Current Market Cap: Rs 435 cr

CMP: Rs. 11.75

Background of the company:

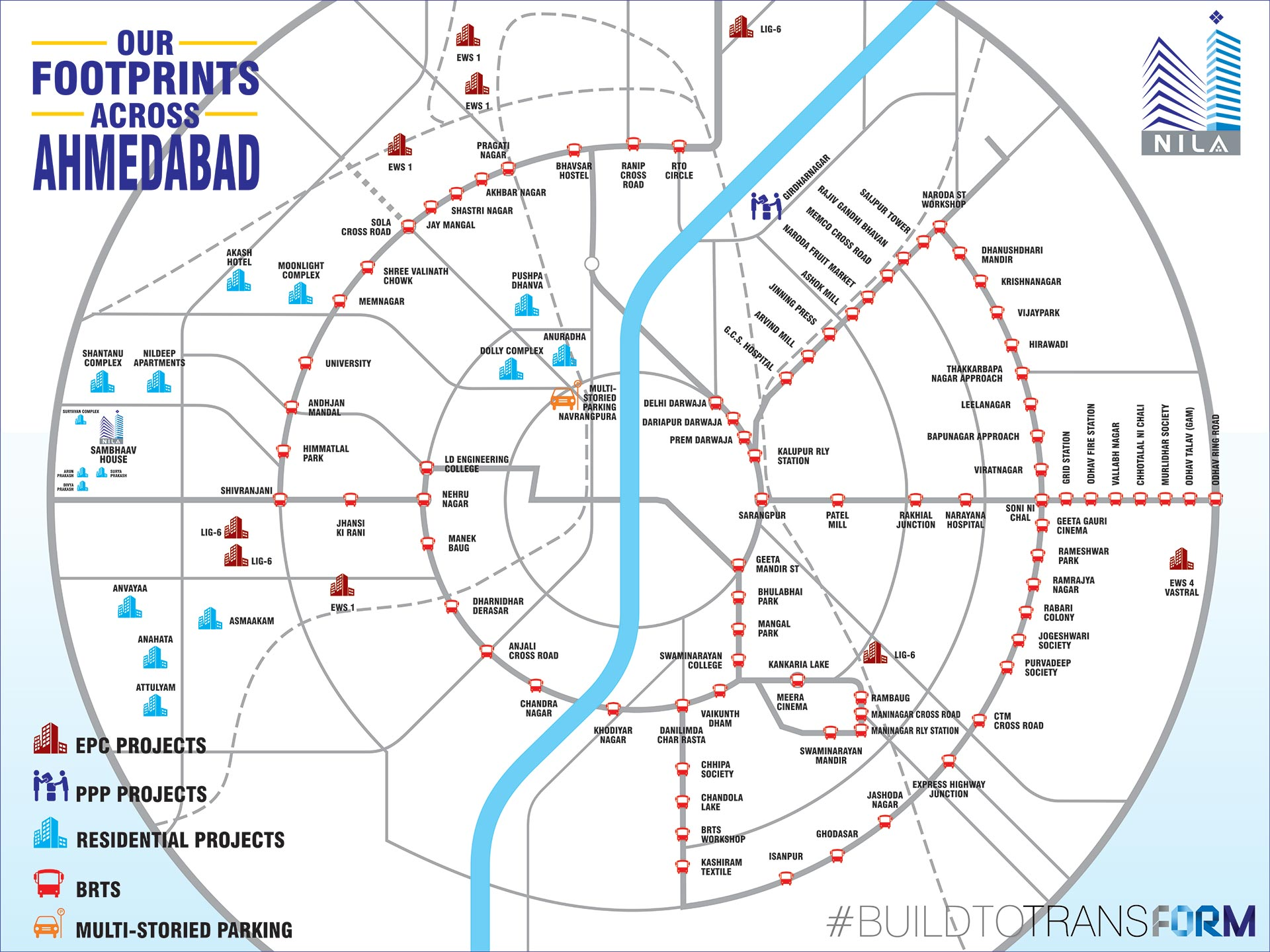

Incorporated in the year 1990, Nila Infrastructures Limited (Sambhaav Group Company - Media) has been promoted by first-generation promoters, Mr. Manoj B. Vadodaria and Mr. Kiran B. Vadodaria. Nila is well established player with a hybrid model in developing Civic Urban Infrastructure Projects on EPC, Turnkey, PPP Mode, as well as Private White Label Construction and Industrial Infrastructure Projects. It also has a long track record of developing and marketing own Real Estate Projects with varied sectors ranging from Affordable Housing to Luxurious Housing. Nila has major presence in Gujarat and has expanded footprint into Rajasthan. Its major clients include Ahmedabad Municipal Corporation (AMC), Vadodara Urban Development Authority (VUDA), Government of Rajasthan (through Rajasthan Avas Vikas and Infrastructure Limited (RAVIL) and UITs), Adani Group, Sandesh Applewood.

