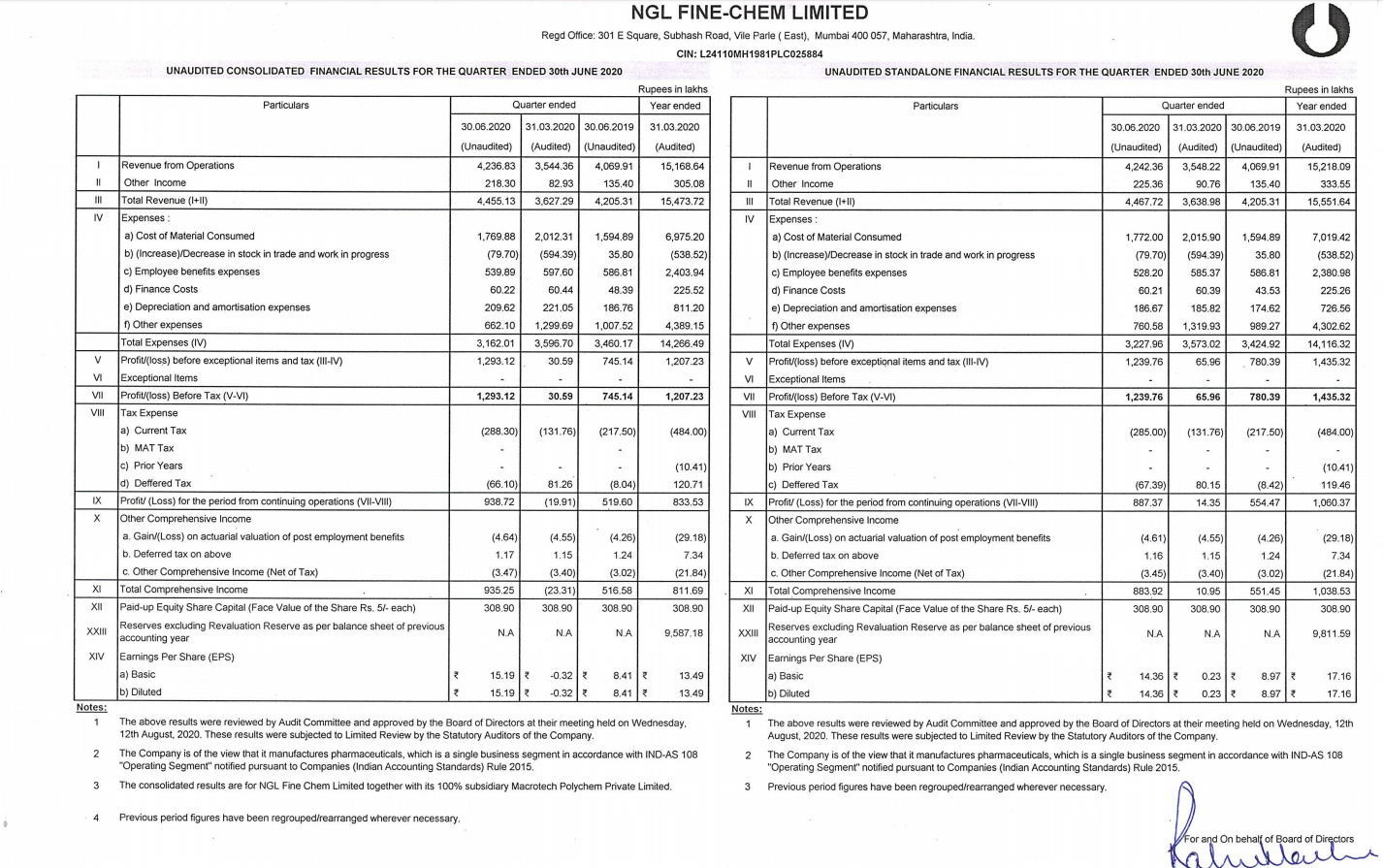

Strong comeback made by the co with superb Q1 results. Standalone OPM: 29.7%, best in the recent history, EPS - 14.36 from 8.97 (yoy)

5 Likes

Adding my notes from Q4 call. Hopefully I am not repeating content.

The global animal API market size reached a valuation of nearly US$38 billion in 2019 and is expected to witness a CAGR of 12.5% to US$ 61 billion by 2023.

