Any idea why the stock is constantly hitting upper circuit these days? The results have been decent but does it warrant this run up?

1 Like

Hi,

Is anyone from Mumbai attending the AGM tomorrow (31-Aug)?

I am sharing few questions with the group, anyone attending the AGM please try taking these up:

Q1- Management had said co. will be able to maintain OPM in the range of 15%, but we have been able to achieve OPM of more than 20% in the recent quarters- is this the impact of modernizing recovery system or due to a better product mix, or is there any other specific reason for improved OPM?

Q2- Can you quantify/discuss the expected growth from our upcoming CAPEX of 25 cr ? Any timeline for the same?

Q3- Top 5 clients and their share in revenue?

Q4- Can you provide the product wise break-up of revenue?

Q5- Any future plans of entering into the regulated market? or seeking approval for the same?

@nikhilmoryani will you be attanding the AGM? Your notes from last year’s meet were really helpful…please share the same this year as well (if you attend  )

)

Thanks,

Yogansh Jeswani

Disclosure: Not Invested (tracking).

1 Like

^bump,

we should explore this company more. any updates?

1 Like

The stock normally gives good quick 20% on results… The trick is to wait for the fag end of fall just before the results… This is repetitive activity for atleast 3-4 qtrs now…

Disc: Holding since longterm. Booked some 20% holding some time back.

1 Like

NGL Fine Chem - AGM 2016

The company held its AGM on 31st Aug’16 and was addressed by Mr. Rahul Nachane MD

Key Highlights

The company has completed the capex program of Rs 25 crore in Tarapur plant with which additional 35% of capacity has been added. Although the capacity addition would depend upon the finished product, technically the company will be able to produce higher volumes by 33% of the current capacity.

With this new capacity, now the company can generate a double digit sales growth in future for next 3 years. Management expects barring an uneven quarter of one or two due to additional depreciation due to the capex and incidental expenditure costs, growth momentum will remain intact going forward.

Veterinary segment is poised for a strong growth in the next 3- 5 years. Lot of outsourcing opportunities has emerged in this sector.

The company has 2 long term contracts and needed more capacities and scale to get the long term contracts. With the added capacity, management is trying for such 3-5 contracts which it expects to receive by the year FY’17.

The margins for Q1 FY’17 were helped by higher offtake of high margin products by an international customer in exports business along with rupee depreciation. It’s difficult to determine the margin exactly as different products have different margins. On an average, given the fall in raw material prices and a depreciated rupee, average Ebidta margin will be around 19-20%.

More than 90% of company’s business is API’s. More than 80% of the total business is exports.

The growth going forward will come from existing products to existing customers, new products to existing customers, existing products to new customers and new products to new customers.

For FY’17, management expects net sales of around Rs 110 crore

The company does process tests of only off patented and matured products in its lab and has delivered about 16-18 API products. 3 more are in the pipeline for FY’17.

Post the completion of capex program, management expects dividend to be declared from FY’17 onwards.

Source - Capital Line

16 Likes

When does the added capacity come into operation. Going by the quarter ended Sep’16, the sales have not seen any benefit for increased capacity

It is strange that the management has declared the capex completed in the AGM, especially since the AR 15-16 states that the capex will finish only in 1st quarter of FY 17-18. This means it was scheduled to be completed between Apr-June 2017 but instead was completed barely 2 months after the AR was released.

I feel there may be some lacunae in the AGM minutes prepared by Capital Line - it is rather more likely that the capex was started when the AGM took place.

2 Likes

@Leading_Nowhere - Precisely! Capex coming online is still 3-4 qtrs away.

Hi Everyone,

Any Idea when the new capacity is coming up?

Thanks

Vinay

NGL AGM notes:

Product and Strategy:

Company is more focused into veterinary APIs. Though they do veterinary formulations and human API in small proportions, the focus areas is veterinary API. Company is NOT focused on US and Europe markets. US and Europe require huge investments and long gestation periods. There is enough scope in unregulated markets of Latin American and African markets. The company supplies to formulation manufacturers of those countries as well as to MNCs. This will be strategy going forward as well. The company earlier needed agents to supply to these markets. Now due to better relationships developed over past 5 years company supplies to formulation companies directly. This has reduced the commission costs of the company.

Expansions:

Current 30cr expansion in Tarapur is almost 90% complete. First phase will be completed by October and by Jan second phase will be ready. Plant will be fully operational for FY19. Total sales can be 60-70cr from this capex in next 2-3 years. There are customer waiting for this capex to complete. The expansion is for current set of molecules already manufactured.The plants has zero liquid discharge and fully automated which require very less man power.

