The sales growth is marginal.

This specially when last year sales were affected due to covid.

Profitability has increased significantly primarily due to curtailing of SG&A costs.

If you go through their quarterly presentations, you will find that they are two primary challenges

Their sales growth has been low in the last two years. In 18-19 some india PSUs merged and they lost some big deals. In 19-20 there was covid in last quarter. In 20-21 there was lockdown on first quarter.

There is always a reason but underlying thing is that their sales haven’t grown. This in an environment where all other companies have been Ble to sell digitally.

Their customer churn has been high. Their annual active clients have been in the range of 550-560 in the last 2 years even though they are adding 50-60 new clients every year.

The business model has potential and is scalable. The only question is sales growth.

This is the same problem that faced intellect design arena and they turned it around brilliantly.

Companies response on sales growth is ( from conf call)

They are hiring more sales people.in developed economies. This is yet to kick in

They are focusing on saas sales in usa which has more upfront cost and lower initial revenue but longer lifetime value.

They have tied up with global system integrator a for selling together. This has resulted in some sales this year but will get traction in coming year.

Disc: invested from lower levels and bought more during covid dip.

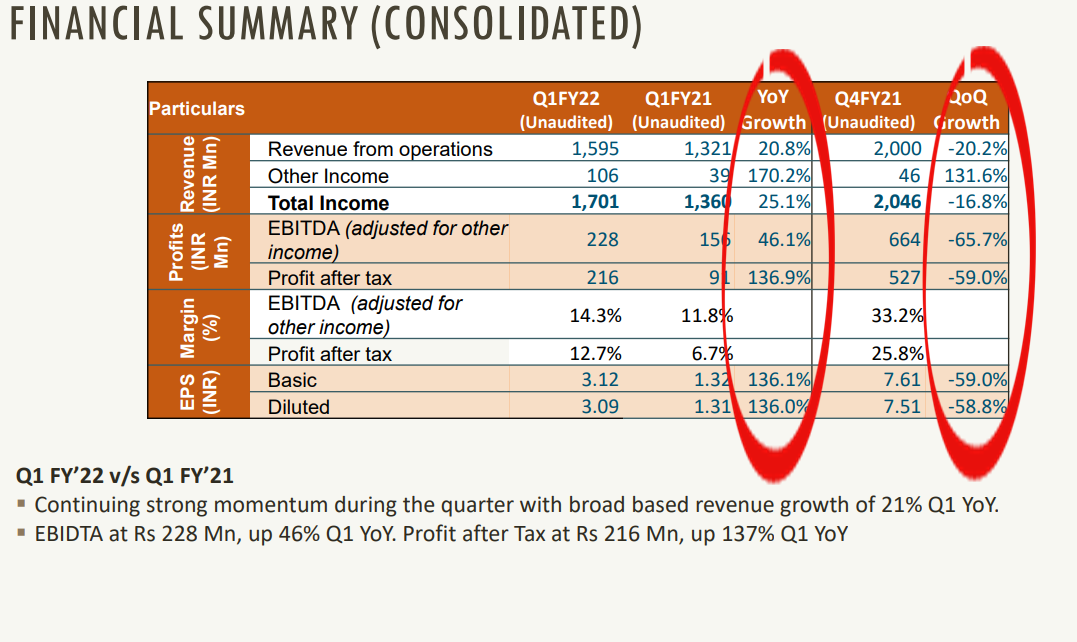

a few things to look at - YoY good results, by QoQ its been bad.

There is seasonality to this business on a quarterly basis, so one has to be cognizant of that it can be lumpy.

Studied Newgen. Liked the potential of underlying industry growth here & Newgen’s positioning to capture it. Don’t want to write a full thesis, just wanted to highlight a few key points.

