Dear All,

I have gone through the NILE Limited. and this is my first post in value pickr. Please correct me if any mistakes. A brief description below,

Market Cap : 186.56 Cr

CMP : 621.85

Face Value : 10

P/E : 6.54

Nature of Industry:

Recycling of Lead, Power Generation through wind farms.

Industry Structure and Development:

Lead and Wind Energy are the two divisions of the Company.Pure Lead and Lead alloys are supplied to manufacturers of Lead acid batteries.Wind energy generated is sold to Andhra Pradesh Southern Power Distribution Company Limited.

The operational performance of the company during the fi nancial year 2016-17, which shows a signifi cant increase in turnover as well as profit.Result in brief

Particulars 2016-17 2015-16

Total Income (in lakhs) 58,005.71 42,784.86

Profi t Before Interest,

Depreciation & Tax 5,283.69 2,154.66

Profi t/ (Loss) Before Tax 4,020.11 1,127.68

Profi t/ (Loss) After Tax 2,623.07 706.45

Net worth 9,858.82 7,344.14

Dividend-Rupees per

share (%) Rs.3 (30%) Rs.3 (30%)

Operations:

Operations of the Company’s two divisions for the year under review were as follows:

Lead Division:

This year, the Lead division recorded sales of Rs.57,883 lakhs as against Rs.42,465 lakhs in the previous year, an increase of 36%.

Windmills:

The entire energy generated at Ramagiri was sold to Andhra Pradesh Sourthern Power Distribution Company Ltd. The total revenue was Rs.53 lakhs against Rs.62 lakhs in the previous year.

Total:

The combined turnover of the Company, thus, was Rs.57,936 lakhs for the year under review, as against Rs.42,527 lakhs for the previous year.

Please find annual report with below link.

http://www.bseindia.com/bseplus/AnnualReport/530129/5301290317.pdf

and the quarter results was good.

Looking for value pickr reviews and suggestions.

Disclaimer : Not Invested.

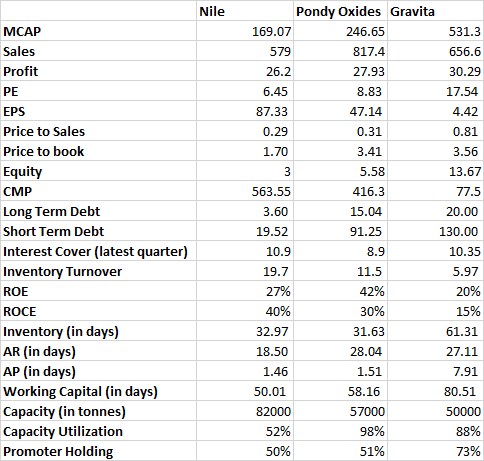

Nile Pondy Oxides Gravita

Nile Pondy Oxides Gravita