I am researching some global companies, which others may find interesting.

My intention here is not to present a thesis for the company, but to present a few points to ponder and learn. We know Amazon, Berkshire, Apple, and few other companies have delivered outstanding returns to their shareholder. However, there are a few other companies that are dominating their niche like Temenos, has delivered outstanding returns (28% CAGR over ten years and 15% CAGR since 2001) to their shareholders.

This thread can be used to learn from these global leaders in their niche or help us when investigating Indian companies in the banking product niche (e.g Intellect Design Arena). Here is my first stab at Temenos.

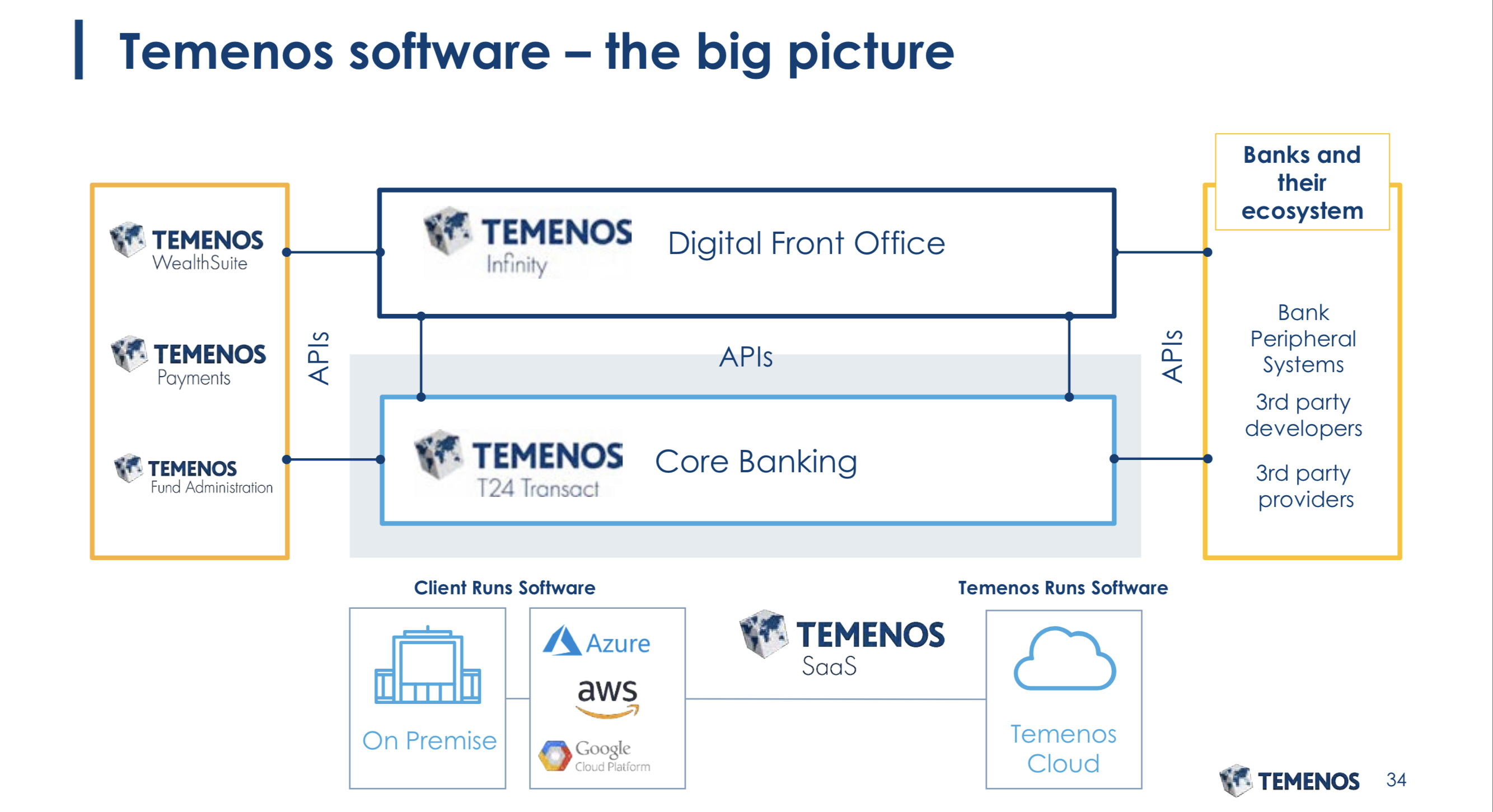

Temenos (TEM) is a leading banking product companies based in Geneva Switzerland. It has been developing banking products for 25 years. It operates across the full spectrum of banking software from the front office- core baking to cloud.

