Hello,

This is my first post on the forum, having learnt a lot from the various posts.

I work in the Corporate Banking domain for one of the main Private Banks, so going through balance sheets on a daily basis is part of my work. However, I do not see myself as an expert in terms of investing basis a deep balance sheet understanding.

Coffee Can type of investing suits me as per my limited balance sheet understanding, and as my equity investing is planned for at least till the time of my retirement. I invest major investing amount into the portfolio on a regular monthly basis, to try and attain a rupee cost averaging instead of trying to time too much. Some portion I keep on the side for a timing opportunity.

My first aim was to just beat the Index. Working in the Corporate Banking domain I feel I have a better understanding of banking, so I started with evaluating investing in Kotak Bank ETF, but I did not want any money in PSU stocks. So I started with a portfolio of Private Banks and am comfortable with it being skewed towards the domain. Also, my understanding(which might be totally incorrect) is that with increased marketing of MFs and Index investing, the SIPs into the major Nifty stocks will continue(and will change only with a big change in Nifty composition).

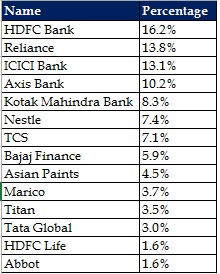

HDFC, ICICI, Axis and Kotak - These together help me diversify within Banking. I ideally want a much higher allocation to Kotak, and am working towards that.

Reliance - Forms a large chunk due to its weightage in Nifty currently, and majorly due to their plans in the retail domain. There are a lot of firms I have met in the domain, and their feedback about Reliance’s agresiveness is the same. Based on all that I have read and understood, I have the feeling that Mukesh Ambani wants to be the biggest entity in India and wants to get to the Alibaba/Amazon level in India.

Nestle - Was a pick due to a Peter Lynch line of thought. I was reading his book and asked my wife to tell me a firm she felt would do really well in India. Being a Coffee lover, and having seen the kind of product range Nestle has internationally whenever we have travelled to other countries, she told me Nestle can expand to a huge product range in India. I analysed the financials, and decided to invest, which has turned out really well in terms of returns till now.

TCS - I wanted to have some exposure to the IT domain, and between Infosys and TCS, decided on TCS due to the Tata group and the various articles on the web I studied about the firm.

Bajaj Finance - Again from the financial domain, but seeing the kind of retail debt I saw everyone around me taking(plus the increased focus of the banks towards that domain as well now), I wanted an exposure in the domain. From all of my analysis and the options available, Bajaj Finance seemed the best bet for the long term.

Asian Paints - I do not have an in depth understanding of the domain, but based on the historical track record(plus the financials showed enough strengh), decided on the firm.

Marico - Wanting an additional exposure in FMCG, with the other firms have very high valuations, I decided on Marico since I was getting good value plus again the historical track record and the increase towards the health segment helped me decide in favour.(Other candidates were Britannia and HUL).

Titan - I handle the Jewellery segment in my region for my bank, and while I personally never thought that in the long term our generation will buy a lot of gold, I was proved wrong looking at the kind of business the unorganized sector does(many small players are my clients).I saw that a lot of business Titan can still eat into(and is regularly eating into). They have already proved adept at moving from watches to Jewellery, and seeing Taneria being launched I was confident of their long term prospects. Being from the Tata group also helped.

Tata Global - This was a very small bet as I really wanted to get into the Starbucks story, plus I wanted to own a small cap stock as well before the days it became big. While it will take a long time for Starbucks to be big, which I feel it will seeing their presence in other countries, and our culture shifting to a daily coffee habit after some years. Already the multiple Starbucks around me are always full despite the prices(I buy a stock of Tata Global every time I go to Starbucks for a meeting and don’t buy an expensive coffee, just for fun). The FMCG strategy of the Tata Group might do well too, but I do not have the confidence yet to invest a larger amount(the stock has run up a lot too). Trent was a candidate which I decided to pass up in Tata Global’s favour.

HDFC Life - The Life insurance business will do well as per my understanding. Banks sell a lot of Insurance as cross sell, as some people might have noticed, and HDFC Bank’s branch network and aggressiveness will help HDFC Life do a lot of business in the future. HDFC AMC was also a stock I wanted to own, but I was not sure about the long term prospects of the AMC domain in general.

Abbot - Wanting an exposure in the Pharma domain, but not having an in depth understanding, my first criteria was a debt free firm(an advantage with Nestle as well), as I have seen first hand in my job what debt does to a firm( I am confident Mukesh Ambani can handle it). Pfizer was another candidate but I liked the financials of Abbot plus the product range expansion plans looked good. This has given good returns till now as well.

I am looking for a chance to increase allocation to the non financial stocks whenever the timing is right.

In addition, I have SIPs in:

- Axis Long term Equity(Direct Growth) ELSS for wife(expense : 0.92%)

- Mirae Asset Tax Saver(Direct Growth) ELSS for myself - I liked the lower expense ratio of 0.3% and figured Mirae would want to improve the AUM of their ELSS so will focus on performance. Mirae has a good record and Neelesh Surana’s performance in his other funds is good.

The other funds I have are Multicaps/Focussed funds from 3 different fund houses because I don’t have the knowledge for Mid Caps/Small Caps, so I was okay with giving that authority to a fund house. Low expense ratio was a big criteria.

- Kotak Multicap Fund - Direct Growth(Expense : 0.87%)

- Axis Focussed Fund - Direct Growth(Expense : 0.65%)

- Mirae Asset Focussed Fund - Direct Growth(Expense : 0.23%)

Hope the long post made sense. Will edit and correct this for mistakes.

Happy for any feedback on this.

Thanks,

Himanshu

)

)