https://www.neulandlabs.com/sites/neulandlabs/files/neuland-labs/insights/resources/esperions-case-study.pdf#:~:text=Following%20FDA%20approval%20in%20February%202020%2C%20Esperion,the%20active%20ingredient%20in%20NEXLETOL®%20and%20NEXLIZET®.

Neuland is gradually establishing itself as a reliable and efficient CDMO partner for late Phase 3 drugs. The above 2 drugs that is KARXT & Bempedoic acid are estimated to be blockbuster drug. Company is now partnering with big pharma also. All the above things give a lot of optionality to the Company going forward. Any serious investor before taking any buy or sell decision should sincerly go through the last 2 years concal to have a better understanding of the Company and about how it is evolving.

Summary of Concal: (Worth reading every single sentence)

Q1 poor performance was designed to happen and it will not have any impact on future growth:

• As you can all surmise from the numbers, the performance has been below par for this quarter. And through my commentary, I do wish to assure you that we are well on track for achieving both our short-term and long-term goals.

• We had previously indicated that we expect our FY26 growth trajectory to resume on the FY24 base, and despite a weak start, we remain confident of achieving this objective.

• Coming to the quarter’s performance, which has been below par in terms of our performance over the last few years because of the flow of customer orders. However, this is in line with our earlier stated expectations on the increase in revenue to pick up during the course of the financial year. And I guess the orders were planned in a way that the quarter itself was always set to perform in the way it has. This quarter doesn’t change our earlier stated expectations for the financial year as well as the following years.

• I think, we don’t want to give that classification, but I think definitely this year, next year, I think the CMS growth will be quite strong. Strong growth is the word that we are leaving you with.

• While FY25 was a year of consolidation and Q1FY26 has been a continuation of that, our customer pipeline gives us good visibility. Hence, we are confident with the commercialization of Unit 3 production block. It will give the business greater revenue momentum from the latter half of FY26. Overall, we continue to be optimistic about our future and the potential that our business holds.

• See, I think what we have said is a couple of things. One, we should look at a 3-year perspective. Second is, we have also mentioned in the past that over 3-5 years, 20% CAGR is a reasonable number to look at for a company like Neuland and the kind of phase that we are. But yes, I don’t want to connect the words with a number. But yes, we expect to see a strong growth in FY26 as well.

Strong recognition as CDMO player and demand going forward:

• We continue to see increased interest in customers wanting to partner with Neuland as they look to bring in their innovative medicines to patients. I believe this can be attributed to 3 main factors.

Firstly, our reputation has been growing steadily due to the work we have done over the past couple of decades, particularly in the CDMO business.

Secondly, our business development teams are increasingly focused on finding opportunities that align with our long-term strategy, making us more selective and decisive about our partnerships.

The third factor being the macroeconomic environment being favorable. Of course, this is a rapidly changing scenario, which also has worked in our favor. We are excited by the range of customers expressing interest working with us, which gives us great enthusiasm for the future of our business.

• We are also seeing significant growth in terms of new business coming from both existing as well as new customers, which should fructify in the numbers over the course of this and next financial year.

• We are also excited by the range of customers expressing interest in our services and placing first-time orders. Apart from commercial projects and the new business, we are also seeing some of our customers assets in the pipeline make progress.

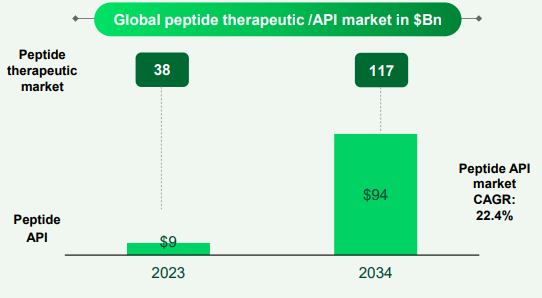

• As stated in the past 2 quarters, our peptide investment plan is on track. We continue to garner more projects in this space, which further validates our excitement about the opportunities that the segment holds.

Peptide development and future opportunities:

• Our peptide scientific team is working on exciting projects,at the same time, they are also developing capabilities that will help Neuland further differentiate itself as a peptide API manufacturer.

• I would like to conclude that Neuland is well positioned to capitalize on long-term opportunities, and we are also positive regarding the outlook for the year.

• Neuland has been dabbling with peptides for almost 17-18 years now. We have had a small group, mostly working in small scale and then in pilot scale and now with this new investment, we wish to embark on large scale commercial manufacturing of peptides. The hypothesis for us has always been that, look, we are present in peptides. We understand the chemistry and the techniques of peptide chemistry. However, we never had the large scale infrastructure.

