Will Amaraja Batteries be benefited?

@Shashank_Mohan From the likes of consumer & B2B facing items such as batteries etc will benefit however not to a extent that they will keep on going forever.

There will be exhaustion and intense competition among the players (i.e. peers).

Yatra Business : Key focused on delivering OTA (Online Travel Agent) to the B2B (business to business which includes business to enterprise and business to agents) & B2C business

- Opportunity Size

- Key Points

- Moat

- Process

- Management Track

- Outlook

Opportunity Size:

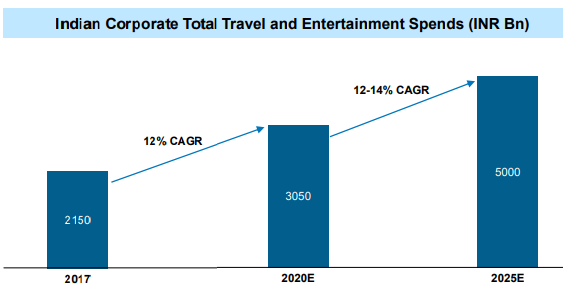

1. DHRP/IBREF/CRISIL Industry Report :

a. By 2028 India Tourism is projected to reach 4540-4560 billion

b. By 2028 online travel market in India is projected to reach US$ 3335 billion (Yatra DHRP)

c. Tourism is the third largest foreign exchange earner for the country.

d. B2B Market expected to grow at 2x the overall travel market and approximately double over the next 5 years driven by:

![]() GDP growth: IMF projects 6.8% growth in GDP for India in 2023, implying higher business activity, and related travel

GDP growth: IMF projects 6.8% growth in GDP for India in 2023, implying higher business activity, and related travel

![]() GST implementation: ~10 Mn companies in India with registered GSTIN - greater scope for organized TMCs

GST implementation: ~10 Mn companies in India with registered GSTIN - greater scope for organized TMCs

![]() Growth in MICE: High margin (~20%) & high demand frequency; expected growth in off-sites, dealer meets

Growth in MICE: High margin (~20%) & high demand frequency; expected growth in off-sites, dealer meets

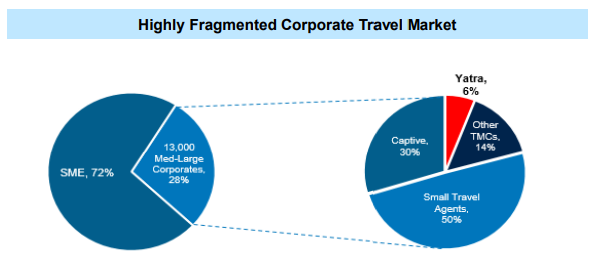

Highly fragmented market shifting towards online & organized segment

![]() Extremely fragmented and a large population of corporates are handled in an analog, inefficient manner with no digitization

Extremely fragmented and a large population of corporates are handled in an analog, inefficient manner with no digitization

![]() Top 13k companies account for 28% of volume

Top 13k companies account for 28% of volume

![]() Yatra is the largest player with 6% share of the 13,000 Mid-Large Enterprises

Yatra is the largest player with 6% share of the 13,000 Mid-Large Enterprises

![]() Travel does tend to be closely linked to the growth in GDP and over the past decade, travel has been growing anywhere between 1.5x to 2x of GDP growth so the travel industry growth would be 6.0% or more

Travel does tend to be closely linked to the growth in GDP and over the past decade, travel has been growing anywhere between 1.5x to 2x of GDP growth so the travel industry growth would be 6.0% or more

YATRA Business

a. B2B (Business to Business which includes business to enterprise and business to agents)

b. B2C (Business to Consumer)

c. Forex - Aiming to get Forex License

d. Visa

e. Activities

f. Travel Insurance

g. Monument/Cultural/Heritage visit

Key Points :

Yatra is more oriented to the corporate business side as they are PAAS which are more likely platform solutions that helps corporates to easily integrate yatra platform to their ERP systems and HRMS systems that can smoothen out the billing and expense process along with it they have associated controls to define on what the employee can opt example business class, Economy class…

Yatra has merged along with Ebix to cross sell insurance and financial items such as Ecash or other wallet, forex etc

They are planning to explore more avenues with help of ebix into markets like Europe, US and prominently become a best travel OTA partner

They are also planning for forex license

Rate gain is one of their client that helps in price management whether it’s hotels, airline etc which gives yatra a sense of what the demand is and what the price predictability is and how they can go about pricing

Yatra business was not doing well at B2C main reason was because of funds

Yatra is doing perfectly well at the corporate end and had about 813 large corporate customers and over 49,800 registered SME customers

Yatra ranks 3rd in India

Yatra has the highest tie up with Hotels & Accommodation at domestic market with about

a. 2,105,600 tie-ups, as of March 31, 2023 (Source: CRISIL Report)

Yatra has 29,800 agents in above 1,000 cities across India as of March 31, 2023

Business Strategy

1. Proprietary eCash loyalty program that enables travellers that book through the platform to accumulate and redeem points