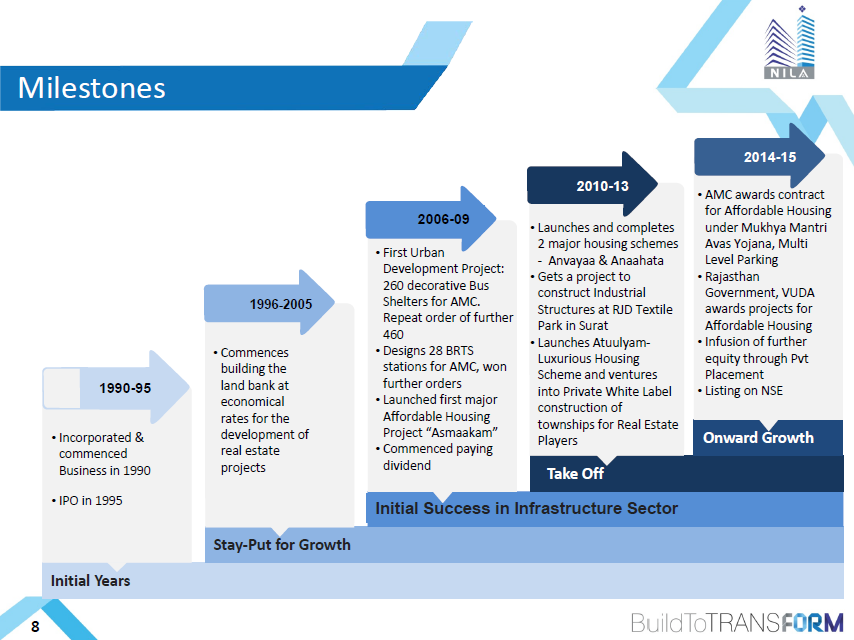

Historical Journey of the company (Transition into Urban Civic Infrastructure Player):

AMTS Bus Shelters

The entry into the Infrastructure space was a fortuitous move and not a consciously planned move by the management. The parent being Sambhaav Media Limited had won a BOT contract from the AMC for building AMTS bus shelters along with the rights to advertise on them for a period of time. Since, it was not a construction company, they had allocated that order to Nila Infrastructures. It was one-off case where there was a synergy between the two companies. We do not really see it in the future because Sambhaav Media Limited right now is not involved with any form of these activities as far as outdoor media or creating any form of assets on BOT basis of advertising, etc.

Relationship between Sambhaav and Nila infrastructures going forward (as per Q3FY16 concall):

These both companies are purely separate companies. One is into the media group and the other is purely in the construction group. So we do not have any relationship within the group, not right now and not in future. Only promoter group is (common) there otherwise there is no other synergy between these.

From Investor Presentation:

- Sole Contractor for first Urban Development Project of 260 decorative bus shelters completed for AMC. Early completion and superior construction quality prompted AMC to award further 460 bus shelters.

- Sole Contractor for 100 Bus Shelters for Rajkot Municipal Corporation (RMC)

FY10: 150 AMTS Bus Shelters construction were completed.

FY11: Total 732 bus shelters were awarded and constructed since the 1st order.

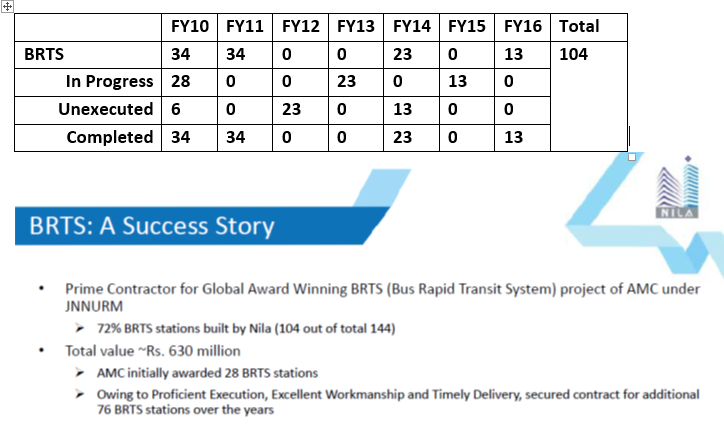

AHMEDABAD’S LIFELINE: BRTS - A qualified success story

The former mayor of Bogota, Columbia, Mr Enrique Penalosa once said –

“A developed country is not a place where the poor have cars. It’s where the rich use public transport”.

Approximation of the progression in the BRTS contracts based on AR data.

