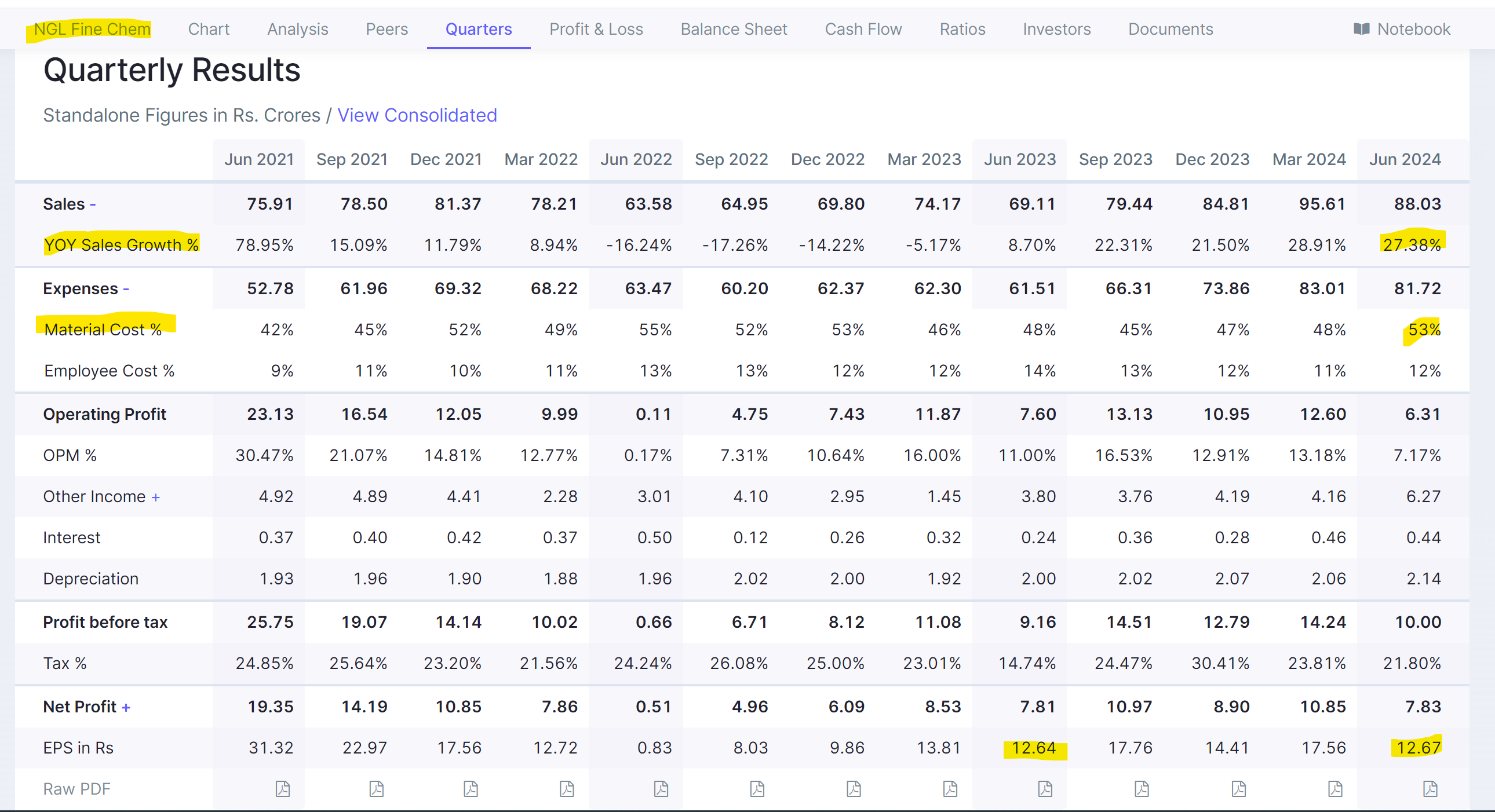

NGL finechem now have two consecutive quarters of comparatively better results - after a prolonged phase of subdued revenue and margins. Specially, FY23 had been a tough phase for company, both top line and margins took serious beating.