2. The company currently have about 7 million eCash registered users on their platform.

3. The company first focus was to have a B2B corporate presence firstly then move to B2B - which is a very good move as they are not dependent on customer front only

4. They have forex partnership and provide forex to B2B only

5. They provide Outbound to Outbound to B2B only meaning China - Hongkong

6. Majority of the travel is Inbound to Outbound meaning - India to US or elsewhere

7. IT/ITES : Contribute to 10% topline growth

8. Corporate accounts carry a potential annual billing of about INR 813 million

9. Yatra has the largest number of hotel and accommodation tie-ups, with 2,105,600 tie-ups in March 31, 2023.

10. Currently 40% and 45% coming from B2B and about 55% to 60% coming from B2C

11. Yatra has holiday advisories and agents who helps in delivering smooth customer experience

12. Recently they have announced Yatra Prime package for travellers to assist in all ways from airport to any site.

Share of market

• India 70%

• International 30%

• Domestic market our market share would be close to between 7% and 8%

• Growing at about 20% faster rate than the industry

Risk

• Sales promotion expenses

• Customer promotions and loyalty program costs

• Payment expenses

• Overall TTV increment

• Cost cutting exercises which you they planning in the next 6 months apart from the savings and finance cost

• Credit cards would be the highest cost

• ESOP cost in quarter 3, 2024

• Cost for selling shareholders for the OFS component

• Cost knocked off against share premium

3 Likes

My 2 cents : My thoughts, not to criticize anyone and open to constructive criticism

- Everyone is bullish on RENEWABLES

- Everyone is bullish on EV

- Everyone is bullish on POWER

What people are missing here?

BATTERIES

The most important criteria for everything.

This point is stressed in Indian Parliament and today in Vibrant Gujarat

- India Targets for 50 GW by 2030 for EV.

- Battery Production will start on February 2024. PLI ACC Scheme will kick in…

- They did mention this WITHOUT BATTERY NO FORWARD MOVEMENT ON AUTO FOR EV…

- The government will reduce cost of EV and full focus on building EV eco system here in India.

- All the imports they will Ban as they will source out Lithium from Jammu and research is going on ALUMINIUM ION Battery, SODIUM ION Battery in IIT…

Future plans :

- 4 lakh crore export

- 12 lakh crore industry

- Maximum part of revenue to GST and state government

- AUTO will be number 1 in the world

Researching about

- Sodium ION

- Aluminum ION

7 Likes

Agree with the thought .

I had taken an initial smll position in Amara Raja for the same ( which now i sold off for small gains) with the same thoughtd.

However, whne scratching the surface , i realised/ interpreted that there is a long way to actually arrive at tangible outputs as the players maybe subject to intense competition amidst their own capabilities juxtaposed with midway challenges in form of upcoming research which may sway the flavour in batteries which would get adopted by the time thier plants are commissioned.

Secondly, there seems to be this race between the cleaner energy fuel types in terms of green hydrogen, EV or ethanol based fuels; ie which ones would hit the trigger faster( given research is on all such directions) .

Agreed as of now EV is the theme dominant, but as globally sales of EV seem to be getting impacted as per recent reports, i feel this also is a consideration.

I dunno if what i wrote makes sense , but thought of putting it for review to learn about the topic.

1 Like

@harmeet_kumar Great

As I was reading a article it said that China just met its 50% renewable energy

Coal accounted for 56.2% of total energy consumption last year, versus 25.9% from renewables which includes nuclear energy, the NBS data showed.

China’s national renewable energy power installation will exceed 1.45 TW, with wind and solar power installations surpassing 1 TW

China is leading the global renewables market

China’s estimated installation is more than double the number of U.S. and Europe installations combined

China’s wind and solar project investment is expected to reach $140 billion for 2023

