Disappointed with the results, the pace of sales growth and pat seems to be lowering, already down from 40 to 30. At this valuation, we can get better opportunities. Let’s wait for the concall tomorrow for the guidance and management way forward

2 Likes

Netweb Technologies | Management Interview

![]() Our orderbook stands at Rs 360 crore’

Our orderbook stands at Rs 360 crore’

![]() Company maintain 30-35% CAGR annual revenue growth target

Company maintain 30-35% CAGR annual revenue growth target

Watch here - https://youtu.be/tw6juHs6uWc

2 Likes

The proposal restricts export to less than 1,700 GPUs per company per year in Group 2 countries.

India falls under Group 2, so how will Netweb make AI servers with only 1,700 GPU/Year?

Read more at:

2 Likes

Guy keeps on repeating the exact same sentences every quarter. Keeps maintaining lower guidance despite faster growth in each of the previous quarters. (Why?) I haven’t calculated it this time, but in previous earnings reports his revenue seems to fall short of the numbers he shows in his pipeline/L1 from previous quarter. When asked why, he says that payment cycle is long so payments happen in next quarter. And even this payment cycle duration he keeps on stretching in each concall. Honestly doesn’t give me confidence.

Due to competitors like HP, Dell and other big players, I personally don’t find any competitive advantage in this. Waiting to see what they do with the tele-comm product which is under development. Did they announce any thing about it this time? I haven’t yet heard the concall.

Not invested. Had taken small quantity earlier for tracking purpose and exited that too.

4 Likes

News item form today’s Economic Times. I quote “India won’t be able to import more than 50k GPU in a year”.

In yesterday’s concall investors/analyst asked the management twice about the impact on the company due to these curbs and they replied company remains unaffected by exports curbs. At the same time they said they will launch Nvidia GB200 chip along with global peers.

They didn’t provide any definitive answer as to how they will procure the chips when exports curbs are in force.

I am really doubting the quality of this management now.

2 Likes

I see many people mentioning that they don’t have tech people on board. But if you take a look at their DRHP, they do have some resources which are engineers and experienced. Can talk about their real abilities, but it would be incorrect to say that they just have commerce and finance people in team.

We have dedicated R&D Facilities which, as on May 31, 2023, comprised a 38 member technically skilled R&D team

all of whom are professionally qualified. Our R&D team is led by Mukesh Golla, Chief Research & Development

Officer, who holds a bachelor’s degree in technology (computer science and engineering) from the Jawaharlal Nehru

Technological University, Hyderabad and has been associated with our HCS since 2004. Our dedicated R&D teams

are based in Faridabad, Hyderabad and Gurgaon, comprising 34, 1 and 3 members, respectively. Our R&D team,

which has 22 engineers, 7 master’s in computer applications, 1 bachelor’s in computer application, 3 science

graduates, 4 graduates in commerce/arts and 1 MBA, constitutes 13.92% of our total workforce. Since April 1, 2019,

our R&D team strength has grown from 12 to 38, as at May 31, 2023.

may be this is the guy that everyone here is looking for : https://www.linkedin.com/in/mukesh-golla/?originalSubdomain=in

I cannot comment much, but one thing I have realized that in IT industry if you are doing one thing over and over again for years, you get expertise in it and that becomes valuable.

For me the bigger concern is that since their work is not deeptech but it is definitely niche and the guys that they have actually might added stars in resumes with good experience in netweb, they may get better offers elsewhere as well. Their attrition as per dhrp is 11.41%, which may be on higher end within IT industry.

Checked their linkedin page. Job functions and positions of ‘people’ is inline with their disclosure in drhp.

Most people are Linux admins, or python developers. But I could not find profiles of senior tech people, most of the people I saw joined in last 2-3 years and some of them are “open to change” for new job.