SI tie up efforts to play out in medium term revenue growth – One of the key reasons revenue growth can accelerate and be on the higher side, say 20-25% cagr, is due to the last few years efforts(already done) of tying up with system integrators. Think kpmg, E&Y, accenture etc. They are the ones who have a richer relationship with large clients, who really help in getting an IT products co, business. Went through the last 3-4 years transcripts of peers Appian corp, Pegasystems. 1 clear point which stood out was, Sis you really need them if you want to grow significantly, esp when it comes to getting large deals or traction with fortune 500/2000 cos. Interestingly, Appian has been getting majority of new business from SIs, whereas for Newgen its only 20%. Their scale is 1/4th of Appian, and so far they gotten business from their own direct sales force. Given the revenue growth potential from Sis over the next 3-5 years, growth rates can be material perhaps. Appian corp: “Partners delivered more than 70% of our new logos for the year.”

“Partners continue to be a larger part of our ecosystem and are increasingly helping us sell more software.

“I’m happy to give our partners credit for the increase in net new logos. I think they deserve it, and they’re going to be a powerful engine for us in adding logos going forward.”

“And we eagerly turn that over to the partners who give us the complementary skills that we require, the access, the credibility, the reach and the strong team of trained service providers that dwarfs what we are capable of fielding ourselves.”

“Partners helping us get business going very well. They’re creating IP, they’re making the pace. They’re carrying the deals for a lot of the – they’re doing a lot of the heavy lifting. And the results are so promising and I now consider this to be one of our best up-and-coming verticals. That’s an example of the kind of help we’re getting today from partners, the kind of win-win they’re seeing working with us. It’s of a different league than we saw even 12 months ago.” Pegasystems:

“We had relationships with our partners over the years, but more in an execution way. They did the implementations, they were the global system integrator, they had Pega-certified resources, we worked well with them, but not in a selling capacity. We never went to an Accenture, for example, as just one example of a partner and actually said, hey, we want to be – we want to work together on actually opportunities where Pega and Accenture can actually help our clients. Same thing with Cognizant, with Capgemini, with Ernst & Young, go through the list of those. Those SIs have tremendous relationships with our clients. In many cases, they are better relationships than we would ever have because they’re living with those clients and helping them on their digital transformation.” Newgen:

“have also entered into global strategic alliances to further expand our partner network.”

“see possibilities of accelerated growth in acquisition of new logos both directly as well as through partners”

“the other most important driver for us is to build the global partner ecosystem, most of the product companies beyond a size of $100 to $ 200 million do grow strongly through a partner ecosystem and that is what we are investing in and we hope that in the next 4 to 5 years”

“GSI very small part of business, coming in few next three years this can be a substantial part of our business.”

“Why are GSIs partnering with us: it is true, GSIs traditionally they have been carrying products, the ones we have, like, they have products from Appian, Pega, Open Text and they have been caring to these global customers. What has changed over a period, first of all, organically over the last five, seven years, we have generated a lot of success stories with the GSIs on different accounts across the globe. So, their confidence in our product and platform has really grown. We have excellent success cases. Finally, the GSIs also are looking at a great piece of technology. But beyond that, they are also looking at the customer success, because they have a surety that the use cases will get fulfilled. So, what are the happened, as a part of that our relationships have really grown. So, we are concentrating on four to five GSIs where we are having more strategic tie ups when they are taking our products to their practice areas, having kind of sales targets on our products. And now why should they take our product vis-à-vis competitors? You know, as Mr. Nigam clarified in his call, because of the value proposition. We are one of the few players who have multiple products from the same stable build on the same platform and technology which are used in a single digital transformation case. So, what happens is, the complexity for the end customer and the GSI drastically reduces, and thus their cost of ownership. Very, very compelling value proposition. And it’s not an easy journey to say why GSI would take our product, but I think the hard work has been done over five, six years. Now, we are seeing the green shoots of that, what we have invested over five, six years with these GSIs, building the credibility. So, we are one of the few companies who are consistently in Gartner and Forrester Magic Quadrants, that gives the comfort both to the customer and the GSI.”