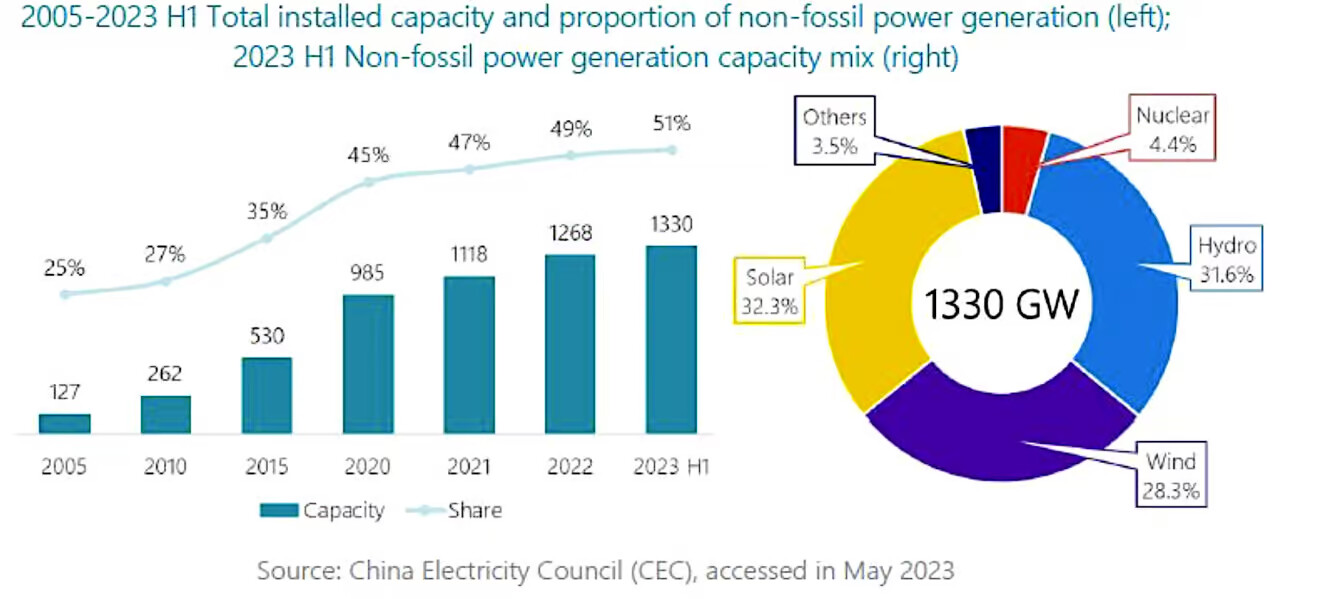

Coming to our end - As of Nov 2023, we have a combined installed capacity of 179.57 GW.

The following is the installed capacity for Renewables:

- Wind power: 44.5 GW

- Solar Power: 72.3 GW

- Biomass/Co-generation: 10.2 GW

- Small Hydro Power: 4.98 GW

- Waste To Energy: 0.57 GW

- Large Hydro: 46.88 GW

The main reason was because China invested 6.5% of GDP value approx. value to renewable

India spent about Rs 13.35 lakh crore (Rs 13.35 trillion) in 2021-22, just over 5.5% of its GDP, on climate adaptation and expects to incur another about Rs 57 lakh crore (Rs 57 trillion) over the next seven years for this purpose, New Delhi told the UN Framework for Climate Change Convention (UNFCCC).

So that concludes that they did spend a lot on Renewable & Real Estate wherein now the Real Estate had filed for Bankruptcy.

Now China is leading on Renewable and on another if you notice 50% of their power is met via Coal and all of their industries are sweating : that’s the major concern as the AQI is over and above 200

The next growth where all are hoping towards is on Sustainability, Eco Friendly and Green Chemistry.

My thoughts

- I think China is fastly improving its infra on renewable side to improvise on carbon footprint and then help industries tap onto lower cost of input such as utilize renewable power, reducing the manufacturing cost so on

- China has over half of the world’s lithium refining capacity but has to rely on imports for about two-thirds of the raw material.

https://www.mining.com/web/china-lithium-probe-puts-spotlight-on-reserves-and-esg-risks/

The advantage we have is low cost, sustainable future - as most of our industry are using green chemistry.

Now raw material is something that we need to source for which we had breakthrough in Iron-ion, Sodium-Ion - if this gets implemented, we will have a chance.

Now coming to your question.

See Amaraja, Exide, Panasonic, Eveready - all should do well : The main factor behind them all driving depends on the marketing and sales.

EV is rapidly catching up but Bio Diesal, Ethanol - all will have to wait because there is sugar shortage.

If you think Bio Fuel is sustainable - to a limit yes but also sugar degrades the soil and this inturn has its own complications.

I feel Sodium, Aluminum batteries, Bio Gas, Hydrogen - should all do well… its certainly not now.

2 Likes

Wow; Those are a lot of numbers to crunch!

What would be your data source for installed capacity for renewables?

Anyways i think there’s growth happening for renewable energy sector, the capacity infact grew by almost 14-15 percent in 2021-22 from the previous year; so definitely we are making progress

This i need some elaboration on

Yeah sounds right , as policy is also mostly geared towards EV currently, but so is/was the case with ethanol

And now aren’t we waiting for TESLA

I must confess i do not know the technicalities of those vehicles

Am not a deep learner, I study only at surface and if I feel the idea is worth it - then I do go for it.

Total digital payment transactions volume increases from 2,071 crore in FY 2017-18 to 13,462 crore in FY 2022-23 at a CAGR of 45 per cent: MoS Finance

Digital payments transactions reach 11,660 crore in current Financial year as on 11.12.2023

| Financial Year | Volume (in crore) |

|---|---|

| 2017-18 | 2,071 |

| 2018-19 | 3,134 |

| 2019-20 | 4,572 |

| 2020-21 | 5,554 |

| 2021-22 | 8,839 |

| 2022-23 | 13,462 |

| 2023-24 (Till 11th Dec) | 11,660 |

Credits :

- In 2017, UPI recorded a YoY growth of 900%, processing over 100 million transactions worth INR 67 billion.