Only this capacity reached 50% of the new capacity, company has plans for next round of capex for which company has already procured the land. This capex can be for around 50cr. The company is already seeding the market with these new products/molecules.

R&D folks will be increased from 18 to 30 in next 3 years. Mostly MSc and PhDs

Margins expanded due to following reasons

1 Energy conservation due to better heat recovery systems. Water usage was halved. Recovery of water heat.

2. Minimise wastage lead to almost 2% improvement

3. Strong r&d - improved yield efficiency and strong processes. Processes were improved for older molecules which lead to better cost efficiency.

Other points:

The company works on 90 day credit and there are 30 days for shipment. Hence receivables will always be high for the company.

Company works only with USD. Forward cover with continuous hedge.

Capital will be deployed back in business rather than dividend at least for next one year.

Competitors include sequent and Lasa in listed space. There are 30-40 companies in unlisted space who are competitors.

30% of sales are long term contract. Remaining are spot contracts.

I would rate the management highly for

a) for clear strategy and focus of attacking unregulated markets first

b) seeding market for new molecules and planning next set of capacities ahead of time ( giving good future visibility for next few years)

c) cost optimization measures leading to higher margins

d)Less customer concentration risks. Top customer is 12% of sales

Big risk is raw material price increase.

34 Likes

Thanks a lot Anand for sharing the details.

thanks a lot for sharing these notes.

FY 18 Q1 Results: http://www.bseindia.com/xml-data/corpfiling/AttachLive/b7b7f8e0-3720-43b9-9212-2a193041620e.pdf

Subdued numbers

NGL Fine-Chem Ltd’s expansion project commences trial production runs

Posted On: 2017-10-05 08:37:35

NGL Fine-Chem Ltd is presently expanding its production capacity by incurring total capital outlay of Rs. 30 crores. The plant is ready for production and trial production runs have commenced form September 23, 2017.

Shares of NGL FINE-CHEM LTD. was last trading in BSE at Rs.316.05 as compared to the previous close of Rs. 315.7. The total number of shares traded during the day was 883 in over 23 trades.

The stock hit an intraday high of Rs. 321 and intraday low of 311.8. The net turnover during the day was Rs. 279892.

Source: Equity Bulls

Link: http://www.equitybulls.com/admin/news2006/news_det.asp?id=214325

Do we have any update post this information?

2 Likes

NGL Finechem Management Q&A – 26 Feb 2018

– Ayush Mittal

– Donald Francis

Human APIs/Veterinary APIs

Kindly educate us a little on NGLs addressable domain. Any plans for addressing adjacent domains?

We are into Veterinary and Human APIs. If we look at the Industry 80% of Veterinary products are also used for Humans. Exclusively veterinary products would be about 20% of the market.

Anthelmintics – De-wormers – is one major category of products we operate in. Animals have to take de-worming once a month due to raw food and conditions they ingest in. There is a huge number of worms that need to be routinely expelled from their bodies. Similarly Blood Parasites is another big category– Animals get bitten a lot by different types of ticks and fleas.

New product introductions is a continual process. We added one new Analgesic product. We are adding one product in muscle growth category. Till now we had been only addressing API requirements for mammals. Now we are looking to introduce five new Poultry products.

Business Evolution/Product Opportunity Choices

NGL Finechem enjoys a profitable niche today. Kindly elaborate on business/product choice philosophy/process.

The kind of product selection you see today started off by chance. In 1981 we were making pharmaceutical APIs like Erythromycin. Till the late 90’s we were into Human APIs. These were primarily 2-step, 3-step process chemistry with low/vanishing margins. The business evolved gradually. In 1997 a Dutch company asked us if we could manufacture a 8-stage-synthesised complex chemistry product. It was our first veterinary product that we delivered and it was very successful.

This was totally different to what we were doing till 1997 – dependent on bulk traders – a different customer set. We started to develop new set of client and product profiles – exploring synergies around customer needs. It took a long time. Gradually customers started asking us for new products – most of which were earlier manufactured in European Union.

In 1997 we had 1 product and by 2007 we could offer 6-7 such products. By 2017 we are now offering 22 products.

What will be the share of complex chemistry products in the 22?

Most are 7-8 stage synthesis complex chemistry products (higher scope for value-addition). Some are 3-4 step products. We have developed the process chemistry for all products in-house.

You enjoy high profitability margins. How do you go about choosing product niches?