TAM & the potential of Low code market growing as a tailwind for Newgen– The biggest issue for us investors to study IT cos is, since most of us don’t have an IT background, we really don’t have a sense & feel for the products. Figuring out opportunity size (actual one, not a random blown up over the top figure), competitive positioning and market share is easier said than done. Newgen:

“we have shown a continued performance of around 20% growth rate over last many years. I think organically we have been able to do that and with our push in mature market and the GSI initiatives, we are expecting to even push it up higher because for our business, the availability of market is not a challenge. So we think the addressable market especially with the Low-Code initiative and the interest in digital we think the growth in overall available market is going to be high. So we do expect that we can even push it up than our traditional growth rates.”

“Addressable market - overall addressable market of the ECM, BPM and CCM which are the traditional product line which are very well tracked by Gartner and other guys. = $20bn. 7-8% cagr. but the Low-Code initiative which has been the recent take on the digital companies, I think that has expanded the market size to a much larger. Cant quantify but as big as $60 to $200 billion additional market” Appian corp:

“The profile of low-code has risen substantially over the past year for reasons we’ve discussed on previous calls. Forrester predicts that 75% of development shops will use low-code platforms by the end of 2021.”

“The macro answer is we’re a 30% grower. And I don’t want to indicate that I expect anything other than that”

“The TAM, as you guys know, no matter how you slice it, is massive.”

“at 2020 and you say, well, that’s the year that low-code took off, low-code is a thing right now, it’s a thing in mission-critical applications” Pegasystems:

“TAM - look at a company like Salesforce, they’ll tell you that the market – that their TAM right now is over $100 billion, growing to $200 billion, just round numbers, right? It’s large. I mean they have something like 25% of the market share of the markets that they’re in, right?

So when you look at our markets, we’re – our TAM, we don’t have the same addressable market that a company like Salesforce has. Remember, they’re getting that data from IDC, from Gartner, from Forrester. They’re not making that up. They’re getting – same sources we go to. So what we did, we went to those same sources that all of our competitors go to. But we focused on the organizations that we target, which tend to be the larger organizations in our core verticals. When you – with just quick math, that kind of cuts the market down by 30% to 50% in terms of the TAM of what you might see from a company like Microsoft or Salesforce in terms of what they could address because we don’t go down market, we don’t sell to every single organization, we don’t sell to every single vertical. So we try to be realistic about the fact that our TAM is something like $60 billion, $65 billion, $70 billion, growing to over $100 billion. Now the reason why I gloss over that sometimes is we’re $1 billion, and we’re talking about a TAM that’s approaching $100 billion. So for us to double our business really isn’t even scratching the surface on disrupting or cannibalizing the market. That’s the reason why I don’t get into a lot of science around sizing. It’s so large that there’s plenty of room for us to double, triple, quintuple our business over – in the coming years. So I think we’re – that’s really not the restricter. The restricter is us executing, right? We just need to execute well. I think the market is plenty big.”