- In 2018, the YoY growth was 246% with transactions worth over INR 1.5 trillion processed.

- In 2019, the YoY growth was 67% with transactions worth over INR 2.9 trillion processed.

- In 2020, UPI recorded an YoY growth of 63% with transactions worth over INR 4.3 trillion processed in December 2020.

- In 2021, the YoY growth was 72% with over 1.49 billion transactions worth INR 5.6 trillion processed in June 2021[5].

- At the end of the calendar year 2022, UPI’s total transaction value stood at INR 125.95 trillion, up 1.75 X year-on-year (YoY), as per the NPCI. Interestingly, the total UPI transaction value accounted for nearly 86% of India’s GDP in FY22[8].

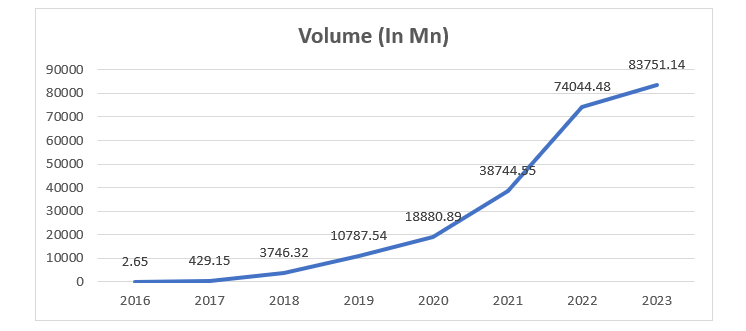

- At the end of the calendar year 2023, UPI’s total transaction volume stands on 83.75 Billion.