Various links related to BRTS (Both positive and negative reviews):

http://www.business-standard.com/article/economy-policy/ahmedabad-brts-catches-fancy-of-several-countries-110082300012_1.html

http://www.business-standard.com/article/current-affairs/ahmedabad-brts-fails-to-bring-down-use-of-private-vehicles-116012000212_1.html

Affordable Housing (Predominantly EWS and LIG)

“We are more bullish on the affordable housing segment because of a simple reason that this is a self-reliant model where government in usual terms is not putting in any money. The governments and various civic bodies are just acting as facilitators between the beneficiary and the developer where the money is collected by the government from the beneficiary and given to us as developers. So that comes about with risk minimization of points being stuck with the government which is usually the case in construction projects and urban infrastructure projects. That is why affordable housing is something that since the time it started in our home town Gujarat and Rajasthan we have been looking at very closely and we have been participating and executing a lot of orders in there.”

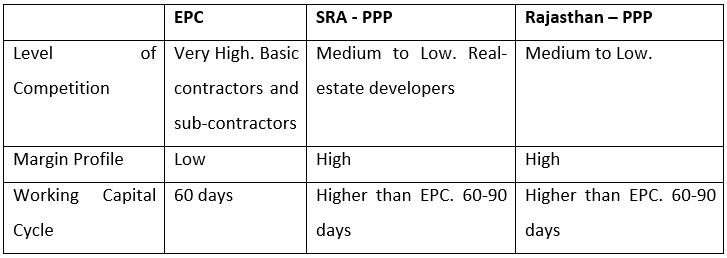

IMHO, I think the management was wise to see the opportunity in urban civic infrastructure and make the transition from being a real-estate company, in spite of the serendipitous nature of the opportunity. There are 3 different models through which Nila gets revenue and subsequently different margin profiles –

- EPC: AMC tenders such as MMAY, MLCP, BRTS.

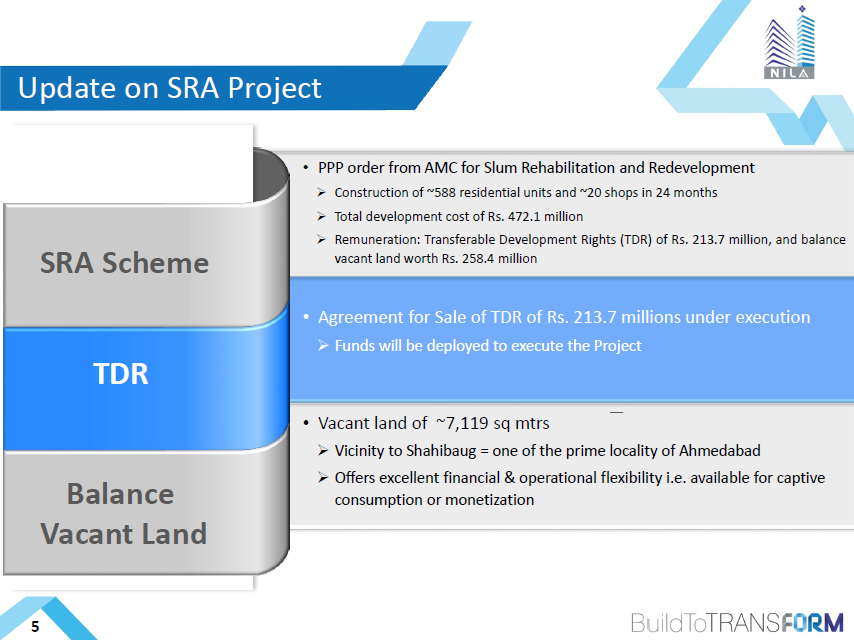

- Traditional PPP: AMC tender for Slum Rehabilitation

- Cross-subsidized PPP: RAVIL Tenders for Affordable Housing in Rajasthan.

Based on above and management commentary in concall, there is no construction cost paid in case of the Slum Rehabilitation. It has to be self-funded by the contractor in the construction phase.

For the current scenario, Nila is selling of the TDR’s worth 21.37 crores to fund the actual project.

Note: There was a revision in the development cost upwards from 410 milion to 472 million, due to which TDR worth went up and Vacant land worth has come marginally down.

Based on management commentary, the order of margin profile would be:

Cross-subsidized PPP > Traditional PPP > EPC.

Revenue Recognition Methods:

- TDR - We would monetize it by this quarter. And revenue from the same would be as per AS-7, so whatever construction for the slum rehabilitation takes place, similar percentage would be recognized from the part of TDR. (TDR’s are typically given for a separate land. In case of Mumbai, i believe TDR’s were given in a region north of the city)

- Balance Vacant Land - Will be accounted using AS-9

The main difference with the cross-subsidized model of Rajasthan govt. is the fact that Nila will be paid the construction cost along with the balance vacant land on completion, while there are no TDR’s.