7 Likes

Excerpt from press release shared by the Management today morning:

- We view the emergence of DeepSeek as a significant opportunity for our business growth

- By lowering the cost barriers associated with advanced technology, it enables a wider range of customers previously hesitant due to high adoption costs—to access and utilize appropriate computing resources

- Our offerings include hardware, middleware, and utilities that seamlessly integrate with end-user applications like DeepSeek

- The Indian government’s current AI policies explicitly emphasize “developing indigenous large language models and domain-specific AI models” as a key pillar. Such disruptions will only hasten India’s commitment to advancing its AI initiatives and allocating resources toward this transformative technology

- We remain focused on surpassing our guidance and solidifying our leadership in the High-end Computing space

8 Likes

Any thoughts on why FII’s and DII’s holding decreased despite of good quarter? Is there something which I am missing?

2 Likes

, Netweb Technologies has

Secured a ₹1,734 Crore Strategic Order to Power India’s Sovereign AI Infrastructure. Media release attached.

netweb tech.pdf (911.6 KB)

6 Likes

Another order received worth Rs 450 Cr for Deployment of AI Infrastructure

facility using the latest Tyrone AI GPU accelerated systems. The point to note is that the execution is to be by the end of this FY. Rs 415 cr was the highest Qtrly revenue ever achieved by the company till date . When the project is executed one can only imagine the revenue in current Q4.

Order Netweb.pdf (306.0 KB)

2 Likes

Hot stock/sector. Crazy run up. Execution remains key risk. Strong volumes but still unable to understand the credibility of the management. Nvidia association is a major boost but little info available. Has anyone done a deeper dive into this company?

2 Likes

The valuations are crazy if one considers the present price. The PE ratio is a mind boggling 180 for today’s closing price. The P/B is even astounding at 43 plus. One should await the Q2 results for taking any buy/ sell decision

3 Likes

While the Q2 results show year-on-year growth, the sequential (QoQ) momentum seems to be missing. Historically, the June quarter has tended to be softer, with a revival usually seen over the following three quarters — but this year, that recovery hasn’t been as visible on a QoQ basis. It’ll be interesting to see how the market interprets these numbers — whether it focuses on the steady YoY growth or gets concerned about the lack of sequential pickup.

20% YoY growth at a PE of 170 is unjustified irrespective of the order book and growth in their AI business. I’m sitting on 110% profits so I’m going to sell my holding tomorrow and wait for a correction to take entry again. It will be interesting to see if the market behaves exactly the way I’m thinking.

Disc- 7% holding in portfolio

2 Likes

while searching regarding the OEM (indian company) the following is shown in

- Preferred Status as Indian-Origin OEM: The “Make in India” initiative encourages government departments and public sector entities to procure from domestic manufacturers. Netweb, being one of the few Indian-origin Original Equipment Manufacturers (OEMs) for high-end computing solutions (HCS), benefits from this preference in securing government and defense-related orders.

Any idea whether Netweb is the only Indian company (OEM) or are there any other listed players?

3 Likes

Agree, the valuations are crazy but it has cooled down now. At its recent top, the price already factored in next 3-4 years growth at 20% guidance.

I am also sitting on 70% profit at today’s price and haven’t sold when at peak I saw 130% profit. Taking it as a long term bet. Looking to add if it comes back to my previous buying levels.

But here is the catch why I am not selling. We cannot predict market behaviour. An ideal market will bring it back to 80-90 PE range but if bull market returns or it secured further big orders which can happen anytime, PE might even go to 500, 600 etc.

Since it’s one of its kind listed company, fundamentally good, management seems down to earth to me, no fancy Outlook…they are more likely to do good in next 4-5 years, so I am not in a rush to sell.

Surely not good levels to enter right now, but if you are holding and in dilemma if you should hold or sell, my take is hold for long term and brace for AI bubble crash in between.

Disclosure - holding at 1800 levels and around 18% of my portfolio.

I own a concentrated portfolio with just 7 stocks, so I have other stocks also with similar portfolio weighing..this is not an outlier

7 Likes

Strong Q3FY26 Numbers

The demand for high-end computing is huge. AI systems now contribute 64% of revenue. EBITDA margins saw a slight sequential dip.