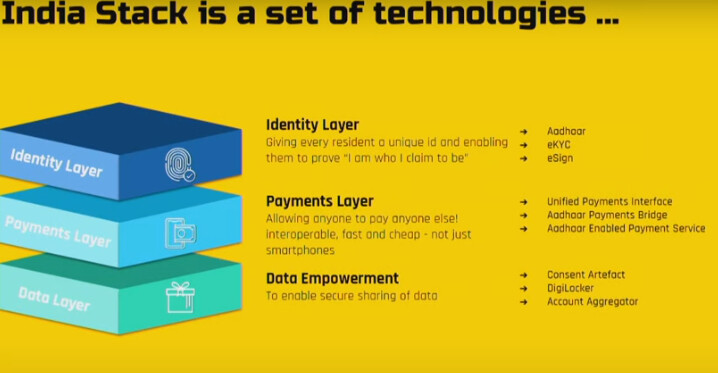

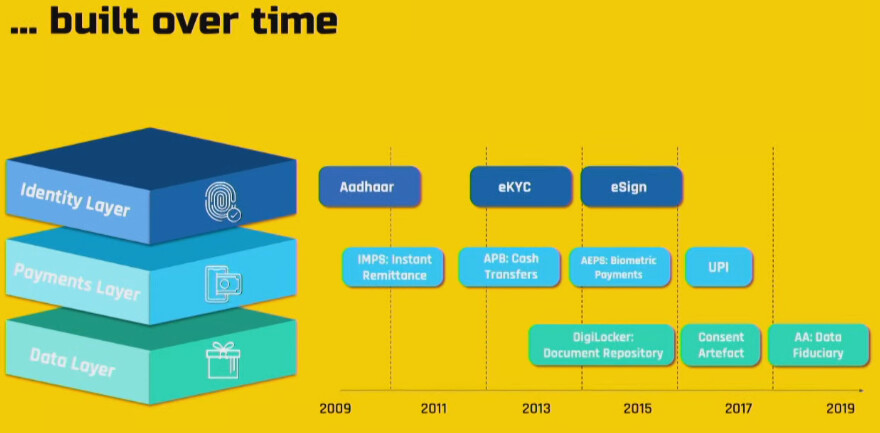

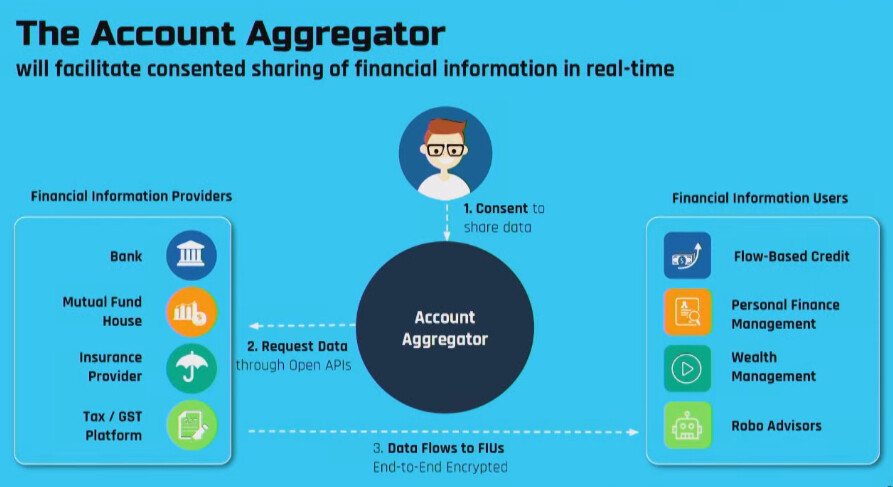

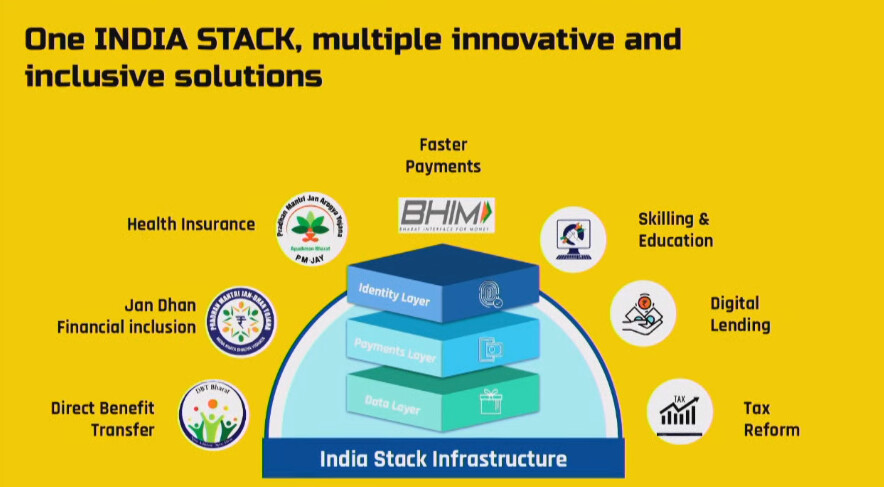

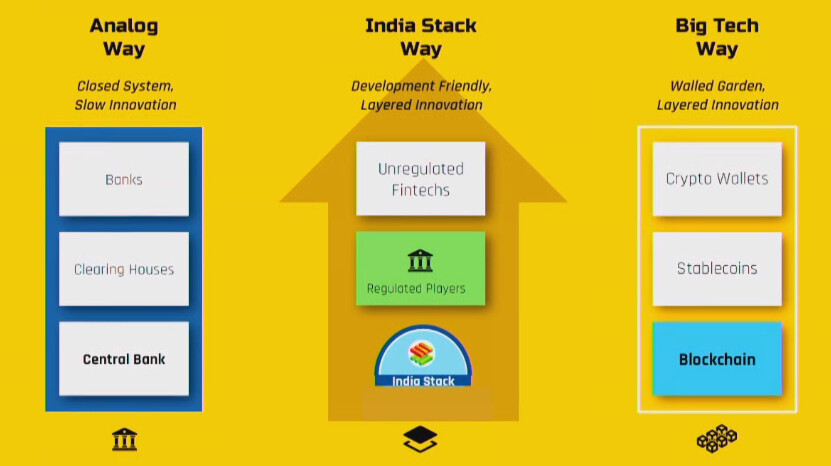

India is on a next leg of growth spurt - to account for this India has a Tech stack which is very well built and a brilliant way that has been put up.

Now lets understand what happened from 2009 till now

Credits : https://www.youtube.com/watch?v=8PLEZmJ36y4&t=233s - Brilliant work done by Nandan Nilekani (Infosys) - thanks to him that we are much far ahead coming to the digital revolution

Why am saying all this?

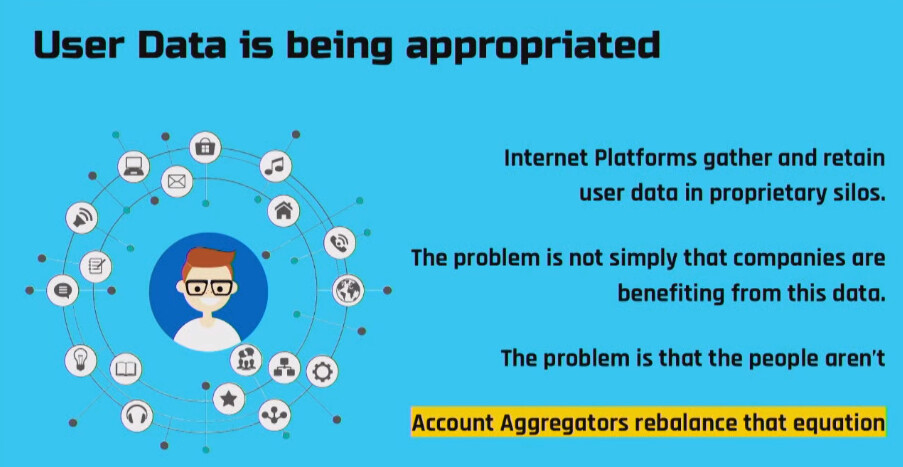

1, If you know that we have a vey robust and a structured way of growth : tomorrow if anyone needs a loan - he/she can get it in minutes, by first giving their consent to the banks to authorize his/her aadhaar - get all details with respect to the credit score, credit profile etc etc and get loan approved immediate and loan amount transferred to Bank account.