Opportunity Size of Ahmedabad alone is potentially very high

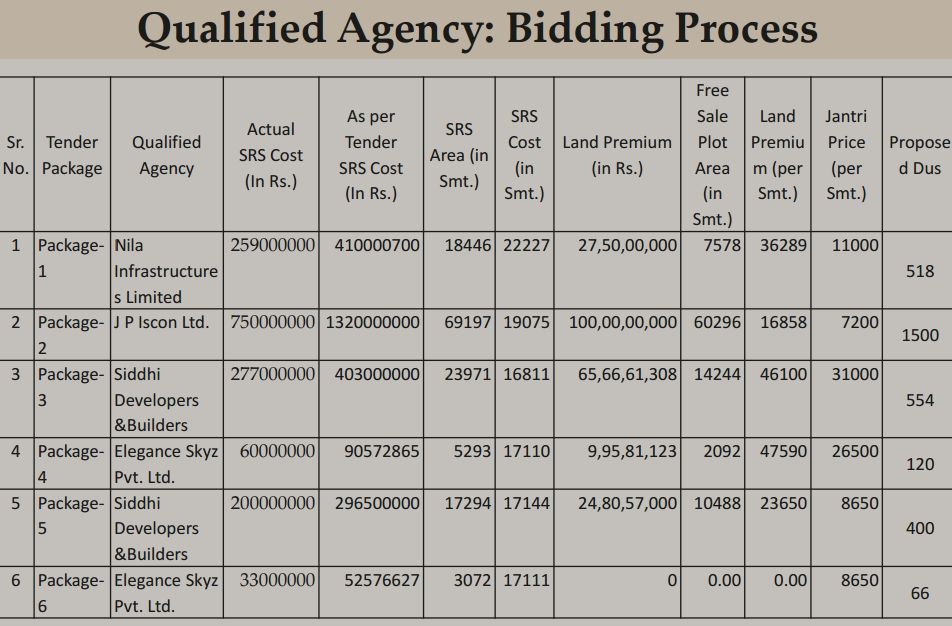

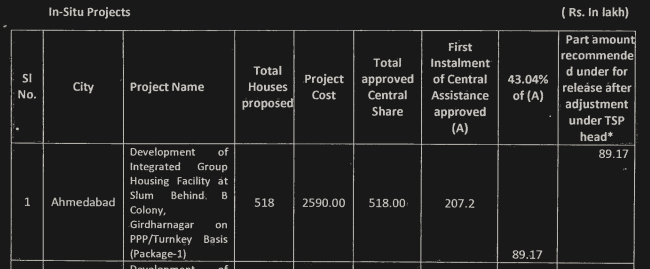

Ahmedabad has 500 slums which needs rehabilitation, out of which only 10-12 slums have been rehabilitated as part of Gujarat Slum Redevelopment Policy – 2010. Nila won the recent SRA tender on PPP model for Girdharnagar as part of the 2013 policy implementation.

Slum Free City

http://smartcities.gov.in/writereaddata/winningcity/AhmedabadSCP.pdf

As per census 2011, slum households stood at ~1.63 L and slum population was 7.28 L. Most slums are heavily populated with substandard housing and lack basic facilities such as reliable sanitation services, supply of clean water, reliable electricity and others. Besides a low quality of life, slum dwellers are also prone to epidemics and diseases which may spread to other areas in the city. Slums also exert a lot of pressure on existing city infrastructure contributing to non-revenue sources, encroachments, illegal establishments and undeveloped land. Currently, more than 40,000 units would be delivered by 2017-18 under various schemes such as Mukhymantri Gurh Awas Yojana, BSUP, RAY (rolled up to PMAY), Gujarat Slum Rehabilitation Policy and Housing Facility under Safai Kamdar.

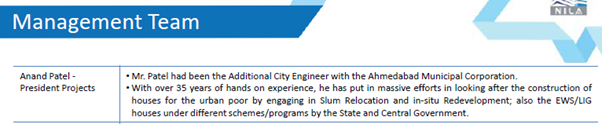

If we consider the addition of Mr Anand Patel, who was the spearhead of the Slum Networking Project while being the Additional City Engineer of AMC, it shows management is very focused on fully capitalizing the Slum Rehabilitation opportunity.

http://ahmedabadcity.gov.in/portal/jsp/Static_pages/slum_ntwk_project.jsp

http://www.egovamc.com/Citizens/RTI/right_info/2014/housing_snp_pad.pdf

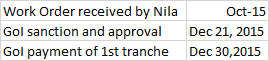

This is backed up the Central Govt. Assistance in partial funding @40% of total project cost through the Housing for All – 2022 mission. If we take the SRA tender as an example, the work order for the project was received by Nila from AMC around end of October 2015.

http://mhupa.gov.in/writereaddata/CSMC04Gujarat.pdf

In the monthly review of the Central Sanction and Monitoring Committee (CSMC) of the Pradhan Mantri Awas Yojana (PMAY), the project was cleared for payments to fulfil Central Govt. contribution and the payment was duly completed on Dec 30th, 2015. http://mhupa.gov.in/writereaddata/Gujarat_417085.pdf