• I think what makes Neuland a strong player in the peptide space is the 15 plus years of experience we have had in peptide chemistry. If you look at the IP landscape, the number of patents filed by Neuland scientists over the years, the kind of work we have been doing, not just in terms of peptide APIs, but in peptide fragments, etc., I think that creates layers of depth of expertise that I believe Neuland uniquely has, at least from this region. In the space of peptides, techniques become that much more important than just knowledge of chemistry because when it comes to executing peptide projects, there are a lot of techniques, whether it is purification, lyophilization, precipitation, or different techniques, which are very difficult to achieve and apply to projects. Companies that have years of experience, especially even on the large scale, they tend to do well and we believe that is what gives us the advantage. What was the limitation for Neuland, frankly speaking, was that we never had the large scale capacity. Even before 4 or 5 years ago, we had been approached by biotech companies for making commercial peptides, but we could not fulfill those projects because we never had that scale. But now with the creation of this capacity, we are very confident that our business will grow., but I also do believe that there is enough space for multiple players to do well, but you do need strong R&D capabilities in peptides. Just having infrastructure may not be enough.

• So we have several CMS molecules, some as late as Phase-3 and several in earlier stages, which are peptides. And they are part of our portfolio and they are also part of that table that we keep disclosing every quarter in CMS.

Working with Big Pharma and efficient Capital allocation:

• It is an interesting question. I think to work with Big Pharma whether it is for early stage or late stage, I think building those relationships require time and they require certain kind of infrastructure capabilities, etc. I think as we have always mentioned, Neuland has traditionally worked a lot with biotech companies. Even today, most of our pipeline comes from biotech companies, not a lot comes from Big Pharma. I think Big Pharma work is either coming through peptides or when a biotech company is getting acquired by Big Pharma. So frankly speaking, we don’t have a lot of experience to speak about what it takes to convert Phase-3 projects from Big Pharma. But our approach has been to kind of keep investing in capabilities, infrastructure, which we have been doing and engaging with Big Pharma for unique technologies. So for example, Neuland is in contact with several Big Pharma for areas of peptides or deuterated molecules because these are capabilities that Big Pharma does not find from their traditional API suppliers. And in that pursuit, we are looking at some early stage projects. We are occasionally also finding opportunities on the late stage, but it is really too early for us to comment on whether they will fructify to business or not. But yes, I think Big Pharma is a very important target segment for us. And there is a lot of effort for the medium to long term to build large businesses with Big Pharma and I believe we are making good progress.

• I would say directly it is not because even in Neuland, if you see, we have been investing in capacities ahead of the curve.

• And if a Big Pharma or any other client were to have a project, I think they would find capacity in Neuland. So I don’t think that is directly a concern as of today. But yes, perhaps 2 years ago, 3 years ago, maybe we would not have that. But what we also see mostly is whenever you engage with any biotech or Big Pharma, unless it is a late life cycle opportunity where there is old molecule which is nearing patent expiry, a Big Pharma is not really looking for huge capacity straight away to be available. We have seen some opportunities slip from us because some large, big companies have looked for large volume APIs which are nearing patent expiry for which they needed some ready capacity. And I believe we have lost one or two of those opportunities. But again, we also feel from a scale chemistry point of view, those are not really great fits for us. The way we have been building our business is to start partnering for molecules which are late in the clinic or in the middle of the clinic or maybe early commercial. And for those kind of opportunities, you really don’t need to showcase so much capacity ahead of time. You need to show your ability and bandwidth as a company to create appropriate capacity in time for the scale up of the molecule. But more importantly, you need to show the technical capabilities for handling the process and designing the process which we have. So it is a very finished approach where we need to find the right kind of project. And I think Neuland as a company, although we want to work with Big Pharma, we are also very careful not to approach Big Pharma for the wrong kind of projects because then we would end up competing on capabilities which we are not very strong at. So we are very careful in that approach.

Lumpiness to reduce going forward

• But at an aggregate level, because we have a small pipeline, and these pipelines are contributing to the growth, and this pipeline is young, we are seeing this lumpiness, but if you go fast forward maybe 2 years from now, 3 years from now, I do believe, and at least instinctively, that this lumpiness should come down. You should not see the kind of swings that you would see when a company or the business is at a smaller scale.

Conclusion:

1. Top grade management.

2.Efficient capital allocator.

3. Walk the talk management.

4. Optionality developing in the business.

5. Established and reputed player.

6. Capital and Capex is in longer a constraint which used to be 3-4 years back.

7. Net zero debt Company.

8. Strong cash accruals and free cash flow to take care of growth CAPEX. Annual CAPEX of Rs around Rs 300 Cr can be done annually without any incremental borrowing. .

9.Consolidation period is expected to get over.

10. Strong growth guidance given by the management.

11. Sector tailwind.

12. Long runway for the business.

13. Clarity of thoughts.

14. Execution capability.

15. Established compliance culture thereby successfully clearing various audits without any major observation, which is one of the most critical requirement for any Pharma company.

16 Decadal experience with focused approach.

17 Volatility in earnings/lumpiness to reduce going forward.

18 Growth in business with improving margins showing quality of business

19 Balance sheet can be comfortably leveraged to increase the CAPEX growth.

Disclosure: Invested and view are fully biased