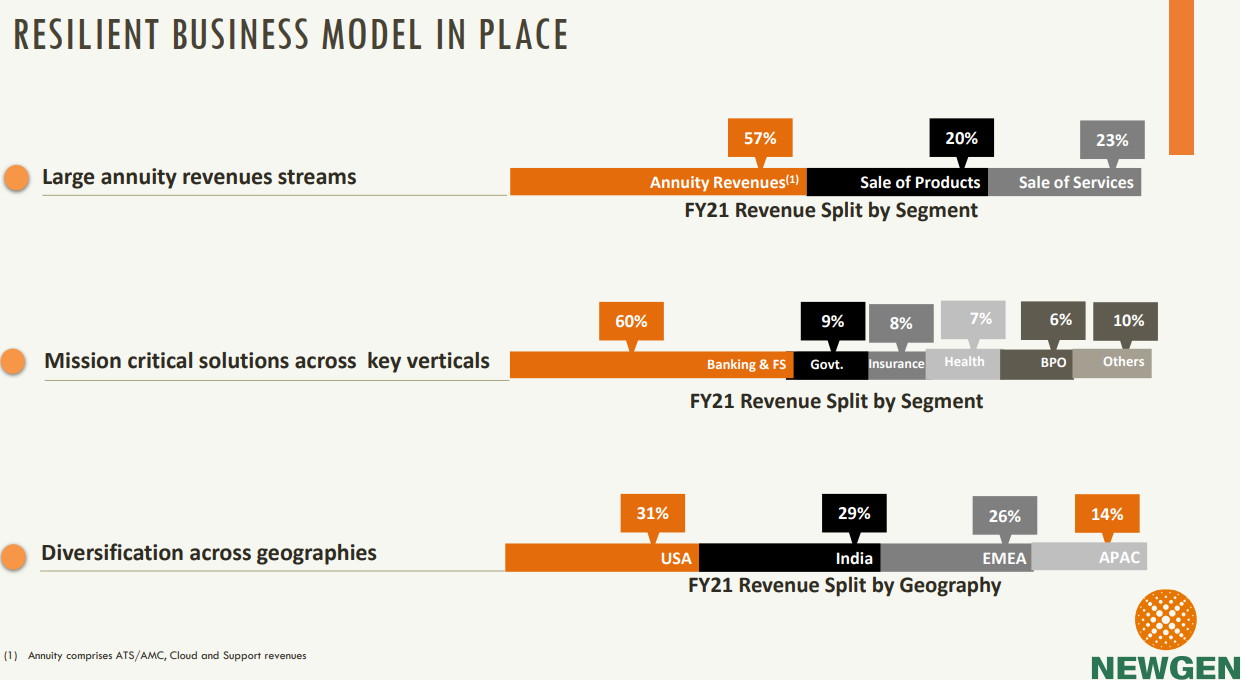

Competitive positioning – read a bunch of gartner & forrester reports (available in plenty on Newgen & peer sites). Really helps in getting some sense on strengths & weakness for each co’s product. After seeing no of reviews, rating score, comments in reviews, number of competitors on list – Newgen seems decently placed, I would categorize in a mid to upper tier vs peers.

The 2 traction points are a well-integrated product suite (organically built, peers have often used acquisitions to fix gaps, however this leaves room for integration failures & frustration for the client) + value for money offering (cheaper offerings, price competitive). Weaknesses mentioned are limited presence in mature markets + lack of a developer ecosystem.

Making headway in mature markets + tie ups with Sis is the way forward for Newgen to get stronger and scale up.

Interestingly, on checking employee reviews, its clear most mention an outdated tech stack for Newgen. This is a negative, and one needs to keep tracking industry reports from Gartner & forrester for Newgen’s positioning on its product vs peers.

Management has already mentioned that they get paid differently for different market they are operating in, So best measurement would be to compare Quarterly results YoY.

Once Newgen shift their model more to SaaS revenue will get stability.