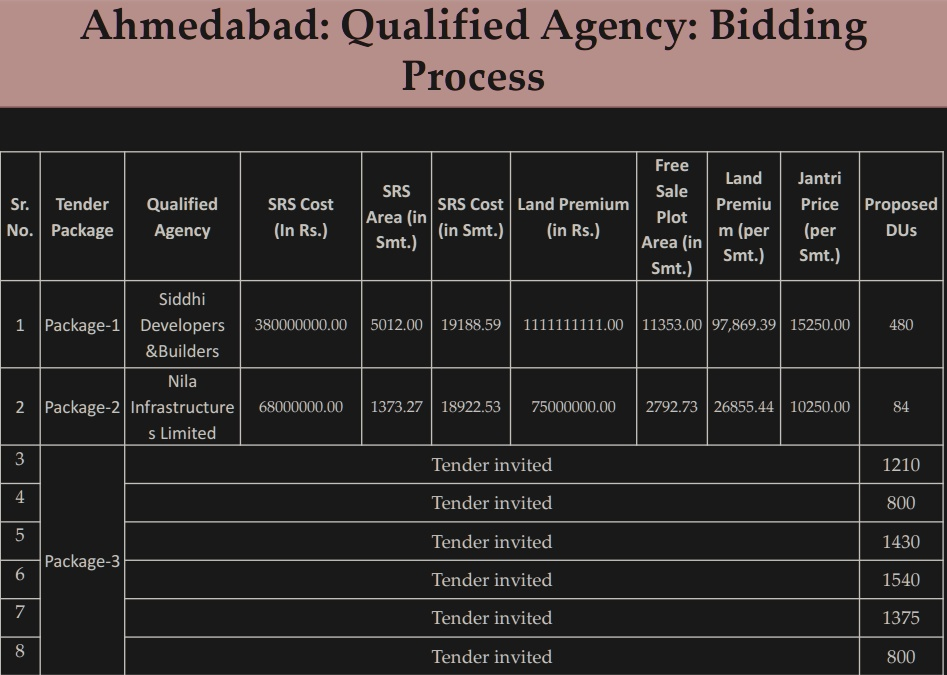

Nila looks like it has won a new tender (though it has not been officially announced) to rehabilitate Kailasnagar slum on the Sabarmati riverfront. Package-3 is the Ramapir No Tekro slum, and would be huge if Nila can manage to win the entire package.

Sabarmati area of Ahmedabad city is considered to develop under “Smart City” so slums near around this area will be Re-Developed under this project. This slum is located at Transit Oriented Zone therefore eligible for development with 4.0 FSI as per local GDCR.

http://mhupa.gov.in/writereaddata/7thCSMC-PMAY-Gujarat-17-03-2016.pdf

Ahmedabad Municipal Corporation: Is it an excellent paymaster?

Himanshu Bavishi: Right our main major customer is AMC, I am sure you would be aware that AMC probably is the only corporation in India, which can offer its own bond without the sovereign guarantee. It is probably double A rated also and their operational efficiency or administrative and bureaucratic efficiency is very streamlined. So AMC is our major customer where we do not experience any blockages. The other one is Vadodara Urban Development Authority and the third major one is Rajasthan Government’s Nodal Agency that is Rajasthan Avas Vikas and Infrastructure Limited. Apart from that there are private white label like Adani and Sandesh Group.

Deep Vadodaria: What really helps the process is that obviously AMC is a very good pay master and has a very good track record, that is how that enables it as one of the best municipal corporations but it can be also noted that majority of the projects that we are doing are all self-funded projects. So, basically the civic body or the government is just a nodal agency in the middle, and they are just collecting money from the beneficiary and giving it to us. There is no big budgeting or planning that is required from the government or the budgets are not really coming-in from the government. That is why the cash flows are smoother than what you probably see in other infrastructure companies where majority of the budget is going to come from Central government or the local government. And such budget gets affected by the stance taken by that government.

http://www.ilfsindia.com/downloads/bus_rep/ahmedabad_bonds_rep.pdf

Negative criticism of AMC

http://www.indiaspend.com/cover-story/ahmedabad-two-steps-forward-one-step-back-59247