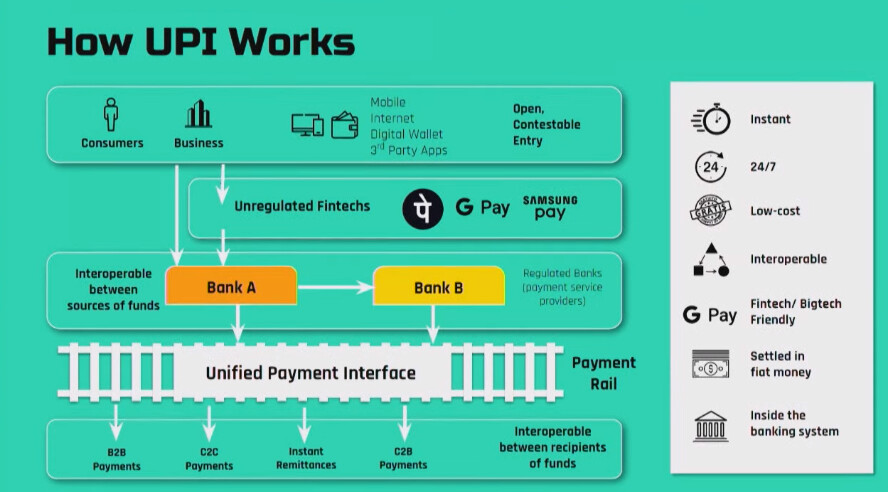

UPI has revolutionized the way that we work

Now more and more countries are planning to adopt the UPI system.

Everyone is talking about the consumer discretionary spending and so on and so forth.

From what I learned so far

- How much digital are we?

- What digital platforms that enables all these elements?

- Consumer Discretionary spending true but what platform? - ecommerce, merchant or elsewhere

- Which payment interface?

- What technology enables these?

If I consider Starbucks or Bigbasket

- Will you go out for coffee or would you like to shop from home

- What is the win win for both these parties here? - Its the payment interface

If payment interface then which?

- UPI

- Card

- Cash

- Online Web

Who are the companies that helps these?

- CC Avenuve

- Razorpay

- JustPay

- Paytm

- Phonepe

- Google Pay

Which area of basket they target

- Large Enterprise

- Medium

- Small

- Micro

One thing to note : No matter which way you go, the payment aggregators will benefit either if you shop from Starbucks on a weekends or Bigbasket on weekdays.

The business is cyclical but the payment need not be.-

Share your thoughts.