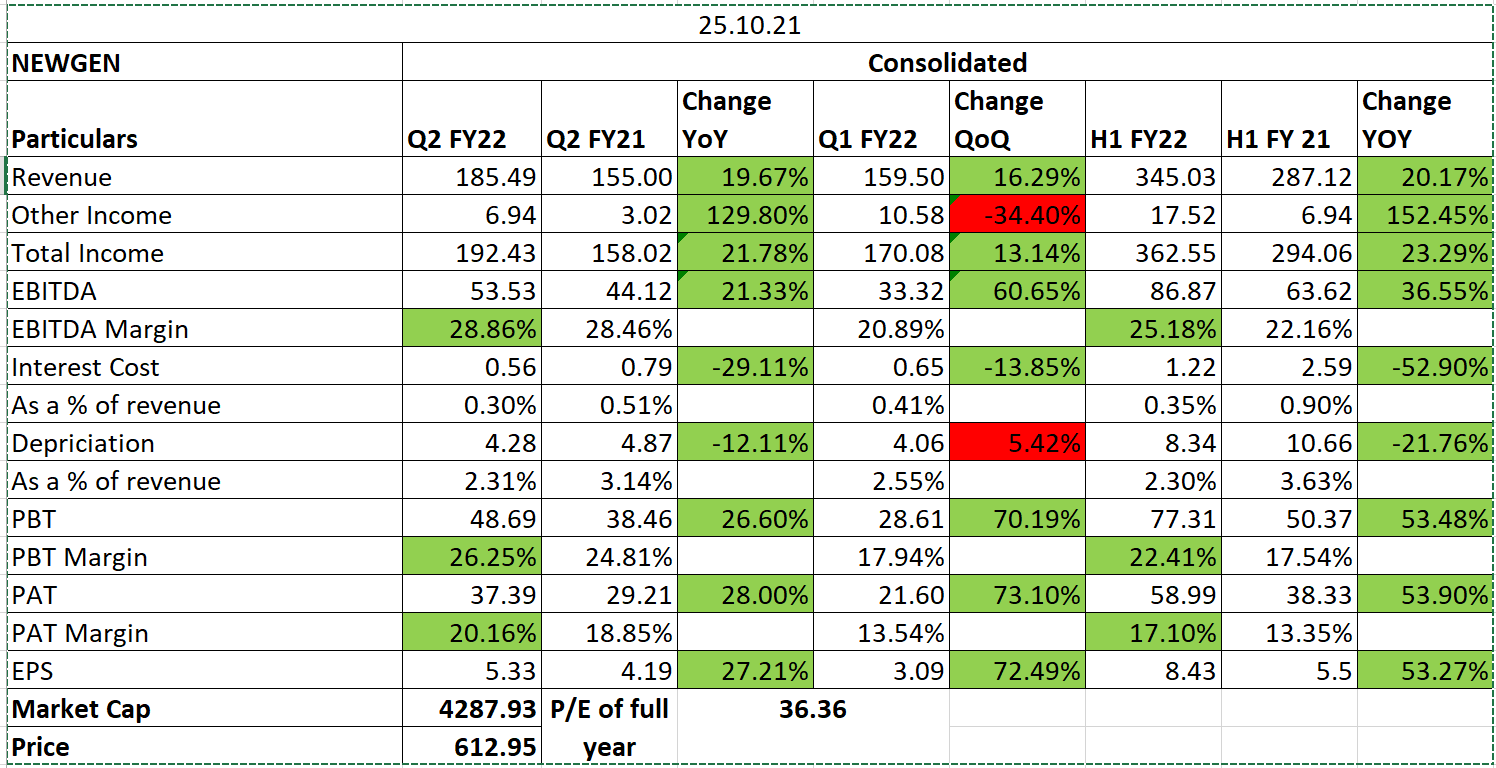

The Q2 result seems good both on YoY and QoQ parameters but the stock price has not moved accordingly. Infact its falling. Anything that i am missing which can explain this reaction to the stock price ?

There has been a lot of movement in the promoters shareholding recently. BSE website shows sale of significant promoter stake in June-2021. Should this be of any concern to investors?

The promoters sold shares to a group of private equity investors last quarter.

At current prices and valuations the current year earnings are already discounted 27 times. When the earnings roll forward to next year in Jan22 or there is an earnings surprise in second half the price move may happen more suddenly.

This company is getting combined with the conventional IT services pack whereas it should be treated as a product firm where valuations are slightly different.

Another trigger is when the market cap crosses 5000 crore more broking firms will cover it.

Promoters sold stakes directly to PE firms and Mutual funds. Mutual funds had recommended promoters to sell 10% of stake to increase the float in the market so big fishes like mutual funds can buy big quantities. Promoters want to use money philanthropy and other personal finances.

Yeah could be. And since results have been good, guidance for Q3/Q4 is also good, ASM is a transient phase which does not reflect anything about company fundamentals, i think Newgen provides a good risk reward at this CMP. Whats your view ?

Being a product based company, at the current juncture, they need to keep on innovating. Looks like management acknowledges it.

Investment on R&D (as a % of revenues) has grown consistently from 7.3% in 2017 to 9.8% in 2021.

It will be interesting to watch if the co. can regain the profit margins > 30% in q3 & q4.

In the next 4-5 years, they will have a very high margin as they will start getting the max revenue from SAAS. Compared to the license-based model, initially, SAAS revenue may seem less, but as time will pass, they will have a higher margin and higher revenue.