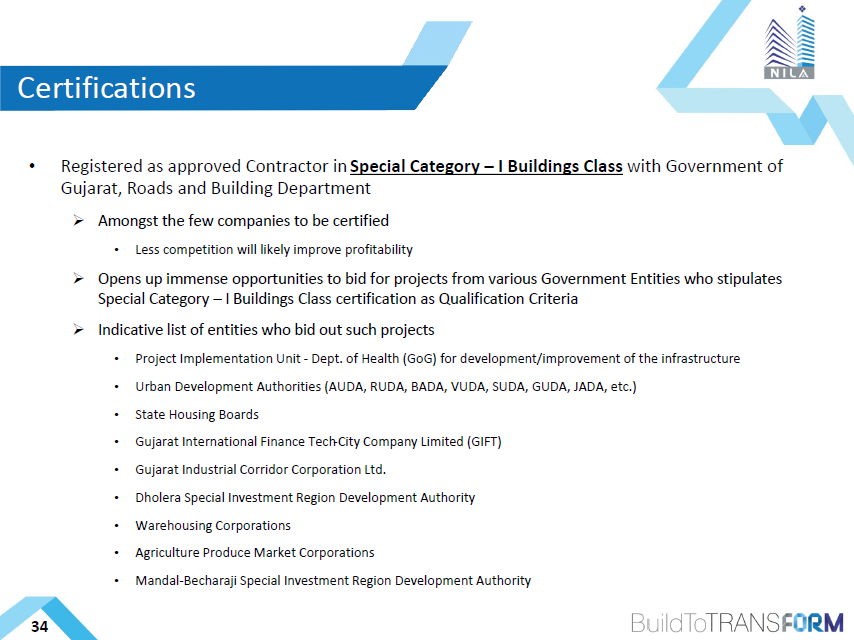

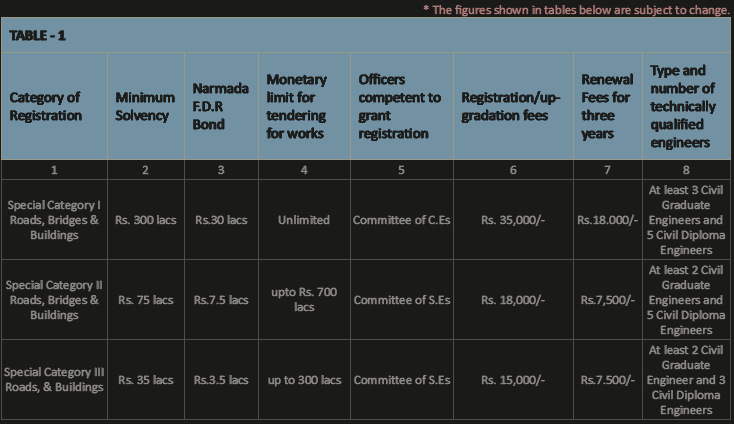

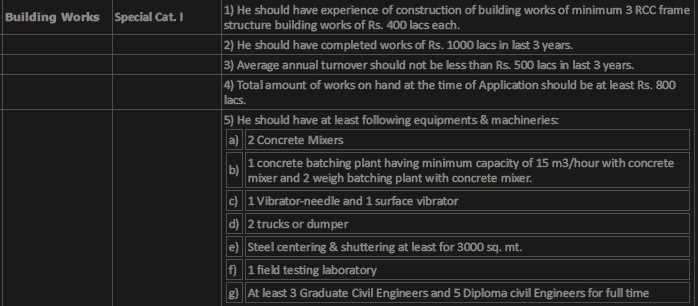

Significance of “Special Category – I Buildings Class” certification:

Deep Vadodaria: It depends on what are the sort of projects that come about with the requirement of having that special certification, it keeps on coming. So as and when they come we do participate but as of now in this quarter we have not really participated in any of those bids. But yes, the bids will continue to flow and we will keep on selecting the bids. We are very selective with the bids, the target ratio or the number of bids that we place against the number of bids we win is very high and we would continue to keep it that way because we are very selective about bids that we do and it is not that any bid that you bid. We are possibly not just bidding for the sake of it. We only bid for projects which we feel that we have a good chance of winning it the way it is. So right now in the Special Category as you are talking about in Gujarat, yes this gives us the edge over other contractors because not a lot of them have this certification in lot of projects. Most of them which are on larger scale they require these certificates and we will actively participate in them as and

when we get the opportunity or we feel that it is a good project to bid for.

From the Roads and Building Department portal:

http://www.rnbgujarat.org/contractors/contractorregis.aspx

An unlisted peer primarily operating out of Vadodara and Rajkot, Cube Construction Engineering Ltd., also has the above same certification as Nila.

http://www.ccel.in/Default.aspx

Rajasthan

Tender won in FY15 - http://www.mhupa.gov.in/writereaddata/Rajasthan.pdf

Rajasthan Government has been making rapid progress in low-cost housing through its ‘Housing the Poor’ programme. An ambitious target of building 5,00,000 EWS, LIG & MIG units over 5 years has been set. For the period from June 2011 to January 2013, the number of low-cost housing units built in Jaipur (309) exceeded the number of units in Delhi/NCR (66), Chennai (30), Hyderabad (200), Bhopal (285), etc.

In the recent “Resurgent Rajasthan Summit – 2015”, while the company had entered into MoU’s worth Rs. 400 crores prior to the summit, it won Rs. 66.87 crores worth of tenders spread across 5 different projects after bidding for contracts worth Rs. 154 crores.

It reiterates the management’s policy to be very selective in bidding tenders, and maintain a high bid-to-win ratio (43%-win ratio).