*

7 Likes

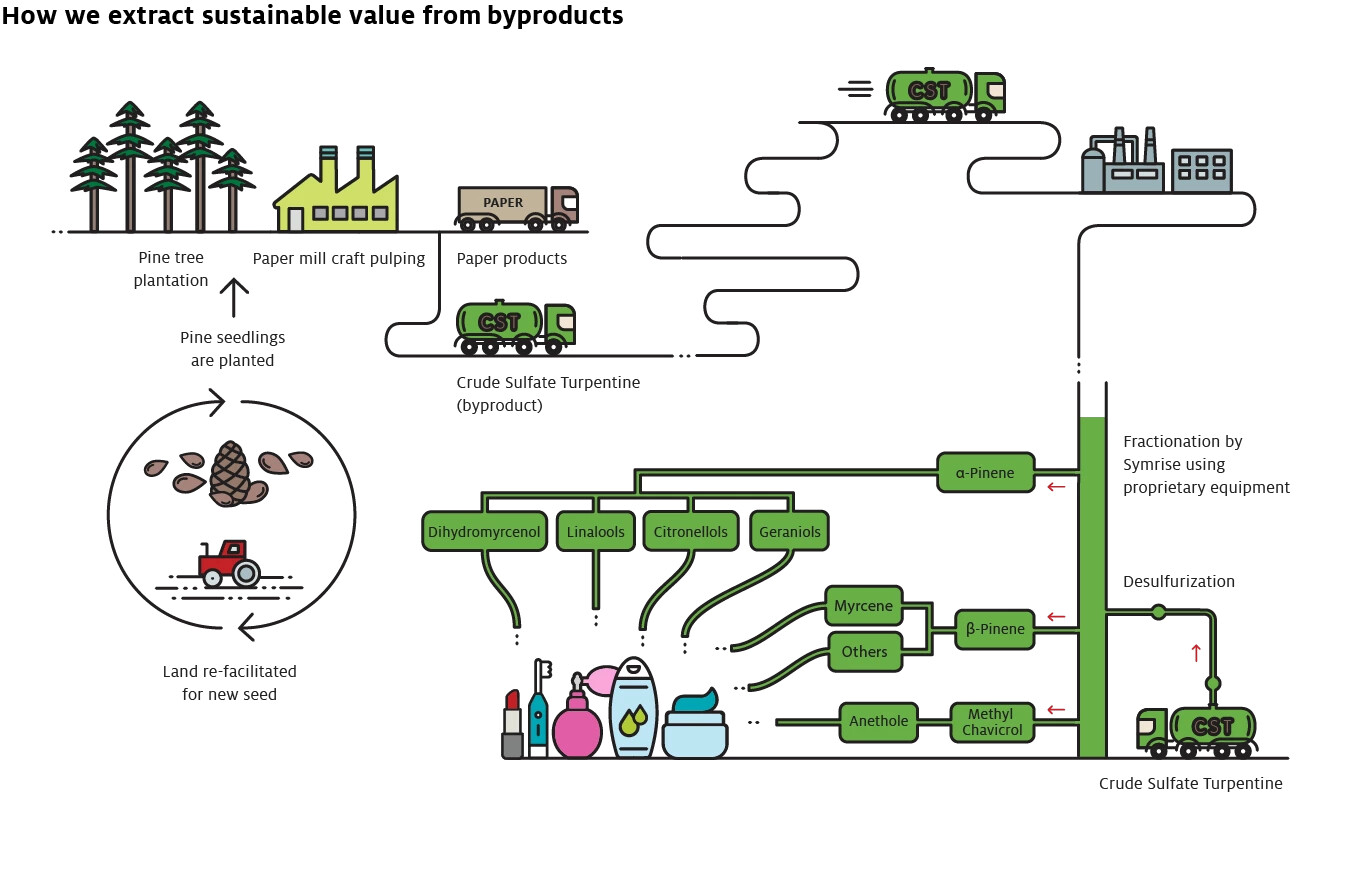

Privi Speciality :Privi Speciality Chemicals is India’s largest and one of the leading manufacturers of aroma and fragrance chemicals in the world.

- Opportunity Size

- Key Points

- Moat

- Process

- Management Track

- Outlook

Opportunity Size

Global Aroma Market

- USD 5.57 billion in 2022

- USD 8 billion by 2031

- CAGR of 4.1% during the forecast period (2024-2031).

Global Perfume Market

- USD 33.9 billion in 2022

- USD 35.12 billion in 2023

- USD 46.61 billion by 2031

- CAGR of 3.60% during the forecast period (2024-2031).

’

Total Addressable Market Size

| USD Billion | 2022 | 2031 | Total |

|---|---|---|---|

| Global Aroma Market | 5.57 | 8 | 13.57 |

| Global Fragrance Market | 33.9 | 46.61 | 80.51 |

| 94.08 |

Roughly 9400 crores INR.

Key Points

- PINENE - Process

Source : Green chemistry - Power and the possibilities - Symrise

- CITRAL - Process

Source : Green chemistry - Power and the possibilities - Symrise

-

MUSK - Process

-

PHENOL - Process

-

Overall Capacity as of 2024 : 48,000 metric tons per annum

-

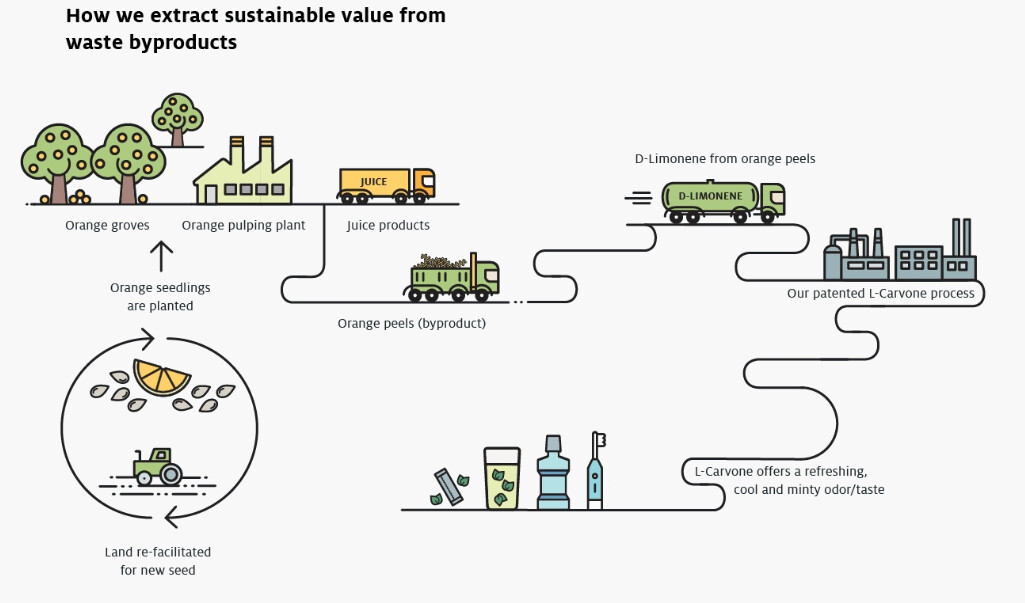

It has backward integration to use waste generated from pulp mills, the crude sulfate turpentine, the CST as it is called with a capacity of over 36,000 metric tons per annum