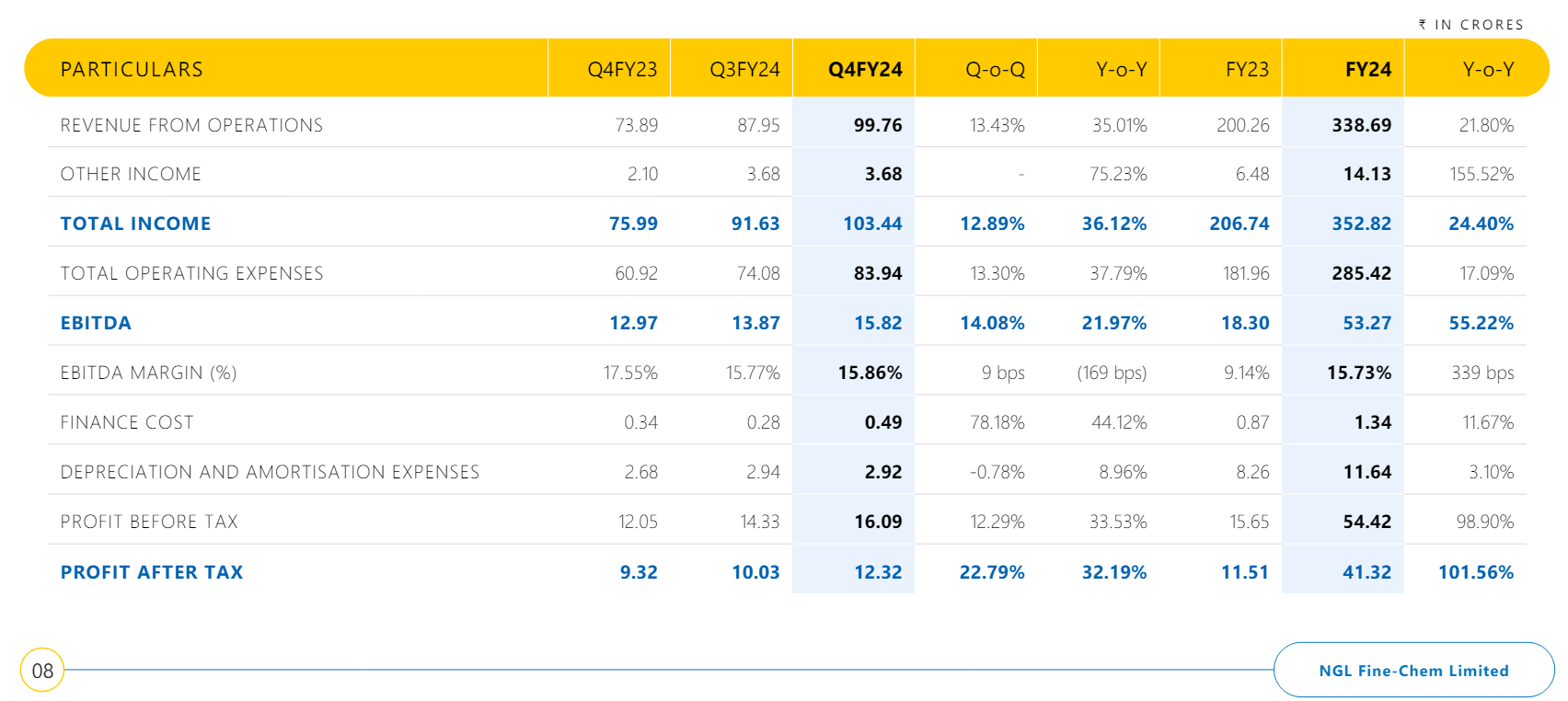

For Q3FY24, on a consolidated basis:

- 22% Y-o-Y revenue growth | 10% Q-o-Q revenue Growth

- Y-o-Y 67% Net Profit growth | flattish Q-oQ net margin growth.

- Operating margins in the range of 16% (have been in the range of 20% - 30% in recent times except for FY23, which really had been tough for company)

Some noteworthy excerpt from recent investor presentation:

In light of the promising signs of demand recovery, we are accelerating our CAPEX plans, aiming to complete phase 1 by the end of Q2FY25. With an investment of ₹75 crores earmarked for this phase, of which ₹45 crores have already been invested, we are laying the groundwork for capacity expansion. Phase 1 will see the establishment of all necessary utilities for the entire CAPEX project and the operationalisation of one clean room (API line), setting the stage for further expansion.