Whenever you start a new product, you are never the best at it. You become better, more efficient (process chemistry), with time. We don’t go by margins to start with. We have never chosen a product from market size/profitability analysis. Volume products usually see high competitive intensity. We have consciously chosen a low-volume niche game – products which we can make well and sell well. Every year while working on new products we need to also focus on improving process efficiency for existing products.

Markets/Customer Segments/Evolution

Can you please elaborate on the sell-well philosophy?

First we need to be able to make the product efficiently. Then we need to treat our customers well. No false promises. Be able to fulfill in the quickest possible time. Be transparent in pricing – we have actually passed-on price discounts to our customers on occasions where there is a big benefit. We have done this on 3 occasions till now. We always strive towards developing long-term relationships with our customers.

Could you give us a sense of how Customer Segments has evolved?

15-20 years back we were 100% dependent on traders. Today contribution from traders will be less than 10%. Traders are bulk customers and would order in Tons. Today we serve about 350 customers directly. Ultimate customer requirements would be in 50Kg to 100 Kg lots – but with higher profitability. We serve 4 of the Top 10 global customers. All customers from 1997 are still with us.

How easy or difficult is it to access/address top global customer requirements?

To address a top customer it can take anything between 2-4 years for first sale to happen. It took us 4 years with our largest customer. The requirements have become stiffer and takes longer with Customers now asking for 3 commercial batches versus lab sampling earlier. One now needs to provide stability data also. Most common requirement is 6 months accelerated study. And Customers will then perform their own checks. Our facilities are audited every 2 years. 40% of our Sales are to EU customers – but for Sales in other un-regulated markets.

You seem to be focusing only on un-regulated markets? The rationale?

At this stage of our business size we are content to play in un-regulated markets. We find there is enough scope in the medium-term for our product range to scale efficiently, and profitably in these markets. You see the cost-structures for a regulated market entry is much higher. It is not only the registration/filing costs; one cannot serve both regulated and un-regulated markets from the same factory – cost-efficiently. The investments in manpower, equipment, testing also are of a higher order.

If regulated markets are growing at 6-7%, how are unregulated markets doing?

Un-regulated Markets are growing at a much faster rate. What happened in India in the 80s is getting replicated in many countries. Every country/government is encouraging and providing incentives for local manufacture. To give some examples – In 2004 when we first went to Columbia, there were only 10-12 companies, today there are 300-350 companies. Bangladesh had 20-25 pharma companies, today there are 500 pharma companies, 20-25 are veterinary companies. Most of these companies are making formulations – they need APIs from quality and efficient suppliers like NGL.

What would be the addressable market for NGL’s current 22 products in unregulated Markets?

Difficult to put a proper figure here without published data. But should be around ~1000 Crores.

Nature of Customer Contracts. Proportion of long-term contracts versus SPOT orders?

Typically Customer relationships are all long term in nature. As mentioned before all our customers from 1997 are still with us. However most orders are on SPOT basis. There are couple of products for which we do contract manufacturing for which contracts are long term in nature.

NGL Management Q&A Feb 26, 2018 - Happy to have the opportunity to present a Management Q&A after a long gap. Complete Q&A available here

Disclosures:

Ayush Mittal – Invested; No transactions in last 30 days

Donald Francis – Tracking; Not Invested

70 Likes

Will the revision of Q2 and Q3 Results https://www.bseindia.com/xml-data/corpfiling/AttachHis/20831cbb-d2cb-40c2-b699-1886f6d92fd3.pdf due to the ‘inadvertent error’ in computing depreciation have any impact on your assessments?

Bit outdated: https://www.indiainfoline.com/article/print/capital-market-analyst-meet-agm/ngl-fine-chem-116120900262_1.html

1 Like

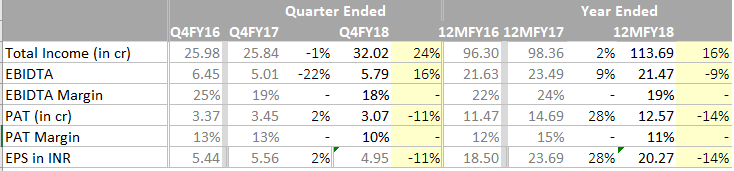

FY18 & Q4 Results:

Net block has increased from 26Cr to 56 Cr. Increase in raw material and employee cost ha s put pressure in the margins.

1 Like

Operating margins are pretty good…the drag is due to increased costs like employee exp, depreciation and other fixed costs probably.

8 Likes