Temenos has shown consistent increase in revenue/profit/EPS over many years.

(source- morningstar.co.uk)

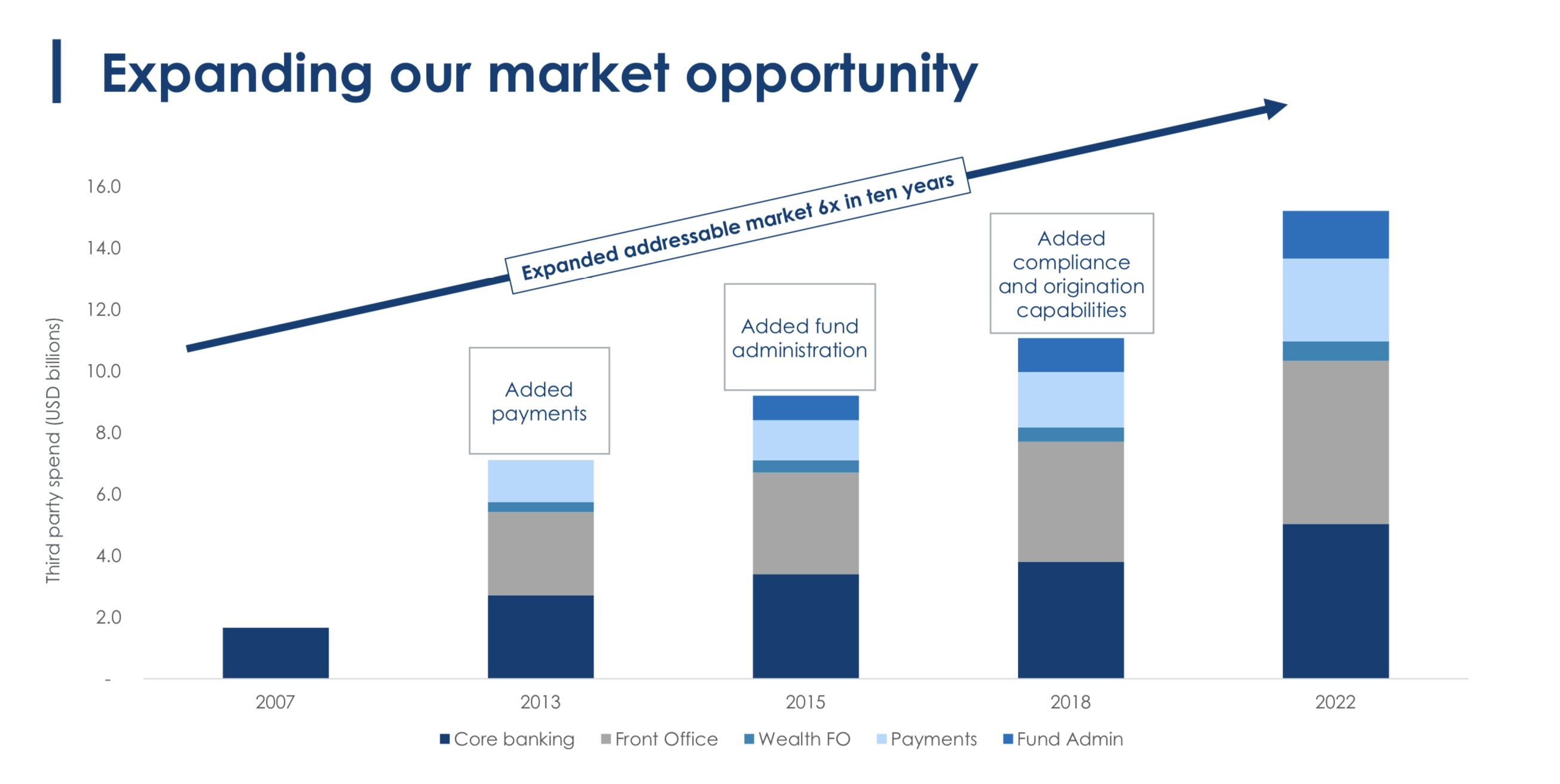

The market size of their TEM products is around $12 billion globally and expected to increase by 8% CAGR by 2022. Moreover, they are incrementally adding capabilities to their product, enhancing the addressable market size.

TEM had a profitable business before 2013. On the back of existing profits, they have managed to add capabilities mostly in-organically and the pace of capacity addition is increasing recently.

As shown above, TEM acquisition size has increased since March 13, maybe due to a sense of urgency to dominate their niche segment. They are also earning good profitability (and free cash flow). Strong profitability (and free cash flow) coupled with a stronger balance sheet allows them to acquire more companies with complementary capabilities, resulting in the rich product set.

As a result, they are increasing market share as shown below. On average, they are selling more than 5X more products than their average competitor.

Key takeaway (How did they achive it)

Focus on R&D

TEM invest around 20% of revenue in R&D, and it is even higher in the last few years, touching to 25% of revenues in 2013/14. Considering, TEM has a revenue of $900 million in FY18, they have spent around $180 million just on R&D. I do not think the smaller players have a luxury of spending such money on R&D. Agree, that spending huge money not necessarily your means success, but if you are a leader and constantly investing in the areas where the client is looking for, you increase your chances of success significantly. Furthermore, TEM has been an active acquires of Companies in their space, giving them access to the latest technologies and clients, further cementing their leadership position.

Cloud

Cloud deals are getting a lot of traction in the banking segment. By their nature, Cloud deals long term in nature (3 to 5 years or maybe more). As a result, the bank wants to make sure that the company (who’s product they are buying) has a balance sheet to support themselves for several years. Hence, they are looking for companies having a strong balance sheet. Due to this, the smaller player suffers disproportionately as not all of them have a strong balance sheet, resulting in market share shifting to a stronger player.

