While the usual issues associated with government owned businesses such as slow decision-making, bureaucratic interference, etc. are all applicable to NMDC as well, there is another side to all the negativity and criticism.

There seems to be quite a bit of misconception regarding NMDC’s Nagarnar Steel Plant. The project has been criticized for being highly delayed. But it is not an easy project to build. If memory serves me right, the last greenfield project successfully commissioned in India was the 6 MTPA plant of Jindal Steel & Power in Angul Odisha way back in 2013.

To the best of my knowledge, not a single greenfield steel plant of any meaningful size has come up in India even from the private & public sector in the last decade. Even POSCO Steel, Korea has struggled for years. Arcelor Mittal had to buy out Essar Steel to enter the Indian market.

Firstly, the entire plant is being constructed in an area called Jagdalpur in Bastar district, which happens to be in the heart of the Naxalite zone with negligible infrastructure and rail / road connectivity in the surrounding region.

Secondly, this is an integrated iron and steel plant, which includes conversion of iron ore to iron to raw steel to hot rolled steel and finally to specialized steels. This project includes a power plant to supply at least 40% of the total power requirement of the plant, an internal railway line, plus a large township complex. For more details on the size and scope of the project, you can refer the environment clearance report from 2014:

Q.1 Why construct the steel plant if the location is so difficult then?

Primarily, three reasons:

- Large Indian Steel OEMs like JSW are doing backward integration by getting into mining operations. Naturally, if your large customers are increasingly investing in backward integration with captive mineral supplies, then as a mining operator NMDC will be compelled to plan for forward integration to secure consumers of their iron ore.

- NMDC is a highly cash rich PSU. All the investments in the steel plant have come from internal accruals.

- Access to high quality iron ore from NMDC mines in Chhattisgarh in the neighbouring Dantewada district.

In general, iron ore is of different grades:

- Magnetite: 70-75% concentration of Iron (Fe)

- Haematite: 60-70% concentration of Iron (Fe)

- Limonite: 40-60% concentration of Iron (Fe)

- Siderite: 40-50% concentration of Iron (not worth mining)

Please refer NMDC Annual Report 2021, Page 8:

- Baila ROM: 10 mm to 150 mm size with Fe 65.5%

- Baila lump: 6.3 mm to 40 mm size with Fe 65.5%

- DR CLO: 10 mm to 40 mm size with Fe 67%

- 10-20 mm Baila Sized Lump: 10-20 mm with Fe 65.5%

- Baila Fine: -10mm with Fe 64%

- Doni lump: 6.3 mm to 31.5 mm size with Fe 65%

- Kumaraswamy Lump: 6.3 mm to 31.5 mm size with Fe 64.5%

- 10-20 mm sized Kumaraswamy Lump: 6.3 mm to 31.5 mm size with Fe 64.5%

- Doni Fines: - 10 mm with Fe 64%

- Kumaraswamy Fine: -10 mm with Fe 64%

As can be seen, most of their iron ore is of high quality in both Chhattisgarh and Karnataka.

Usually, people would associate mining with digging deep in underground tunnels. However, most of NMDC’s mines are open-cast (Refer the image on page 10 of Annual Report 2021).

A combination of high-quality iron ore accessible above the surface level makes mining a lot easier and cheaper as compared to extracting minerals from rocks deep below the surface, which gives NMDC a major cost advantage.

Q.2 Is this cost advantage sustainable?

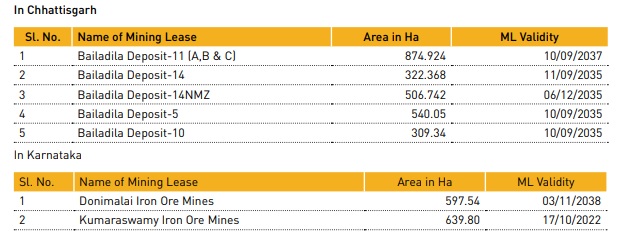

Please refer Annual Report 2022, Page 35: NMDC has mining licenses for most of their mines till 2035-2037. Therefore, this advantage may be sustainable for a long period of time.

Q.3 How are the raw material supplies be secured if the Mining and Steel businesses demerge?

Annual Report 2022, Page 24: Shared Assets

NMDC and NSL shall enter into shared services agreements and long-term supply agreement, as may be necessary, on terms and conditions that may be agreed between NMDC and NSL and on payment of consideration on an arm’s length basis and which is in the ordinary course of business.

Q.4 How has NMDC constructed this project without any know-how on setting up a steel plant?

The complete project consultancy, plant design, evaluation of suppliers and tenders, inspection and supervision of commissioning has been outsourced to MECON Limited. MECON is another PSU under the Steel Ministry and has been primarily responsible for setting up and modernization of almost all the steel plants of SAIL – Durgapur, Burnpur, Rourkela, Bokaro, Bhilai as well as RVNL and RINL.