As we plan for the completion of phase 1 and look ahead to phase 2, which involves making the remaining 5 clean rooms operational by December 2025, our financial strategy remains focused on prudence and sustainability. The total project cost is maintained at ₹140 crores.

To date, we have invested ₹45 crores in the CAPEX, all through internal accruals. We anticipate

investing an additional ₹25 crores from internal accruals into the project, covering both phase 1 and phase 2 activities. This approach underscores our strategy to increase the proportion of internal accruals in funding this CAPEX, while also acknowledging that some level of debt buildup may occur from Q1FY25 as we advance our expansion plans and strive to meet our

strategic objectives.

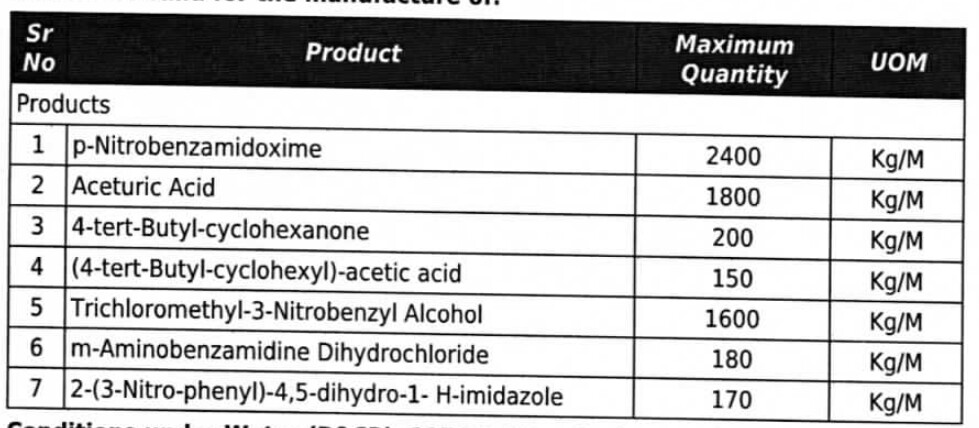

As per most recent EC reports, below are the products for which they have got Environment clearance approval. This proposed expansion will increase capacity by 50%.

Margins inching back to 20% levels with expanded capacity kicking-in over next 2 years can be interesting.

In the Annual report for FY23, they have mentioned about European CEP filling for three products namely Triclabendazole, Flunixin Meglumine and Marbofloxacin. This is interesting development. So far they have been rather conservative in going after developed/regulated markets.

- Triclabendazole appears to be a low competition space with approval granted to Alivira Animal (100% subsidiary of Sequent Scientific) and Rakshita Drugs only.

- Marbofloxacin - 5 approved CEP players. Wisdom Pharmaceutical, Aurore Life (Originally M/s. Konar Organics Limited) and three different entities belonging to ZHEJIANG group China.

- Flunixin meglumine appears to be little crowded with 7 approvals so far.

Filling for Triclabendazole in Europe can be particularly noteworthy. Triclabendazole falls in the family of Benzimidazoles class of Anthelmintics. Other significant drugs within Benzimidazoles class (where NGL is not looking to EU market today) are:

- Albendazole - Only two valid approvals. Sequent scientific (capacity must be ~80MT/M) and recent entry of MSN life science.

- Fenbendazole - Three group of companies has European approval. Shaanxi Hanjiang (China), Jiangsu Baozong (China) and Sequent Scientific.

- Oxfendazole - Only three approved players. Jiangsu Baozong & BAODA (China), Shaanxi Hanjiang Pharmaceutical, and ALIVIRA ANIMAL (Sequent Scientific)

- Mebendazole - Only three approvals. Changzhou Yabang-Qh (China), Shaanxi Hanjiang Pharmaceutical (China), and MSN Life India.

As of today, we dont have visibility if NGL is going for the other APIs excpet Triclabendazole for Europe. However from adjacency perspective, can be interesting opportunity for two reasons- a) they now have filing for Triclabendazole for Europe. b) each of the products within Benzimidazoles class of Anthelmintics has low competition intensity for European market

Tarun

Disc: Invested, no transactions in last 60+ days