Business Quality

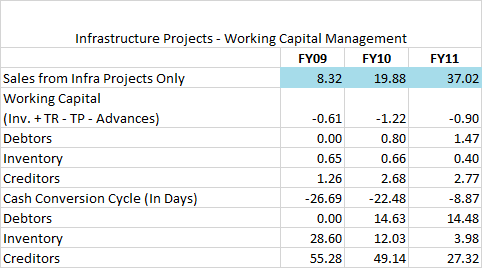

Working Capital Cycle

Management had given separate breakup for FY09, 10 and 11.

From the above, it can be observed that Infrastructure Projects segment is working capital negative.

Caveats:

- This considers only BRTS projects implementation. There is no Affordable Housing portion.

- Sample size of only 3 years’ data which is small.

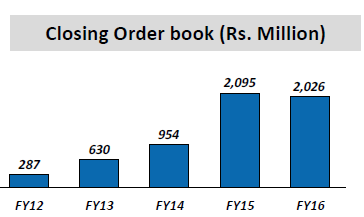

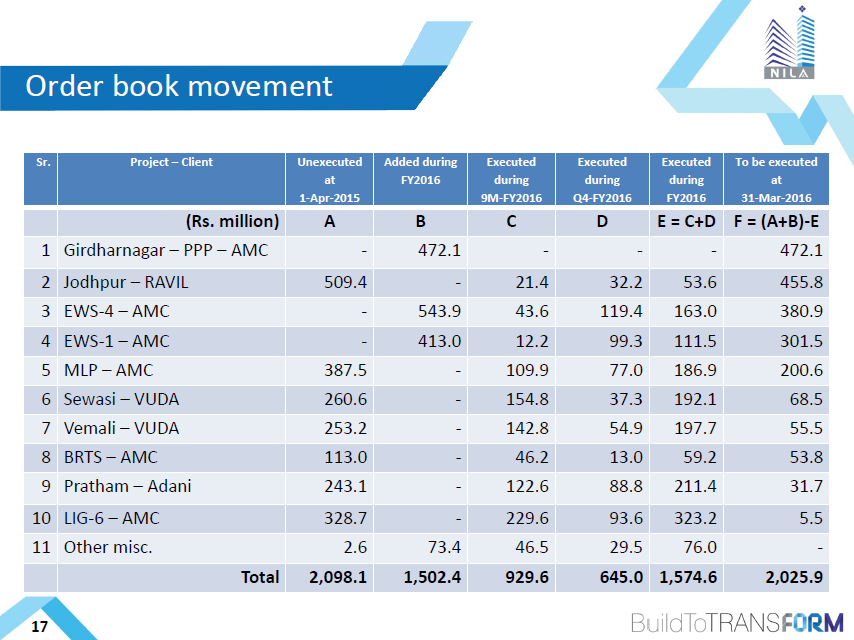

Order Book

The company has executed 43% of the order book (E / A+B), which is consistent around the 40-50% range maintained since FY14.

If we include the recent order win from Rajasthan, then the total order book is INR 2694.6 million, which translates to a Book to Bill ratio of 1.71 (below the management threshold of 2).

One can expect increased bidding for more projects by management in FY17.

Other Optionality

- MoU with Kataria Group – To build Industrial/Logistic Parks near the Mehsana Auto Hub.

- JV’s and Associate Ventures to develop existing Land Bank of approx. 90 acres with a book value of 82 crores.

- White label construction for established entities such as Sandesh Group.

Management Quality

(Not so good at assessing mgmt, but below is a rudimentary attempt)

Marking a HR policy ground-shift, we are among the first in our category to introduce an ESOP (Employee Stock Options) scheme for all our employees. This, among others, is an excellent employee retention strategy that is going to further lower our already low attrition rates.

In a significant attempt at capital structure reform, the company has issued shares on a private placement basis, raising the authorized capital by Rs. 15 crores and reducing the proportion of promoter shareholding.

Posting the below note from India Ratings report (thanks to @ankitgupta )

During the concall found the below exchange very fascinating:

Deep Vadodaria: We have at present about 85 employees. These are our company employees and otherwise, as you understand the dynamics of this industry, a lot of things is being done through contractors.

Vishal Agarwal: And which is booked under project expenses?

Deep Vadodaria: Yes, that is true.

Vishal Agarwal: So if I look at the breakup of these 85 employees what could be the broad breakup because the numbers are not getting translated in the employee cost. It is around Rs. 3 crores odd in employee cost.

Deep Vadodaria: Yes.

Vishal Agarwal: Out of which Rs. 0.5 crore is towards the senior management so with Rs. 2.5 crores and 85 employees comes to a very low base?

Himanshu Bavishi: Yes. There are two disclaimers. One, this company has been into existence for about 25 years now and was basically nurtured by the promoters as a traditional company. And then two, Ahmedabad has not been a market which is where the salary packages are as good as Bombay. Our employees have been with us for years together and there is hardly any attrition that we have experienced so far.