In simple words, NMDC spends the money, but MECON is the technical brains and decision maker behind the project. And MECON has more than enough experience in setting up steel plants of all kinds in India.

Unlike some of the private sector companies which have bought Chinese equipment, NMDC’s Nagarnar Steel Plant has a lot of equipment from Tier-1 European OEMs like SMS Group (Germany), Danieli (Italy) and Primetals (Mitsubishi-Siemens). Many of their auxiliary packages have been set up by Tier-1 EPC contractors like L&T (Eg. Water Treatment Plant) and Tata Projects (Eg. Blast Furnace).

Q.5 Does this Iron & Steel Plant have any meaningful functional value?

While the project has definitely gotten delayed which has increased the cost beyond their original target cost, a new plant constructed by Tier-1 companies is definitely valuable. Since this project has been funded mainly from internal accruals, interest cost burden isn’t very high.

The total project is spread over 1980 acres, which leaves enough land for brownfield expansion in future to upgrade from 3MT to 5-6MT capacity. Any future expansion will be a lot easier as most of the utilities such as roads, township, etc. are already built. Jagdalpur now also has an airport with a daily flight from both Hyderabad and Raipur.

Q.6 Valuation:

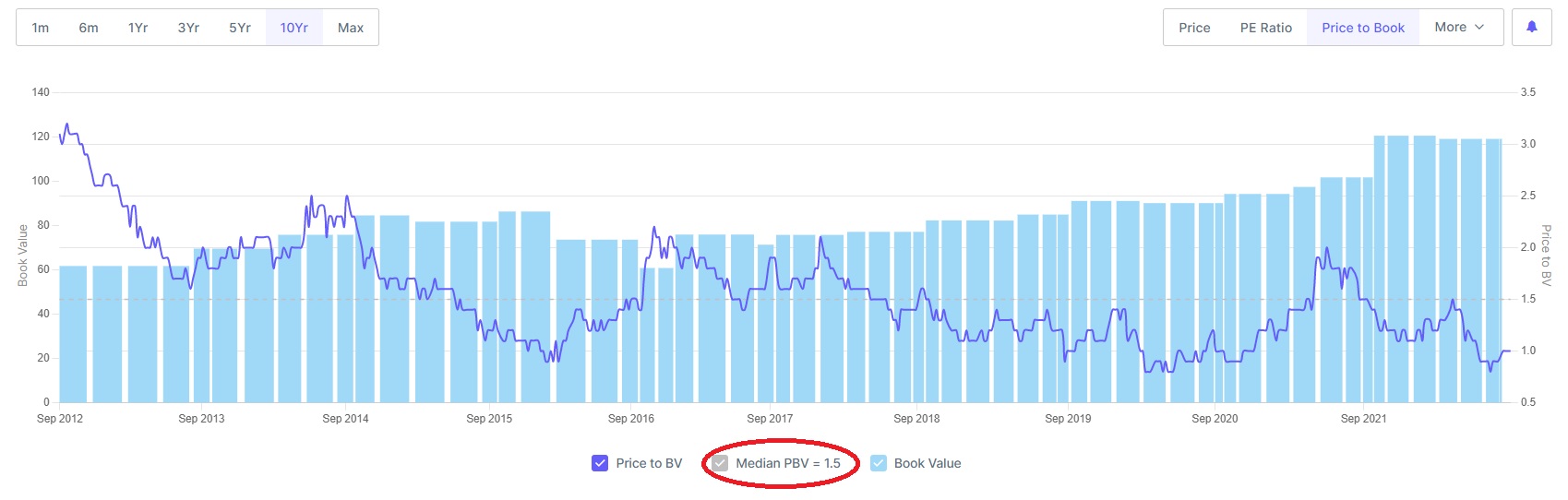

NMDC’s 10-year median Price to Book value is 1.5 (Source: screener.in). Currently it is at P/B = 1. This P/B ratio is based on NMDC’s March 2022 balance sheet where their fixed assets are Rs. 3,966 crores. The complete investment in the steel plant is shown in CWIP (Capital Work in Progress) of Rs. 18,300 crores. At some point, this Steel Plant will eventually be completed and commissioned. So, this Rs. 18,300 crores will be added to the gross block of Rs. 3,966 crores (less depreciation). Even if the P/B remains at 1, which is at a 33% discount to its long run average, it represents is a significant upside to CMP of approx. 125.

Since the demerger is going to result in a mirroring of shareholder pattern, I haven’t gone into the separate valuation of the two demerged businesses.

Disc: Biased

- Invested in NMDC since over 1 year

- Vendor to NMDC Nagarnar Project for plant & machinery, with regular onsite visits by my team at site for machinery installation