As per company management, TEM is increasing market share, but other players (maybe first 4-5 products in the niche) are getting more business, too. The incremental business they are grabbing may be from the smaller players, who find it difficult to sell the on-premise license and have a weaker balance sheet.

I think the market is getting concentrated in the hands of a few players, and the biggest benefit is the leader. This pattern is evident if one looks TEM, whereas the number of deals signed has improved significantly. I think the same pattern can be observed in other product segments to like Insurance (Guidewire -Insurance product leader) or Intuit (Accounting software leader). With the leadership, they are earning higher revenue, higher profit and increasing cash flow and rapidly scaling their business, creating a vicious circle.

Winner takes all market. Although TEM management says it is Winner take all market (and they are dominating it), it is not true in entirety in my view. I think (I have not data to support) TEM is gaining market share, but the looses in this would be smaller players, who are unable to upgrade their capabilities. The leading players are able to grab more and more business at the expense of a smaller player, who is getting marginalised.

Tier 1/Tier 2 clients

TEM generate around 50% of revenue from Tier 1, and Tier 2 players and their long term aspiration are to generate approximately 60% of revenue from Tier-1/Tier 2 customer. Top tier customer provided high license revenue; they also provide high AMC (Annual Maintenance charges, are per cent of license fee).

Moreover, Top tier customer would rather deal with a company having a leading product and high compliance rather than risking their reputation to a smaller player.

Indian product focused players like Intellect Design Arena (& Majesco in insurance) are missing top tier segment. Although they have few Tier 1/Tier 2 clients, these are not many, and it is reflected in their subdued profitability. They (Intellect or Majesco) may show good data points like a number of active clients, a number of clients going live or on in the cloud. However, when it comes to profit, they struggle.

References

1- Capital Market Day

2- 2018 Annual Reports.