Deep Vadodaria: So I will just put it this way that your question was that it is not really translating in Rs. 2.5 crores, how do we have so many employees. Is that your question, Vishal?

Vishal Agarwal: Yes sir. I just wanted to check if we have a bench strength enough to execute Rs. 2,500 million of projects. So I was just trying to get that?

Deep Vadodaria: Yes, we do and as and when it is required, we keep on taking fresh people on board. Like we have just taken Mr. Anand Patel who has a rich experience of almost 40 years in executing only affordable housing for the government. He has, in his life span, constructed or overlooked construction for about more than 40,000 houses. So, and when it is going to be required, we will get people who are willing to do the job and who have the sort of track record to do so, like I just mentioned one person at the senior level that we have just appointed. He is the first one who started the Slum Rehabilitation model so now it is going to be of tremendous value to us when he is on board and we are getting into the whole foray of slum rehabilitation project. So and when required for a specific project, we do make these appointments at senior level and also at junior levels. And as Himanshu rightly mentioned, that it can be noted that the attrition ratio of the company is very, very less compared to the overall market.

To verify the above, it does make sense when we see the CS + CFO getting a combined salary of 13 lakhs per annum.

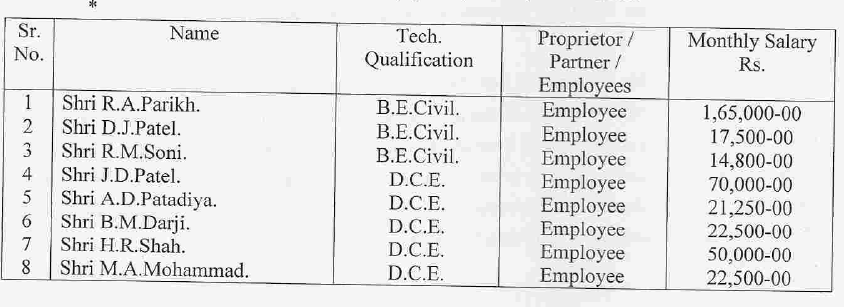

Below is a snaphot of the employees who are responsible if and when the company gets the Special Category related tenders.

On ESOP’s

Options allotted to Key Managerial Personnel

a) Prashant H. Sarkhedi, Chief Finance Officer: 500,000

b) Dipen Y. Parikh, Company Secretory: 350,000

Exercise price equals market price: Rs. 6.64

And sir, if you can tell us how many share warrants are there including the ESOPs and in terms of conversion when it will happen, so just wanted to understand in terms of the increase in the number of shares going forward.

Dipen Parikh: There are 1.10 crore ESOPs that have been granted earlier and there were around 25.80 lakh (ESOP) granted around 15 days back from the overall ESOP plan of 1.50 crore options. With regard to the warrants, they were issued to the promoters last year i.e. 2.25 crores warrant convertible within a span of 18 months. So, up to July 2016 they are exercisable.

Shravan Shah: So by July this 2.25 crores number of shares will be added?

Dipen Parikh: Yes, if exercised, they will be added to the equity.

Shravan Shah: And that ESOP time limit is one year?

Dipen Parikh: ESOP is having entire time span of five years and it is at the discretion of the employees. So it is difficult to say the exact time limit but they will be exercisable within a period of five years as per the different vesting time periods.

Again given the total number of options being granted is 11 million, the CS and CFO are getting very miniscule amount relative to the average employee.

Concerns

- Negative Operating cash flows till FY15 (which i think is mostly due to the overhang of Real estate inventory - Atulyaam project). Keenly awaiting the AR for FY16.

- High proportion of ST Loans and Advances (to JV’s) relative to the Current Assets

- Lack of clarity on how management views it land bank. Does it see as an Inventory like Ashiana, or does it view as an Asset (point raised by @Anant)

- Change in government with the upcoming state elections in Gujarat and Rajasthan in next 2 years.

- Dilution of focus from management as the JV’s and Industrial Logistics begin to come into the picture.

I found the company website to have excellent disclosures, and even their Annual Reports are filled with farnamstreet style anecdotes. In fact, they also have an interactive AR.

I need to highlight here that the main source of the idea origination was an unrelated tweet by @ayushmit back in 2012.

Some Links for further reading:

June 2016 - Investor Presentation

Case Study of the first batch of Slum Rehabilitation Projects in 2010

Report on Atulyaam Project - https://im.proptiger.com/2/1/509666/105/251456.pdf

http://amrut.gov.in/writereaddata/Local%20Area%20Planning%20in%20Ahmedabad.pdf

Disclosure:

I have bought my initial position in May @13.8 and have averaged down as my conviction increased. Currently it makes up 5% of my portfolio.

This is neither a recommendation to buy/sell.

Intention is to get contrarian views to negate my investment rationale.

Please do your own due diligence.

!!

!!