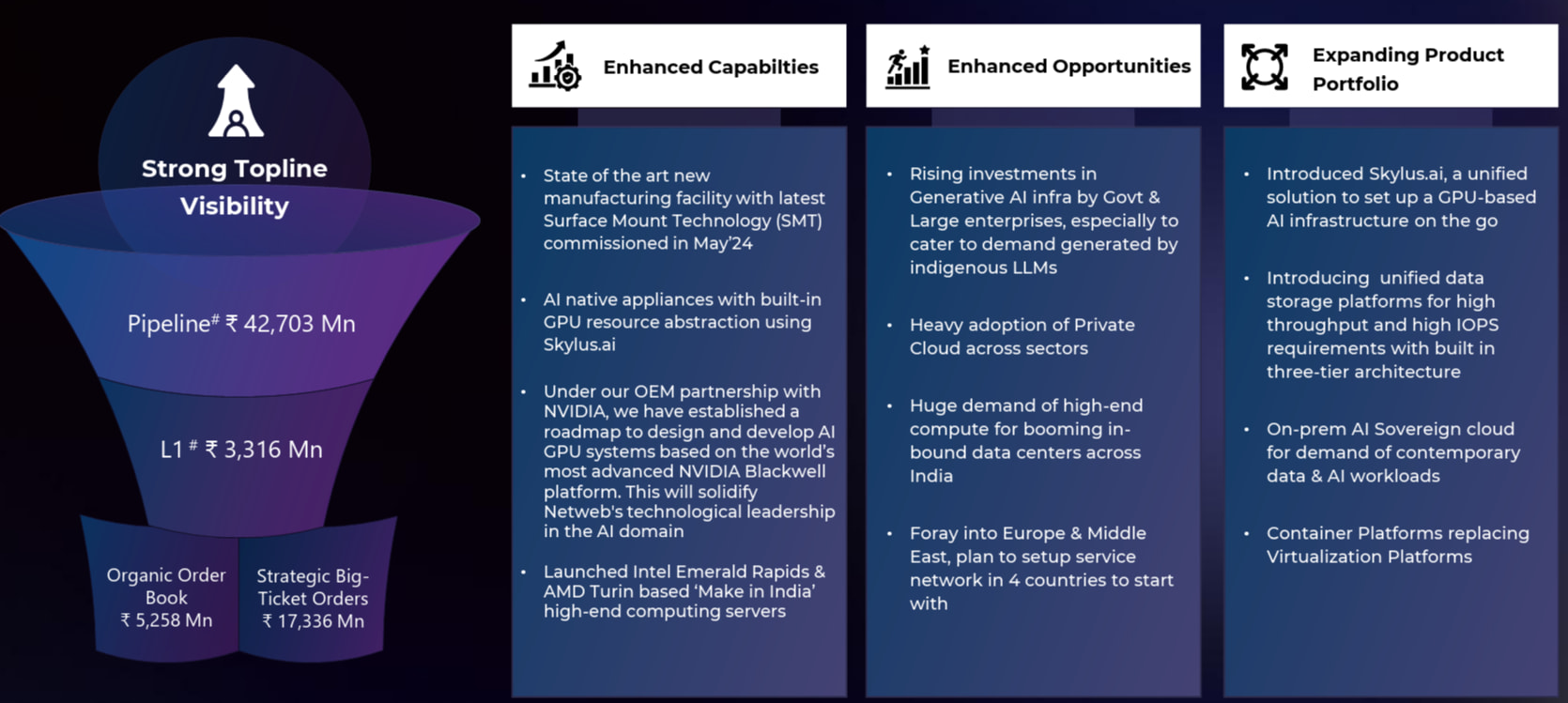

Focus on the IndiaAI Mission. Apart from that, a massive pipeline of over ₹42 million. However, there is a difference between a “potential pipeline” and an “organic order book” (which currently stands around ₹5,258M). Have to pay attention to the conversion rate.

Source: Investor Presentation

3 Likes