.49 |

| Gross Margin | 41% | 41% | 44% |

| OPM | 13% | 14% | 15% |

| NPM | 7.58% | 7.18% | 8.31% |

· EPS is increasing steadily

· RoCE is good (>25%)

· ROE is good

· Current Ratio is reducing which is not a good sign. (If someone can shed some more light here not able to understand this properly)

· D/E ratio reducing steadily

· Healthy cash flow

· Net profit margin unchanged but positive

Valuation-

| Market Cap (in cr) | 386.08 |

|---|---|

| P/BV | 0.92 |

| P/E | 3.31 |

| Industry P/E | 10.87 |

| EV/EBDITA | 2.43 |

Performed a quick DCF. Presenting the results below

| 3 yr Avg FCF | 54 |

|---|---|

| FCF Growth rate for first 5 years | 6.6% |

| FCF Growth rate for last 5 years | 5.0% |

| Terminal Growth Rate | 3.0% |

| Discount Rate | 12.0% |

| Year | Cash flow | NPV |

|---|---|---|

| 1 | 57.6 | 51.4 |

| 2 | 61.4 | 48.9 |

| 3 | 65.4 | 46.6 |

| 4 | 69.7 | 44.3 |

| 5 | 74.3 | 42.2 |

| 6 | 78.0 | 39.5 |

| 7 | 82.0 | 37.1 |

| 8 | 86.0 | 34.8 |

| 9 | 90.4 | 32.6 |

| 10 | 94.9 | 30.5 |

| Terminal Year | 10.0 | |

| Terminal Value | 1085.7 | |

| PV of Terminal Value | 349.6 |

| Total PV of cash flow | 757.4 |

|---|---|

| Total Debt | 173.0 |

| Cash & Cash Balance | 5.7 |

| Net Debt | 167.3 |

| Share Capital | 17.02 crores |

| Face Value (INR) | 10.0 |

| Number of Shares | 17020000.0 |

| Intrinsic Share Price | 346.7 |

| Margin of Safety | 30% |

| Lower Intrinsic value | 242.71 |

| Upper Intrinsic value | 450.75 |

Taking a 30% margin of safety, this stock still seems undervalued.

(This is my first DCF, please let me know how I can improve DCF analysis)

Competition-

| Name | Mkt Cap (in cr) | P/E | ROE | EV/EBIDTA |

|---|---|---|---|---|

| N R Agarwal | 386 | 3.31 | 32% | 2.43 |

| JK Paper | 1730 | 4.92 | 20% | 4.23 |

| West Coast Paper | 1264 | 3.41 | 30% | 2.56 |

| Andhra Paper | 897 | 6.84 | 24% | 3.81 |

| T N Newsprint | 869 | 25.6 | 8% | 5.37 |

| Century Textiles | 3751 | 10.84 | 13% | 9.59 |

· P/E is way below industry average.

· RoE slightly better than industry.

· EV/EBDITA is low because of the fall during Covid-19 Lockdown.

Challenges-

- Cyclical stock, raw material price increase can hamper operating margins.

- Lack of demand due to Covid-19 (Company recently stopped operations (temporary) in Unit 2 due to lack or orders)

- Digital Transformation will reduce use of paper for office use as manual work will be shifted to computers.

My Take-

- Company has progressed nicely in the last 3-4 years. However, raw material prices will dictate the profit margins of the company.

- Covid impact has been huge on the company and the company is expecting a bad quarter, also had to shut down one unit temporarily.

- Long term wise it looks good especially beacause company looks undervalued in the market and company also has plans to increase Duplex Board capacity becuase of growing demand.

(Since this is my first attempt, there might be some mistakes or vague conclusions. Please let me know I will rectify them, it will be a learning experience for me. It would be great if people reading this can also give me suggestions on how to improve in the future, what other parameters to look at and how to understand the numbers from a long term perspective. Open to all suggestions/feedbacks.)