Our entire product range is for mammals. We don’t have any product for poultry except two which are under development right now. Currently these two don’t contribute anything to the top line meaning the sales are probably less than half a percent of our total turnover.But going forward we hope that it will contribute to at least between 8% to 10% of our sales by the time we reach the 250 crores turnover in 2-3 years at 18% CAGR.

Top 10 products contribute 78% of sales. similar mix will continue for next couple of years as the demand for these products are high with a growth of 15% for next 2-3 years and we are market leader in top 3 products with a market share of over 50-60%

3 Likes

What would be the impact of Sequent Scientific with takeover by Carlyle group on NGL?

Recent ratings reports highlighting improvement in company fundamentals and demand scenario in current times. Have a look.

Disclosure: Invested. Only for educational purpose.

6 Likes

The company seems to be investing in mutual funds and equity shares to the tune of Rs. 10.65 crores (AR 2020 - page 102). A bit difficult to understand when it can easily to pay off the debt or borrow less.

Why should a company borrow for cash cycle while other money is sitting in shares and mutual funds?

Disclosure: Not Invested but Interested.

5 Likes

Mr Rahul - MD Interview

6 Likes

These videos seem to be from 2010-11. Listen to part 3, 3:20.

They generally keep it for liquidity. It’s like if we have home loan, still we prefer to keep emergency funds in liquid funds.

3 Likes

Okay. Could there also be a case where they would be using this liquidity to lever up the company by taking lien against mf?

Thanks for sharing these. Though these are old videos of 2010-11 timeline, but it was good to see the clarity of management. Having done interview few years back and while listening to recent concalls, its heartening to see the same consistency in management  Same focus on quality, value addition, good business ethics, good customers, market leadership etc etc.

Same focus on quality, value addition, good business ethics, good customers, market leadership etc etc.

On a tiny unchanged equity capital of just 3 Cr, this company has come a long way from a turnover of just 25 Cr in 2008 and profits of just 2-3 Cr to probably 250 Cr+ turnover this year.

16 Likes

Very good insights on Animal Pharma industry: https://www.youtube.com/watch?v=QN8bpEY4ys0

3 Likes

Sir, very well said. Your thoughts on NGL performance in view of Carlyle taking over Sequent Scientific

I think its good that Sequent is doing well and when a large company like Sequent which is already 1100-1200 Cr turnover aims to double its business, it indicates the large opportunity size and also lays out ways to grow for other cos. Given the rich valuations that Sequent is getting, NGL can get attention as its ratios (profitability) have been better than Sequent till now.

16 Likes

The Carlyle PE deal of Sequent valued around 2000 cr with profits of around 50 cr + in mar 19 …look at NGL finechem ,this year /next year they will do close 50 cr PAT -current market cap only 730 cr !! The return ratio of NGL is better than Sequent …what I like about NGL is clear strategic focus and conservatism with clear focus on ROCE /value creation

NGL : 1) have tail wind of China +1 strategy 2) Growth from existing customers in next 5 -10 API’s (not the top 5 only ) 3) New capex yet to be leveraged …poultry is a big opportunity than present pie (3X + though profit margin is lower ) 4) future opportunity in regulated market …the stock has the potential to become 10x in less than 10 years ,lets see what holds for us in future

8 Likes

But mgmt has indicated that they do not want to enter regulated markets now.

I had 1 question: in last concall mgmt indicated of 10-15% growth for next 2 years without capex. H1 of FY 21 saw huge growth due to market share gains and demand for their products. Do we expect 10-15% growth even at this high base for next year? My view was that some of this growth may be due to pending demand due to lockdown and may wither away going forward. Not sure if we will still see 10-15% growth at high base…any views.

Tracking for now

Margin profile and Roce profile of both the Businessess would be very different 3 years out. Think in terms of the incremental returns. Ngl won’t be entering regulated markets. Took 4+ years of pain period for Sequent to get it right

7 Likes

Won’t the current bird/avian flu scare that is going on in 5+ states affect their margins? As I see it, this flu is now becoming seasonal with low/high impact on birds and correspondingly the supply of chicken to the market?

They are yet to get into poultry if I am not mistaken…and their products are for exports only. So no impact.

Regards,

Raj

Disc: Invested

2 Likes

i personally think the base is not high …no one can predict growth accurately (and consistently )in long run ,it short run ie for few quarters ,the promoters (they have best knowledge about their business ) is very bullish on growth and hence we have to reply on their judgement …i normally like companies who under promise and over delivers (NGL was like this ,very conservative ) ,first time seeing them bullish than before ,though they are still very cautious and hence wants to see for themselves for few more quarters

1 Like