-

It is the only Company in the developing world and one of the four companies globally to have the technology and the logistics ability to procure these waste products from across the globe

-

It has the largest single CST processing site in the world

5.Manufacturing Facilities in Maharashtra and Gujarat

Kenneth Andrade’s Recent Interview

- Capital Goods & Capex Dominated stocks are trading to significant premium where any of the large consumers.

- 4 Pharma companies as top 10 holdings : World’s generic manufacturer and capex cycle is almost year, over the course of last 5 years the industry has cleaned up its balance sheet and they are net positive. The ability to generate significant amount of profitability from the existing capex. 2024-25 will be years where this industry will hit its all time high terms of profitability and cash flow generation. Growth + category leaders + balance sheet + favorable valuation.

- Banks & Finance : Kenneth doesn’t have them as he mentions its an historic trade - he chose to be on asset side and not on liability side.

- His Macro Trade/Directional trade would be capex and industrials

- Breadth of the non capex/industrial is narrowing significantly.

- He states that his bet is not on industries but on capex themes

- Global Cycle : Metals/Export/Pharma - Global GDP growth is held up by defense, industrial capex, Governments are going to be largest spenders, consumers are taking back seat due to inflation

- Government put their balance sheet to work on capex side on rebuilding the entire industry, they will have to generate cash (i.e. were the inflation cycle is sitting)

- Kenneth is favorable on commodity, defense.

- IT companies : Significant hiring done with expectation for growth - now cutting down the head counts. IT will be in static phase

- With respect to the power/railway or others - everything boils down to commodities - which can generate huge free cash flow (so he is more interested towards metals, steel, bearings)

- New age companies : Zomato/Paytm - he plans to buy on second cycle, waiting for market to mature and markets correct. - tracking radar.

- Consumer : The valuation is not favorable

- Chemical market is fairly stressed across globe especially agro chemicals

- Consumer space : Middle class is heavily stressed, household debt - consolidation will happen - tracking.

- EV/Energy Transition/Climate Change : Not participating will wait for second cycle

- Generic Pharma/Pharma is mapping to the entire IT cycle that the IT has been through since. Pharma is the lowest cost manufacturer, getting market share from international business, US companies (generic business are extremely leveraged), Balance sheet of Indian companies are in favor, Interest rate going up in US,

India has the physical capacity + Financial capacity = where US has got none.

5 Likes

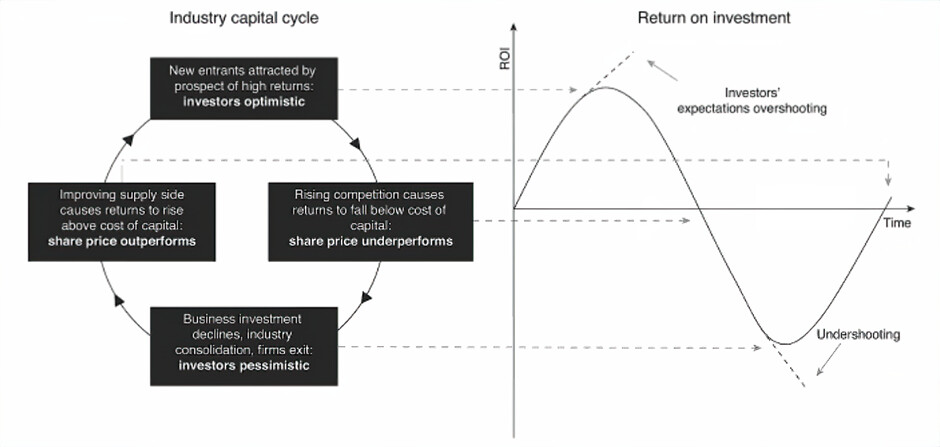

We are in the Business Investment Declines, Industry Consolidation, Firms Exit: Investor pessimistic phase for. (Phase iii)

- Pharma

- Chemicals

1 Like

My notes

Not all sectors are free to hide

If you see valuations of capital goods, power, infrastructure, psu, railway’s doesn’t give me any comfort to enter them…

Of course there are certain stocks that might do well but the big question here is

Will FII or DII buy such expensive companies?

They too will think and calculate the risks and upside left for the stock…

Of course if any HNI or DII/FII has bought this stock at a far very cheap price they would tend to average at some correction

But what about those who are waiting on sideline?

From sectors point of view I see

Auto

Chemical

Pharma

Are still normal to cheap level depending on each company.

Defense is a big opportunity however what are in defense

Drone

Anti Drone

Radar

Aerospace

These would do definitely well

5 Likes